A few days before the traditional employee savings plan, and especially at the dawn of the season for the payment of profit-sharing and profit-sharing bonuses, here are 10 things to know about your employee savings plan.

Asset n1 – quickly pay income tax

Are you entitled to an incentive or participation bonus in 2023, based on your company’s 2022 results? If you take the cash, the sum will be added to your earned income, and will automatically increase your income tax.

If you place it on the company savings plan (PEE) offered by your employer, the operation is tax-deductible. You still pay social security contributions. Here’s how much you save. It all depends on your marginal tax rate (TMI), the rate that applies to any extra money added to your income.

| Gross employee savings bonus paid to the employee: 1500 | Marginal income tax rate | ||||

|---|---|---|---|---|---|

| 0% | 11% | 30% | 41% | 45% | |

| Net premium paid into an employee savings plan | 1355 | 1355 | 1355 | 1355 | 1355 |

| Net premium received in cash | 1355 | 1221 | 989 | 855 | 806 |

| Gain linked to the payment in the employee savings plan | 0 | 134 | 366 | 500 | 549 |

After deduction of the CSG-CRDS: 9.7%

After deduction of CSG-CRDS and income tax

Source Eres

Trick. To know your TMI, you can test the official income tax calculator on impots.gouv.fr. But you will also see it appear in a few months on your tax notice. It is a novelty of the year 2023.

Taxes: these new features that await you in 2023

Weakness n1 – If you are not taxable…

Logical consequence of the table above… If you margin in the left column, in other words if you are not taxable, you have nothing to gain (tax speaking) pay your annual profit-sharing bonus or participation in a plan of business savings.

If you are one of the households (more than 1 in 2) who do not pay income tax, it is however very important to make a choice on the option form, also called interest form or participation form. , provided by your employer. By default, without any choice on your part, the money will be placed on the PEE proposed by the company. And what’s more on a generally uninteresting fund (monetary or bond, often among the least profitable).

Taxes: should you cash or invest your employee savings premium?

Advantage n2 – A limited panel of funds, for a simple choice

For some, the proliferation of unit-linked funds on life insurance contracts is a guarantee of quality, for others it is a foothold in financial complexity. On this point, the vast majority of companies offer (via the managing body) a limited panel of a few employee savings funds – at most ten – to their employees. In the lot, most often: a low-risk monetary fund, a bond fund, a French equity fund, an international equity fund, and at least one responsible fund (SRI).

Weakness n2 – What help for salaries to invest?

When you bet on a bank investment, your banker is supposed to advise you. When you bet on life insurance or a retirement savings plan, you may benefit from the advice of an online savings broker or a wealth management advisor.

For employee savings, when it’s time to choose the funds in which you invest your annual premium, you realize that your employer is not a financial adviser (that’s not his colleagues. Some PEE managers have set up automated advice, but this remains minimal assistance, far from personalized advice. Companies using a service provider to advise wages are still few in number

salary savings: why you are so badly advised to invest your money

Asset n3 – Costs covered by the employer

Good news! Expenses? No charges! The management costs of your plan are compulsorily borne by your employer.

salary savings: are your plans too expensive?

Weakness n3 – Expenses not to be forgotten at the start of the company…

But…be careful, these management fees are no longer covered when the company leaves. In addition, indirect costs – levied by management companies on employee savings funds, called FCPE – are sometimes high. But almost invisible… which does not encourage employers and salaried savers to compare rates.

Incentive and participation: what does your departure from the company change?

Asset n4 – Money not so inaccessible as a

Admittedly, the exceptional release anticipated in version 2022 flopped. Only between 4% and 5% of the savings that can be released exceptionally in 2022 have been withdrawn according to the AFG, the group of asset managers. But this flop may be explained in part by an ultimately relatively relative unavailability of these funds invested in PEEs.

Marriage? Birth of your 3rd child? Divorce? Real estate purchase project for your main residence? So many events allowing you to release all the money amassed on your PEE without waiting for the 5 years of theoretical investment, and the list of events opening the way to early release is even longer: domestic violence, death of spouse, unemployment, over-indebtedness , business creation, etc.

Trick. On your annual statement and in your online customer area, your account manager (Amundi EE, Natixis Interpargne, CIC Epargne Salariale, Crdit Mutuel Epargne Salariale, Esalia, etc.) details year by year the amount of money you can withdraw.

The year, which was extremely difficult on the financial markets, did not spare any asset class

Weakness n4 – Really performing funds?

In 2021, MoneyVox had compared the performance over 5 years of the stock market, life insurance, employee savings and… the Livret A. Verdict? On average, PEEs were bottom of the class.

But it must be recognized that the period was unfavorable, on the one hand, and especially that the funds of the PEE were weighed down by the negative average performance of the monetary funds. More than non-performing funds, the PEE paid above all for the lack of advice! And therefore billions of euros vegetating on funds causing employees to lose money every year.

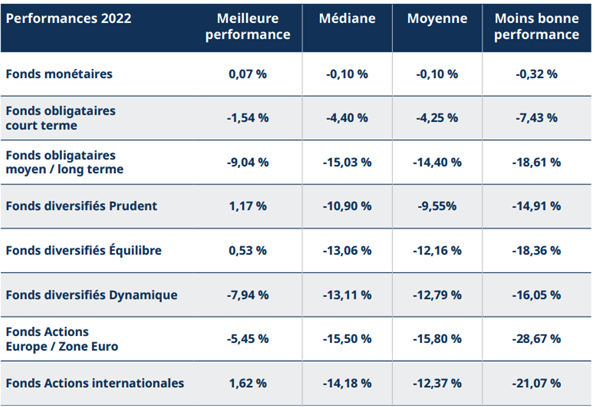

Mercer, a firm specializing in human resources, now publishes an annual barometer of financial management in company savings. Verdict of the year 2022? Some (modest) good news: For the first time in more than 5 years, thanks to the rise in interest rates, money market funds have improved their performance compared to the previous year and are getting closer to positive performance.

And some (very) bad news: The year, which was extremely difficult on the financial markets, did not spare any asset class. Since the launch of this barometer, this is the first time that all the types of funds analyzed have posted negative performance on average.

Excerpt – Mercer study. Methodology: 167 funds analysed, 9 asset classes analyzed and 9 market indices used.

Weakness #5 – An investment you only think about once a year

Once a year, or maybe twice. When you receive the annual employee savings statement, most often in February or March. And when you have to place your annual premium, if there is a premium!

However, the annual photo of your PEE and your investments from past years is not necessarily advantageous. This is probably the case at the start of 2023 following a catastrophic year on the stock market in 2022. Too late? Not necessarily, since the objective remains to invest in the medium term, over a horizon of at least 5 years.

Employee savings plan: 5 reasons not to throw away your annual statement

Bonus – Last asset: matching

Good plan. If ever your employer has set up a matching scheme, this will transform your PEE (or collective PER, if applicable) into an extremely profitable investment. This means, for example, that if your employer matches 50% of your payments (simplified example, the arrangements are generally more complex), you pay 1,000 euros… and that immediately adds 1,500 euros to your PEE. Unbeatable.

Profit-sharing, participation, PEE, PER: who is entitled to what for their wage savings?