The Carbon Score® is calculated by using the proprietary model developed by Axylia, presented on a scale from A to F. The score materializes the ability of companies’ operating profit to pay their carbon bill. The carbon bill represents the damage associated with tonnes of CO2 emissions over the entire life cycle of the company’s products and services.

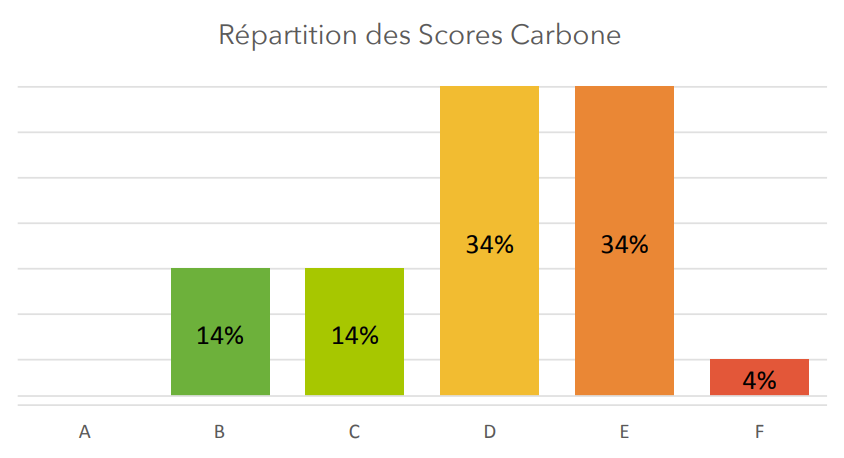

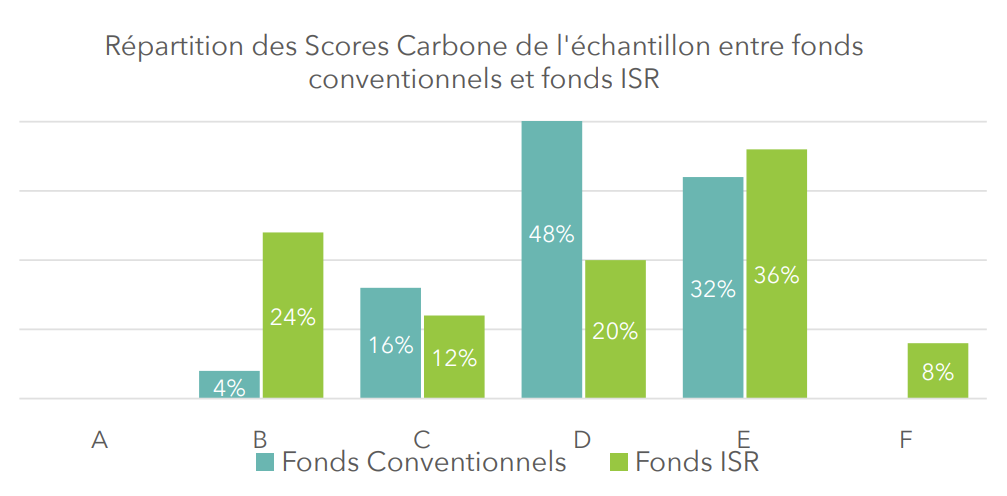

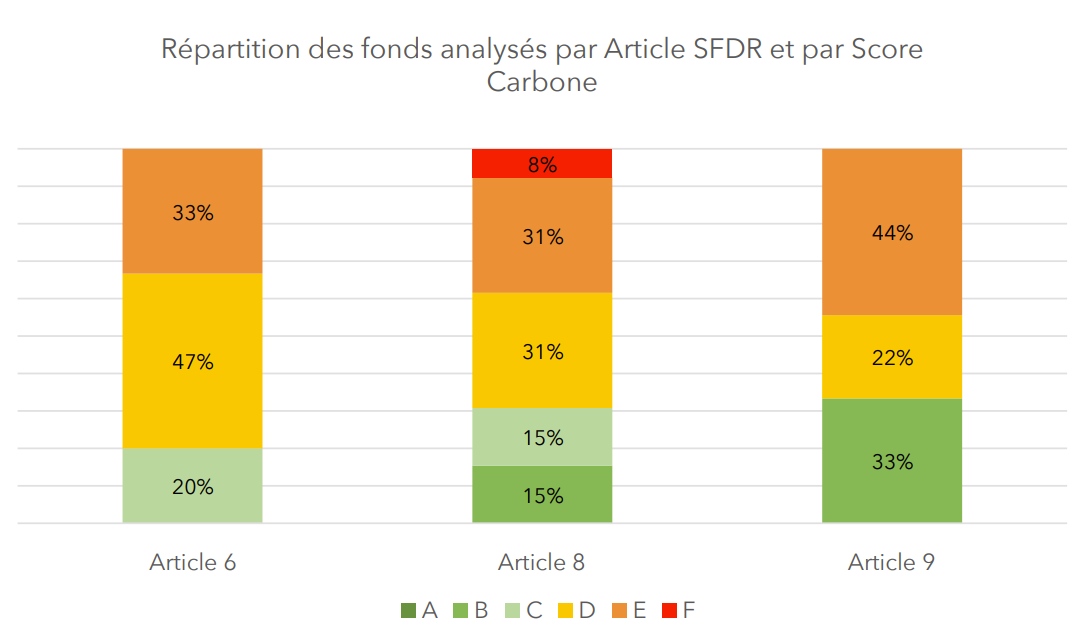

None of the 50 funds achieves the maximum Carbon Score of A. 72% (i.e. 36 funds with a combined total of 46 billion euros) obtain a “negative” Carbon Score of D, E or F. This means that their subscribers are at high risk. loss on their savings in the event of carbon pricing. The SRI funds in the sample are no exception either: 64% of them also obtain a “negative” Carbon Score. We observe that the SFDR regulations provide only imperfect information on the real extra-financial impact of the funds: in fact, 69% of the so-called articles 8 and 9 funds, supposed to integrate ESG criteria, are associated with negative Carbon Scores (D , E and F).

Faced with the systemic risk posed by climate change, Axylia is launching a platform displaying the Carbon Score of companies and funds, helping individuals and professionals to identify the structures that create the fewest negative externalities. A collaborative approach will allow Internet users to make the fund inventories usable in order to import them onto the scorecarbone.fr site. Ultimately, with the help of Internet users, the site will be able to cover the 10,000 funds offered on the French market. The platform creates transparency in order to say stop to greenwashing.

THE FINDING

In France, since 1997, a growing number of investors have used ESG ratings to guide their investment decisions. Like some academics, think tanks, regulators, big bosses and the Inspectorate General of Finance, we note the complexity and exhaustion of the ESG rating, which turns out to be confused and unsuitable to respond to the first of the dangers: climate emergency. Climate change imposes its physical law and forces us to reduce CO2 emissions and not simply to improve an ESG score! The price of the CO2 allowance (see graph) and climate impacts are increasing in Europe, but the ESG rating remains insensitive. When this method is under the wrath of greenwashing, the time has come for a change.

LITTLE SCIENTIFIC REMINDER

CO2 is responsible for increasing climate change. It is released by the combustion of fossil fuels (coal, oil, gas). It is a long-lived greenhouse gas (around 100 years) that traps the sun’s heat in the atmosphere. CO2 emissions can be classified into three categories: direct greenhouse gas emissions (Scope 1), indirect energy-related emissions (Scope 2) and other indirect emissions (Scope 3). However, this third aspect is very often underestimated, even not informed. CO2 emissions linked to use are much higher than those linked to production alone. This is the case for an automobile whose driving (100 grams of CO2 emitted for each of the 13,000 annual kilometers traveled during ten to twelve years of ownership) produces 80% of the life cycle emissions against 20% for its production. It is therefore essential to take into account the emissions linked to Scope 3, in order to obtain a complete result and to know the real responsibility of companies. This is the scope retained by the Carbon Score.

THE CARBON INVOICE SOLUTION

The alarmist speeches of scientists do not seem to be enough to change the world of finance and business. The explanation, in our opinion, lies in the fact that the two parties do not speak the same language: researchers speak of degrees, tons of CO2, when financials and individuals speak in euros. It lacks a common language.

Axylia started from an observation: in contradiction with the polluter pays principle, the damage associated with CO2 emissions is not borne by the company even though it is the source of it. We have worked to convert CO2 emissions into euros. Research by climate economists, taken up by the IPCC, values a tonne of CO2 at 108 euros. This is a tipping level, much higher than the price of the European quota (60 €) and much higher than other world prices.

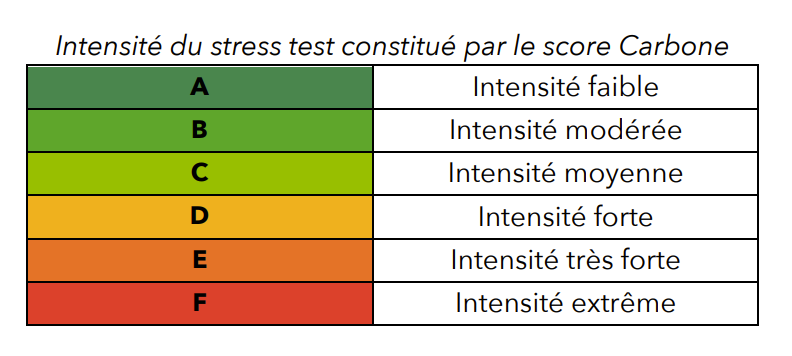

Each tonne of CO2 emitted degrades the operating result of the company. Companies emit millions of tonnes a year. If Nature sent the company its invoice and paid it, we could calculate a “carbon adjusted” financial result. A financial snapshot, this stress test makes it possible to know to what extent the company’s profit depends on CO2 emissions, then standardized in the form of a Carbon Score, according to its intensity:

- Breakdown of Carbon Scores

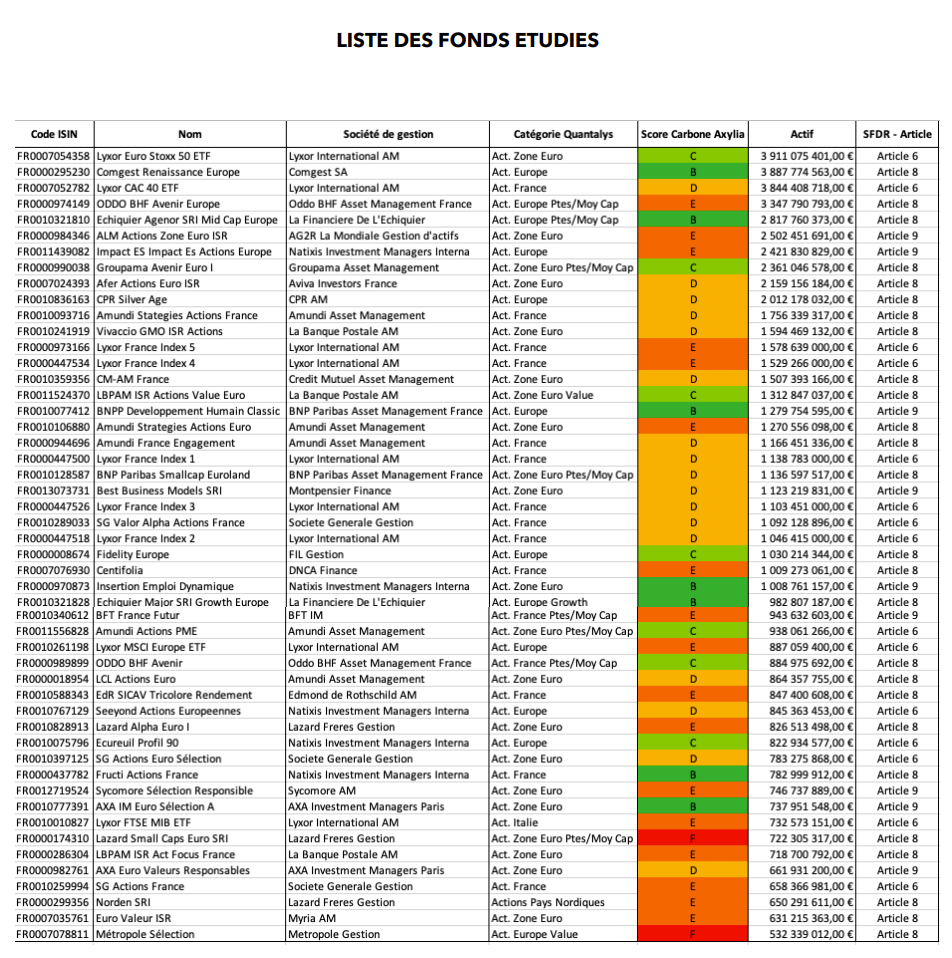

We studied 50 funds, SRI or not, invested in European and euro zone equities.

None of the funds obtain an A Score which is hardly impacted by carbon pricing. Conversely, 38% of funds are under intense or very intense stress (E and F). In total, 72% show a negative Score. Overall, the average of the companies present in the funds show a loss and the funds obtain a score of D.

- SRI funds vs conventional funds

The sample is made up of 25 SRI labeled funds and 25 conventional funds.

36% of SRI funds have a “positive” Carbon Score (A, B and C) against 20% for conventional funds. ESG analysis improves resilience but the two categories, labeled SRI or not, remain overwhelmingly exposed to a tariffed CO2, with an average Score of D. The ESG approach does, however, allow access to a greater number of funds. little exposed to carbon risk (B).

- Carbon score vs SFDR regulation

Since April 2021, European regulations require management companies to classify their funds according to their ESG intensity. The so-called article 8 and 9 funds have a strong and very strong ESG quality, respectively; Article 6 funds do not claim ESG quality.

Article 6 funds only have 20% positive Carbon Scores (A, B and C). Articles 8 and 9 each show almost as many positive scores. Article 9 funds have the highest proportion of B score. 67% of so-called article 9 funds have a negative carbon score!

The SFDR regulation is therefore not sufficient information to know the carbon risk of funds even if the articles 8 and 9 funds allow access to the greatest number of positive Carbon Scores.

* Sample of 50 funds under French law invested in European equities for an outstanding amount of 69 billion euros.

Sources: Quantalys, Trucost, Axylia, websites of asset management companies.