Last week, Bitcoin appeared to be on the verge of a near-term upside breakout. The world’s largest cryptocurrency by market capitalization had formed a bullish ascending triangle that could have seen it break above the key $25,200-$400 area, paving the way for a rapid rise towards the next major resistance zone around $28,000.

However, a combination of negative macro-level catalysts (strong US data and aggressive rhetoric from the Federal Reserve Bank which pushed US yields and the dollar higher and US equities lower) and regulatory concerns amid growing crypto industry repression limited bulls’ stance. Bitcoin ended up falling around 3.0% last week and is already down just over 1.5% this week.

At the current levels of $23,700, Bitcoin sits roughly in the middle of February’s $21,400-$25,300 range. And traders/investors seem confident that these fluctuations will continue for some time. At least this is the message that can be observed on the Bitcoin options markets.

Bitcoin fails to pass the $25,000 threshold

According to data presented by The Blockthe bitcoin volatility index (DVOL) of Deribit fell sharply over the past week, a direct consequence of Bitcoin’s inability to break above $25,000, which would have likely resulted in significant short-term volatility (most likely bullish). DVOL came in at 50, down from 60 this time last week. That’s not far off the all-time high reached in January at 42, just before the start of the 2023 surge.

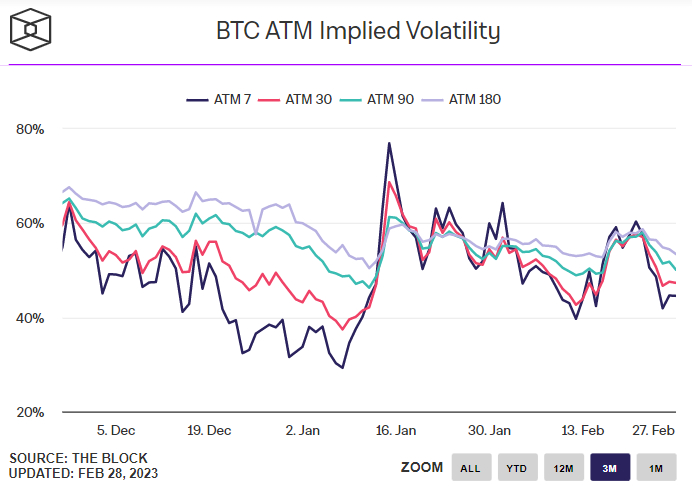

Separately, the implied volatility (Implied Volatility) according to the price of At-The-Money (ATM) options also fell sharply, with the outlook for near-term volatility down sharply. According to data presented by The Block, Bitcoin’s 7-day implied volatility was 44.55%, down from 60.33% last week. Implied volatility at 30, 60 and 180 days is also down sharply to 47%, 50% and 53.5%, from 57%, 58% and 58% respectively last week.

Mixed Price Outlook for Bitcoin in the Options Market

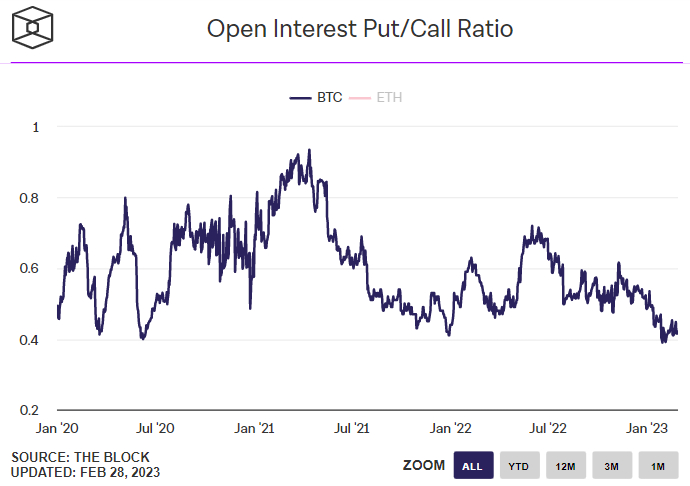

The options market presents a mixed picture on Bitcoin’s price outlook. For one thing, the ratio of open interest in normally bearish put options to normally bullish call options is firmly in favor of the latter, and near an all-time high. According to data presented by The Block, the open interest ratio for put and call options was 0.42, only slightly higher than the all-time high of 0.39 reached at the start of the month.

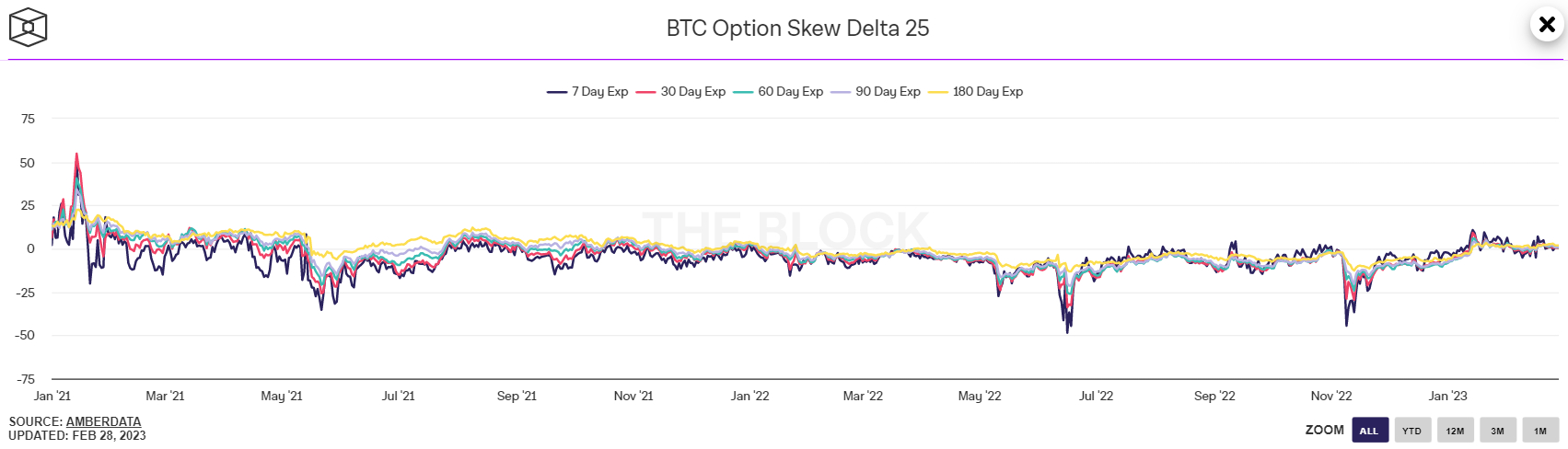

In contrast, Bitcoin’s 25% Delta Skew for options expiring in 7, 30, 60, 90, and 180 days is close to zero, implying a neutral positioning bias. The 25% options delta skew is a popular indicator of the extent to which trading rooms overprice or underprice upside or downside protection via the call and put options they sell to investors.

Put options give an investor the right, not the obligation, to sell an asset at a predetermined price, while a call option gives an investor the right to buy an asset at a predetermined price. An options delta of 25% greater than 0 suggests that trading rooms charge more for equivalent call options than for put options. This means that the demand for call options is higher than for put options, which can be interpreted as a bullish sign as investors are more eager to hedge against (or bet on) rising prices. price.

Follow our affiliate links:

- To buy cryptocurrencies in the SEPA Zone, Europe and French citizensvisit Coinhouse

- To buy cryptocurrency in Canada visit bitbuy

- To secure or store your cryptocurrenciesget a Ledger wallet

- To trade your cryptos anonymouslyinstall the NordVPN app

To accumulate coins while playing:

- In poker on the CoinPoker gaming platform

- To a global fantasy football on the Sorare platform

Stay informed through our social networks: