The Council of State has just confirmed it: the executive had the right, last July, to freeze the Livret A rate at 3%. The observation nonetheless remains true: the rule, which provides for an automatic review every 6 months based on inflation and interbank rates, is almost never applied. Should it be changed?

Thursday July 13, 2023. Bruno Le Maire appears on the TF1 television news to announce the bad news: the Livret A rate, expected at 4.10% due, in particular, to inflation, is maintained at 3%. Worse: this rate will not move, either upwards or downwards, before February 2025, whatever the evolution of the price and rate context. Six months later, the decision continues to be particularly unfavorable to saversas shown in our simulator.

How much will your Livret A earn you?

between February and August 2024? *

* For a stable amount of savings in your Livret A throughout the period, i.e. from 02/01/2024 to 07/31/2024

(1) Official Livret A rate of 3% from 02/01/2024

(2) Rate of 3.9% from the regulatory calculation formula

To justify it, the Minister of the Economy cited “ exceptional circumstances “. This is no coincidence: according to the decree (1) which governs the setting of rates for regulated savings accounts, these exceptional circumstances are necessary to justify the choice of the executive to decree the rate of Livret A. In their absence, the rule is automatic rate revision, depending on the result of an arithmetic formula integrating two variables, inflation excluding tobacco and short interbank rates. But the arithmetic was clear: the Livret A rate should have increased to 4.10% on August 1, 2023 and to 3.90% on February 1, 2024.

Were the circumstances really exceptional enough to justify this freeze? The Council of State, contacted by Paul Cassia, a professor of public law, in any case found nothing wrong with it.

Livret A: the bad news has fallen for the rate of your savings book

Against the “administrative fixing” of regulated savings rates

Quick look back: it has been almost 20 years, since 2004, since the principle of automatic revision of the Livret A rate every six months was put in place. Before this date ?

Fixing the remuneration of popular savings was a prerogative of the executive. From 1818, the date of creation of the booklet, to 1984, it was set by decree, then, from 1984 to 2004, by a dedicated committee (2). For the same result: for public opinion, the Livret A rate remained a political choice, driven by the executive. Result: any drop in the rate made it unpopular with savers.

It is in particular to put an end to the “serious disadvantages linked to the administrative fixing of rates” that a report (3) commissioned by Bercy and signed by Christian Noyer and Philippe Nasse, recommended in January 2003 to opt for a automatic indexation of the Livret A rate. A proposal implemented from July 1, 2004 by Francis Mer, at the time Minister of the Economy in the Raffarin government.

The latter, however, did not follow through with the logic of the Noyer-Nasse report. The executive retained the power to deviate from the new rulein the event of “exceptional circumstances” therefore, and to set the rate itself, on a proposal from the Banque de France.

The quasi-permanent exemption

Originally designed to find the best compromise between, on the one hand, the interest of savers (a “positive” return, that is to say higher than inflation) and, on the other, that of banks and borrowers (a resource close to market rates for their loans), the calculation formula has been adjusted several times since 2003. The latest one, in 2018, clearly tilted the balance in favor of banks and borrowers, by removing the inflation flooror this rule which meant that the Livret A rate could not be lower than inflation excluding tobacco.

The power of derogation remained. And what should have been the exception, the exemption in the event of “exceptional circumstances”, has become the rule. In recent years, automatic revision has only occurred twice:

The waiver power was used 11 times. But only 4 times in a sense unfavorable to saverstherefore to limit an increase in the rate:

- in August 2017, to limit the rate to 0.75%, when it was expected at 1%;

- on February 1, 2023, when the rate, expected at 3.30%, was set at 3%;

- on August 1, 2023, to prevent the increase to 4.10%;

- in February 2024, to prevent the increase to 3.90%.

Other government interventions were rather favorable to savers, in a context, it must be said, very particular. At the heart of the 2010 decade, faced with low inflation and market rates, the public authorities chose to smooth the reduction in the Livret A rate, which could have reached 0.25%. from February 1, 2015. Exceptions thus took place in February and August 2013, in February and August 2015, then in February and August 2016, before the government already decided to freeze the rate at 0.75% from December 2017 to January 2020.

“The depoliticization of rate setting, initiated in 2003, was a complete failure”

How can we explain that automatic revision has, to this point, become the exception? For economist Philippe Crevel, the answer lies in the very essence of the Livret A, this savings product so specific to France. “The Livret A does not obey pure economic considerations,” analyzes the director of the Cercle de l’Epargne. “It is also a political phenomenon, which takes into account social data. A mathematical formula can hardly convey the complexity of the issues surrounding this very particular and sacred product.. » Result: “The depoliticization of rate setting, initiated in 2003, was a complete failure. »

Desecrate Livret A?

How to get out of psychodrama? By returning to setting the rate by government decree? By letting banks set the Livret A rate as they see fit? “It seems complicated,” reacts Cyril Blesson, partner at Pair Conseil, which publishes Cahiers de l’Epargne.

” Why complicate life ? », continues the economist. “With Livret A, the government seeks to present itself as a bulwark against inflation. But there is an institution, independent of political pressure, whose vocation is precisely to set interest rates to combat inflation, and therefore the erosion of the value of assets: the European Central Bank. The simplest would be toindex the Livret A to the ECB rates, possibly taking into account the €ster. It would remain attractive, because its return is net of social security contributions and taxes. »

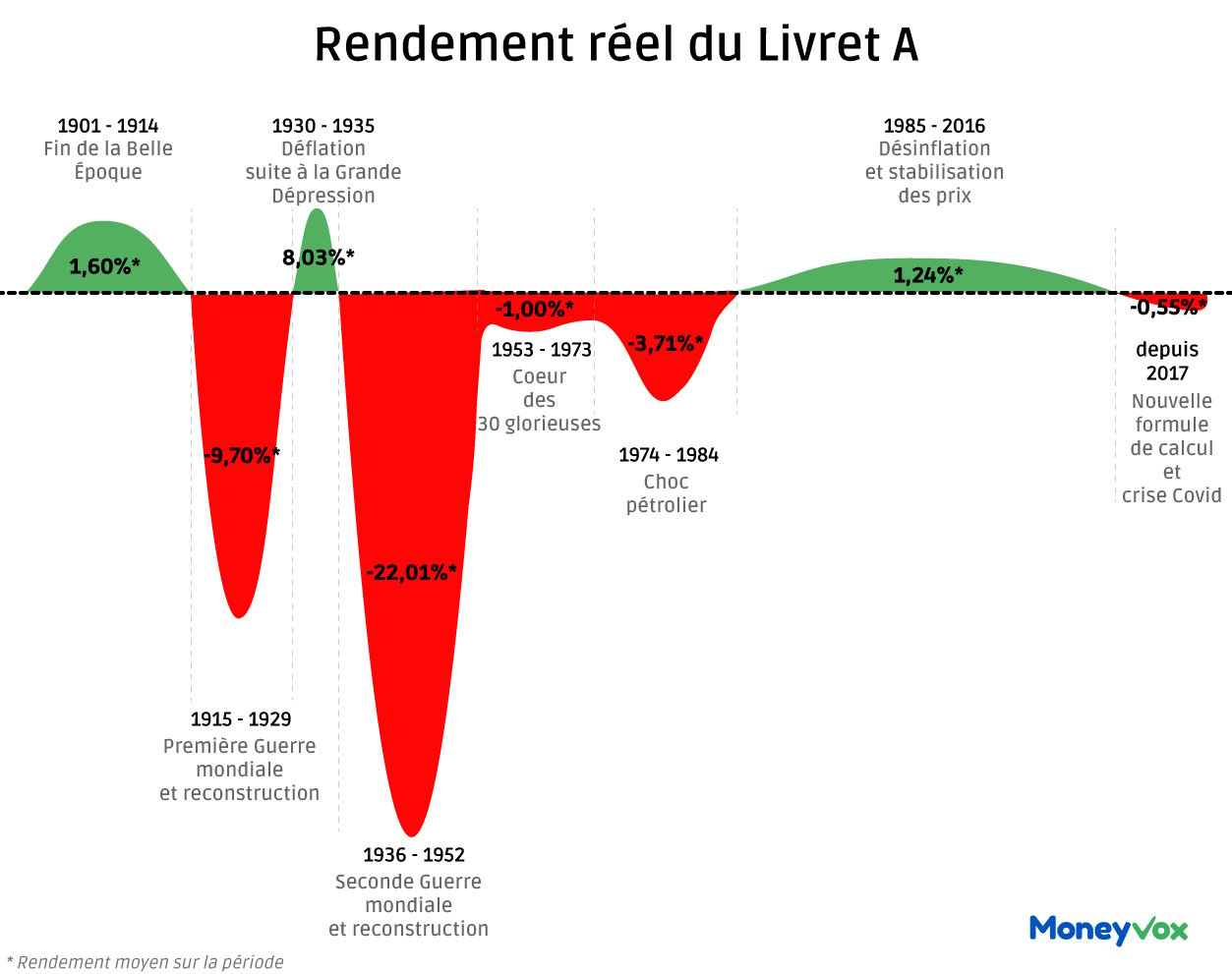

Clearly, it would be remove, at the same time, the power of exemption of the Banque de France and the reference to inflation. A solution which would not necessarily be unfavorable for savers: the rate of the ECB deposit facility is, for example, currently set at 4%, even if it is expected to fall next summer. The Livret A, moreover, has not always been, far from it, an effective shield against inflation, as shown in this infographic produced in July 2022.

The symbolic impact of such a choice, however, would be unpredictable. “It would be possible,” believes Philippe Crevel. “But this would amount to trivializing the Livret A, and therefore to renounce one’s sacredness. » The government that will take such a political risk has probably not yet been born.

(1) Order of January 27, 2021 relating to interest rates on regulated savings products. (2) Banking and Financial Regulation Committee, then Regulated Savings Committee. (3) Christian Noyer and Philippe Nasse, “Report on the balance of Savings Funds”, January 2003.