But just one car manufacturer?

Why Tesla takes so much beating

By Diana Dittmer

March 15, 2024, 7:26 p.m

Listen to article

This audio version was artificially generated. More info | Send feedback

Tesla is struggling. The shares of the electric car pioneer are falling and falling. The former fantasy seems to have evaporated, and more and more analysts are pessimistic about the company’s future. Is it high time to run away? The list of problems is long.

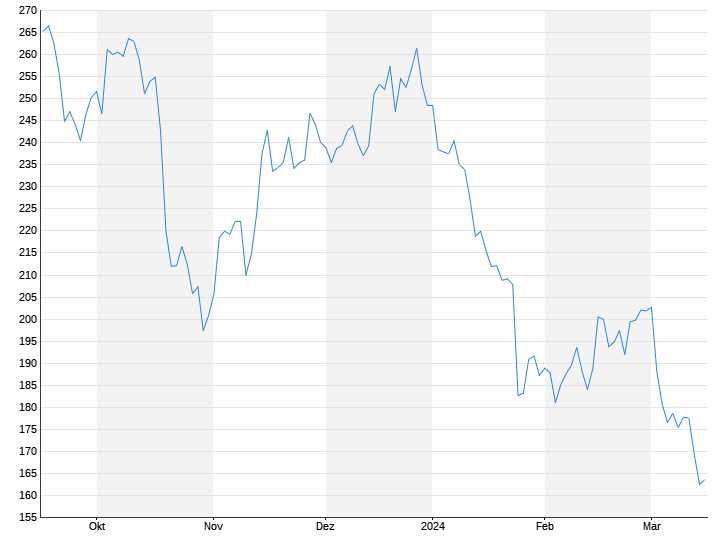

Since 2020, Tesla shares have only known one direction: it went up steeply. But the tide has turned. This year alone, the titles lost around 30 percent in value. More than $220 billion in market value was wiped out. Tesla has thus been thrown out of the list of the ten largest companies in the S&P 500. Critical analysts are hailing brutal downgrades. The US bank Wells Fargo only caused a setback in the middle of the week. The experts lowered their rating from “Hold” to “Sell”. They cut the price target from $200 to $125. The current price is $162.50. What is going wrong with the once successful electric car pioneer from the USA?

Tesla “doesn’t look so great anymore,” said Wells Fargo analyst Colin Langan. He forecasts 1.8 million deliveries in 2024. This would mean sales would stagnate compared to 2023. Earnings per share for this year are estimated at $2. In 2023, Tesla achieved an adjusted profit per title of $3.12. This doesn’t bode well for the future.

Especially because the fall height at Tesla is high. In contrast to other car manufacturers, the company is treated on the stock market like a growth or tech stock. At its peak, the valuation was close to 60 times estimated 2024 net earnings. This only works if investors are willing to price in expected earnings far into the future. This is what we call “future music” on the stock market. The valuation is now “only” 55 times. The comparison shows that this is still fabulously high: all S&P 500 companies together trade for around 20 times as much. Car manufacturers usually achieve single-digit valuations.

Tesla is getting old

Tesla is “a growth company without growth,” said Langan, summing up the problem. Apparently others have recognized this too. You can see how the tide has turned by the fact that the share of optimistic valuations on the stock has fallen to its lowest level since April 2021. The electric car pioneer no longer comes close to the quality and speed it once had. There are many reasons why this is so.

The pioneer of e-mobility is, above all, getting on in years. The automotive world around has changed. The hype about electric cars is over. Buyers are more cautious than expected. Industry and politics are rehearsing the role backwards. At the same time, competition has become significantly tougher. At the end of June 2010, when Tesla floated its shares at $17 apiece, the company was something special. Today over 100 car manufacturers build electric cars. According to the International Energy Agency (IEA), one in five cars sold worldwide will soon be electric. But the cake is too small for everyone.

The competitors are accelerating in their race to catch up. “Tesla is not only losing the American market, but above all the important market in China,” says car expert Ferdinand Dudenhöffer ntv.de. Chinese competitor BYD has replaced Tesla as the world’s largest seller of electric cars. Unfavorable for the US car manufacturer: China, the world’s largest car market, is oversupplied with electric cars and the Chinese like their own brands. Why buy a Tesla when domestic car manufacturers have successfully copied the Tesla look?

“Everybody’s Darling” on a par with the volume manufacturers

The brutal price war that Tesla itself has unleashed in China, combined with an outdated product portfolio where everything revolves more or less around one model, namely the best-selling Model Y, is making it worse. “The competition in China produces and sells cheaper,” says blogger and former Daimler digital boss Sascha Pallenberg ntv.de. “Western competitors have not only caught up in recent years, but have also partly technologically overtaken the electric car pioneer.” Due to the lack of new models, Tesla’s only option is to stimulate demand through price reductions.

But that’s exactly where the calculation doesn’t add up. The former “Everybody’s Darling” suddenly finds itself “almost on a par with the volume manufacturers in terms of profitability,” says Pallenberg. A disappointing development when you consider that Elon Musk previously promised investors an annual growth of 50 percent.

“The group’s growth story has suffered a huge setback in the last few quarters,” summarizes Pallenberg. The biggest omission from his point of view is Tesla’s misguided model policy. “Instead of concentrating on a cheap model for entry into the brand, extensive resources were wasted on the so-called Cybertruck and Tesla Semi,” he explains. The success of the Semi on the commercial vehicle market is de facto unmeasurable because it is hardly sold, and the Cybertruck only serves the US market.

“Musk’s influence on the brand is damaging”

Elon Musk’s aggressive pricing policy also fatally led to the fleet providers Hertz and Sixt delisting Tesla vehicles due to weak resale values. The experts agree that the car manufacturer has caused serious damage to itself. “In the used car market, Tesla is catching up with market reality,” says Dudenhöffer. Pallenberg finds clear words regarding the Tesla boss: “Musk’s influence on the brand is harmful.” Over 50 percent drop in the average selling price of used Teslas in 18 months, “this has never happened before in the history of the automotive industry.”

Dudenhöffer points out another construction site that Tesla himself caused – probably rather involuntarily. The company is struggling with repair problems and high insurance premiums. Of all things, the much-vaunted “gigacasting”, an inexpensive process with which large parts of the car body are die-cast in one piece, suddenly turns out to be a problem. “This makes small damages expensive. If insurance premiums for new cars rise as a result, the vehicles become less interesting.” And the industry expert sees new trouble coming soon: With a US President Donald Trump, things could become even more difficult for Tesla.

Some analysts, such as Wedbush analyst Dan Ives, consider Tesla’s ongoing price declines to be overly pessimistic. “Now is not the time to throw in the towel,” the US magazine “Fortune” quoted him as saying. Pallenberg comes to a different conclusion: “It seems as if more and more analysts are convinced that Tesla is ultimately just another car manufacturer and is many times overvalued at its current market capitalization. I think the current correction is long overdue.”