Due to the bear market, fundamentals, especially in the DeFi space, are increasingly becoming the focus of investors.

While investors in the DeFi boom year 2020 concentrated almost exclusively on how high the Total Value Locked (TVL) and the volumes of protocols such as Uniswap, Maker, Sushiswap and Co. were, they neglected whether the projects were actually profitable or not .

In the following, therefore, the profitability of various DeFi protocols. What does it even mean for DeFi projects to be profitable?

The profitability of DeFi protocols

All DeFi projects generate revenue (either for users or their own protocol) when users engage their services (token swaps, lending…). However, the percentage retained by the logs varies from log to log.

Furthermore, it is important to know that many DeFi projects incentivize their users to use their platform with token incentives. For example, users for trading on the decentralized exchange dYdX (DYDX) receive token rewards in DYDX.

read too

However, such token incentives also have disadvantages. The total range of tokens in a DeFi project is expanded in this way, which can be negative for the course. High log revenue alone is therefore not crucial to whether a DeFi project is viable or not.

The question is therefore always at what cost decentralized finance projects generate income. As with regular businesses, DeFi protocols also need to “spend money (tokens) to make money”.

Often, token issuance, i.e. the tokens that a DeFi project issues to attract more users to its platform, are the highest spend.

Protocol revenue and token issuance

The profit of a DeFi protocol can be defined as follows:

Profit = Protocol Revenue – Token Emissions

While other analyzes Focusing on the protocol revenue related to the revenue flowing directly to a protocol’s token holders, this analysis focuses on the revenue available to a DeFi project’s community (token holders + DAO) after their spend.

The profit thus includes all revenue available to a DeFi project, regardless of whether the profit is paid directly to the token holders or goes into a treasury managed by the community (DAO) of a protocol.

read too

the token issuance refer to the tokenized spend that a protocol distributes to users of its platform (e.g., through liquidity mining, trading incentives, or referral programs) in order to attract even more users to its platform.

While this definition does not include all costs that a DeFi project has, it gives a good idea of how profitable projects are.

DeFi: Are Maker, Lido and Uniswap profitable?

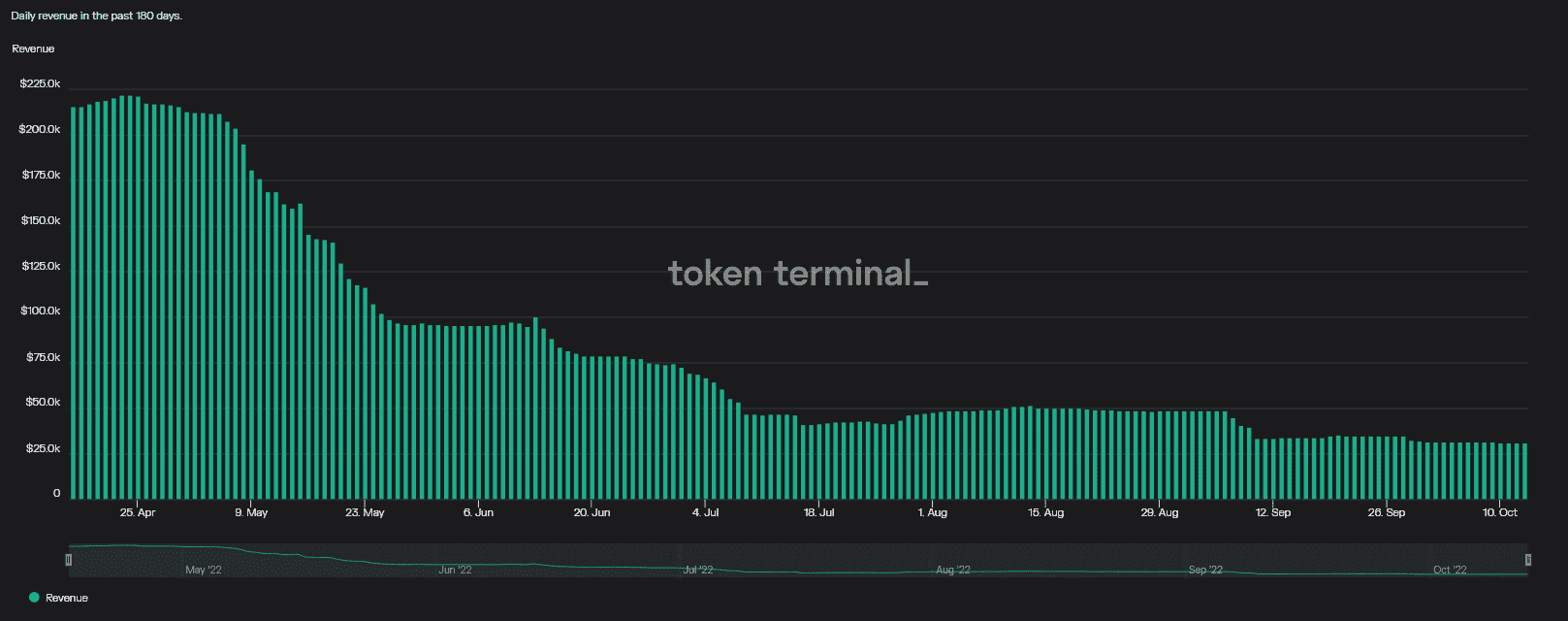

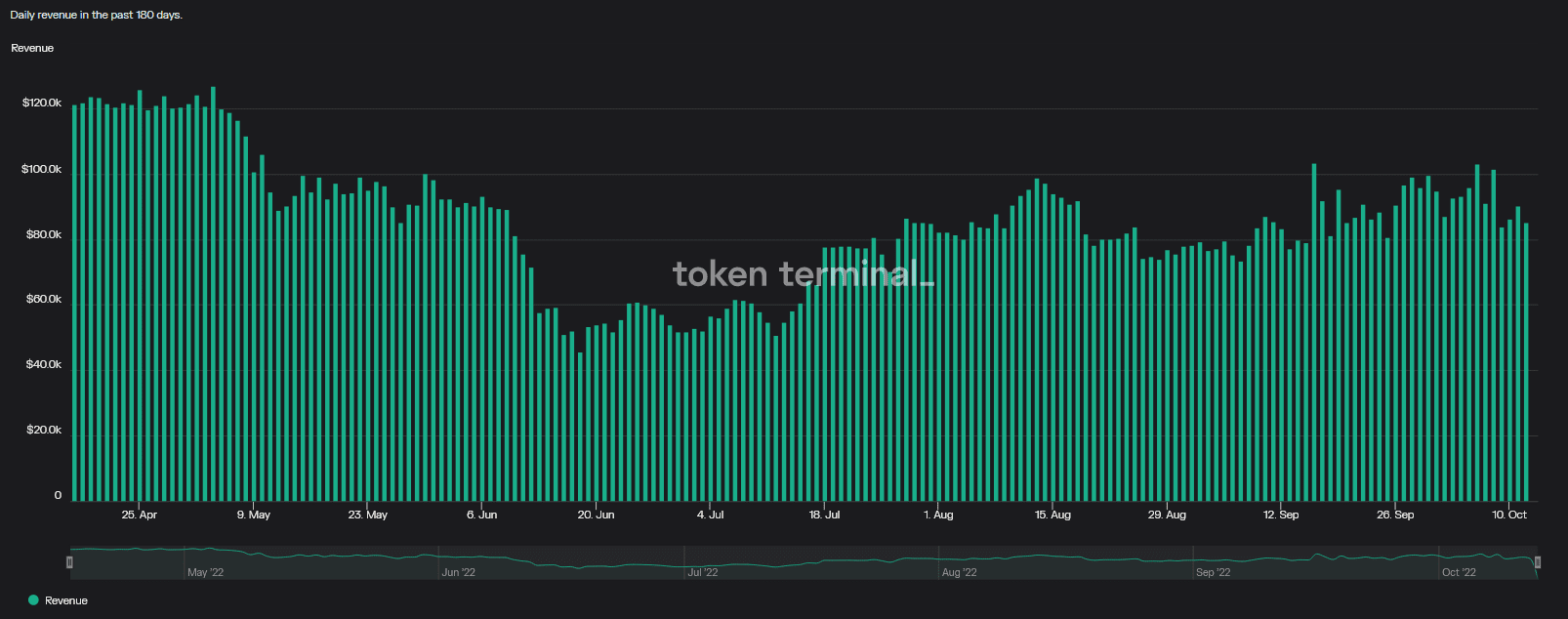

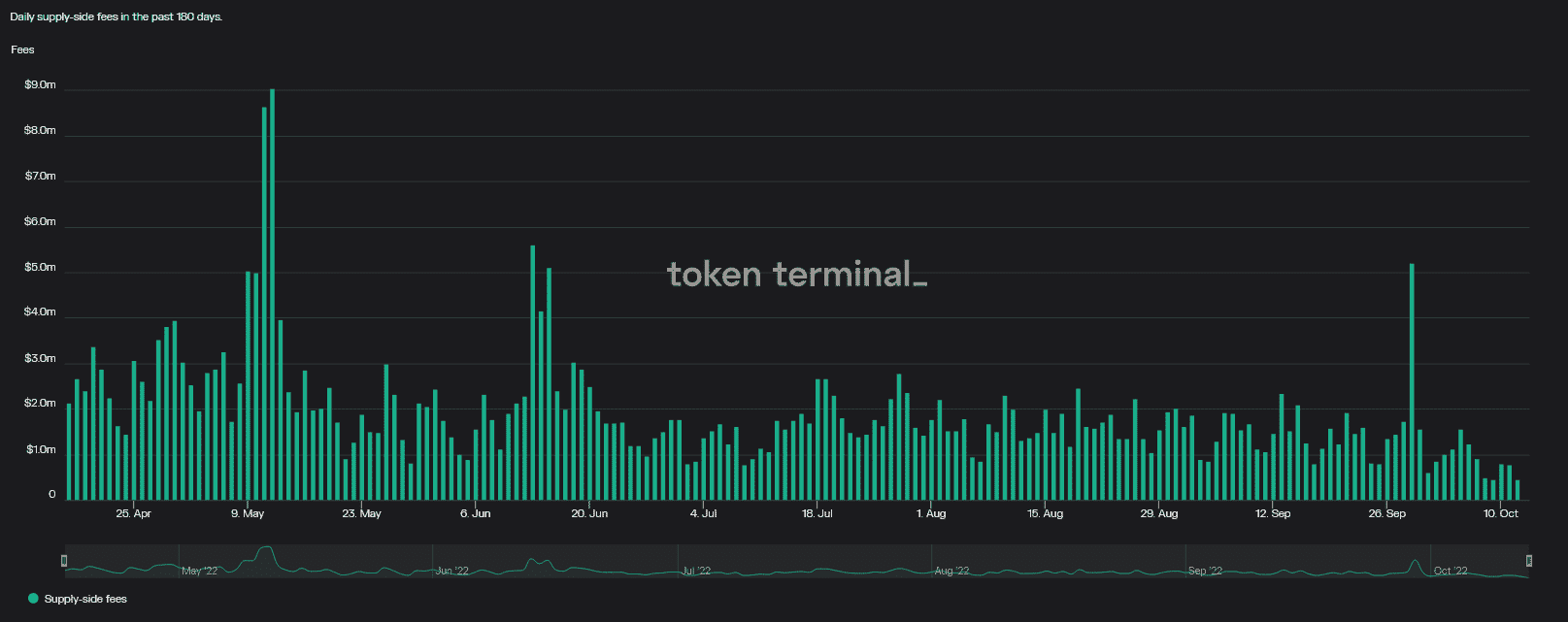

The following is an overview of the profit and loss recorded by DeFi protocols Maker (MKR), Lido (LDO) and Uniswap (UNI) between April 17th and October 12th.

1. Lending Protocol Maker (MKR)

Maker generates revenue from its protocol by charging interest to borrowers and taking a cut from liquidations of leveraged positions on its platform.

For the past six months, Maker has been able to Generate $15.1 million in total revenue. Of this revenue, 100 percent has gone to the DAO of MKR token holders, as Maker is not currently using token issuance.

The Maker Protocol is thus one of the few DeFi projects that is already profitable and growing organically.

2. Lido (LDO) Liquid Staking Protocol

The liquid staking protocol Lido generates revenue by retaining a 10 percent share of its validators’ staking rewards.

Lido’s total revenue for the trailing six months was $154.1 million, of which approximately $15.4 million went directly to the Lido DAO.

However, Lido has also spent a total of 46.5 million US dollars in LDO in recent months, among other things to incentivize various liquidity pools on decentralized exchanges such as Curve or KyberNetwork.

As such, crypto heavyweight Lido has lost -$31.1 million posted.

3. DeFi exchange Uniswap (UNI)

Providers of liquidity for trading pairs such as ETH/USDT or WBTC/USDC have received $349.1 million on Uniswap over the past six months.

However, not a penny of it flowed to UNI token holders or the Uniswap DAO as the DeFi exchange has not yet activated the “fees switch”. However, if the majority of UNI token holders decided to take this step, they could immediately earn between 10 and 25 percent of all revenue generated by the liquidity providers.

With a 10 percent profit share, the Uniswap DAO would have been like this for the past six months Earned $34.91 million.

However, it is unclear how the fee change would affect Uniswap’s liquidity. Liquidity providers’ revenue cuts could cause them to migrate to other decentralized exchanges. This could make trading on Uniswap less efficient and reduce the volume of trades processed through Uniswap.

Still, it is worth noting that Uniswap is one of the few DeFi protocols not to use token issuance to incentivize use of its platform.

So, Uniswap would be immediately profitable if UNI token holders decided to keep a portion of the revenue generated by the liquidity providers on their platform. This is probably also the reason why the UNI token is currently valued at over 6.3 billion US dollars.

It may come as a surprise to some that at the moment very few DeFi projects operate sustainably.

However, one should keep in mind that the DeFi sector is still at a very early stage of development. It is therefore not surprising, similar to traditional start-ups, that almost all DeFi protocols are currently investing enormous amounts of money in their expansion.

Amazon, Google, Uber and Co. also accepted losses in their early years in order to secure market shares and eliminate competitors.

Conclusion

Nevertheless, the constant issuance of tokens is of course not a sustainable strategy. It can even damage the prices of DeFi tokens enormously in the long run. Money is not infinite, and many token incentive schemes lose their power and effectiveness the longer they last due to the constant selling pressure they apply to DeFi projects’ tokens.

Moreover, the selling pressure from token issuance often deprives a protocol of its basis for survival as the funds that can be used to advance a protocol steadily depreciate in value.

In addition, the cutthroat competition in the DeFi industry means that DeFi protocols are unlikely to be able to drastically increase their profit margins. If they decide to do so anyway, they run the risk of losing market share to a competitor.

Therefore, in order to increase their profitability, it seems inevitable that most DeFi projects will reconsider their revenue streams if they want to survive in the long run.

Do you want to buy cryptocurrencies?

Trade the most popular cryptocurrencies like Bitcoin and Ethereum as an ETP on Scalable Capital, the leading investment platform in Europe.