Protected from head to toe

At the end of 2021, the group’s catalog contains more than 1,100 items corresponding to more than 8,000 references. The protective equipment sold through its distributors allows customers to protect themselves from head to toe. Offering a wide range of products is also an integral part of Delta Plus’ strategy, which sets it apart from most of the small specialized players on the market. It should be noted that their catalog is growing at the rate of approximately 15% of new products per financial year.

Here are the 5 segments on which Delta Plus Group is positioned: Head protection (21% of turnover), hand (14%), feet (25%), body (19%) and fall protection ( 19%), others (2%).

Breakdown of revenues by business sector 2021. Source: DEU

Some examples of products:

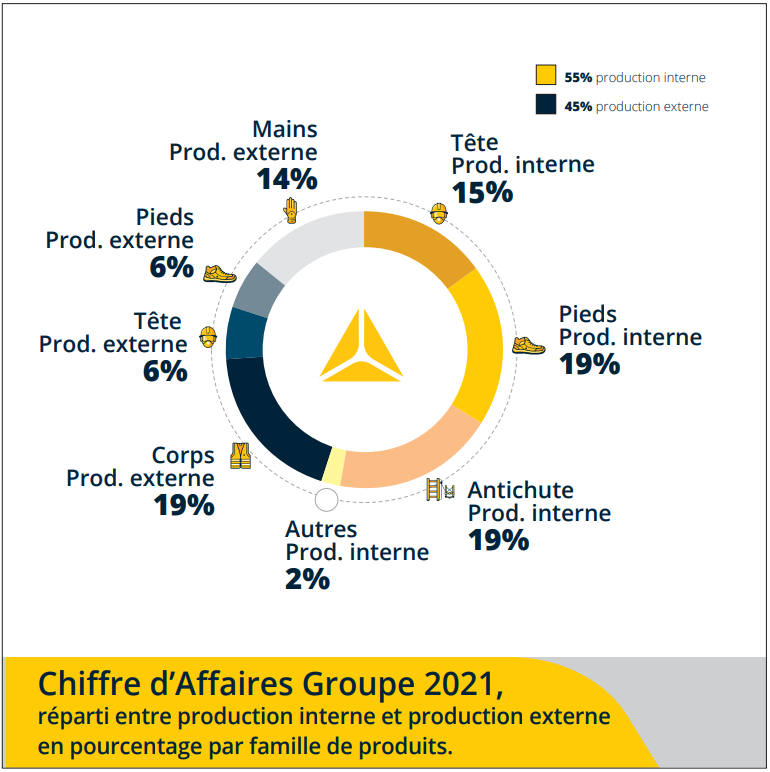

Head: helmets, hearing protection, respiratory protection, goggles, welding masks… 70% of the products in this segment are manufactured in-house. A single patent has been filed in this segment (in France and in China).

Hands: biological protective gloves, anti-perforation/cutting/burning/abrasion… disposable and reusable protective gloves… Products designed in-house but entirely manufactured by external suppliers.

Body: woven or non-woven (disposable) clothing. Jackets for increased visibility, protection against climatic factors (cold, heat, rain), acid-resistant, fire-resistant, cut-resistant, protective clothing against mechanical risks, etc. Products designed in-house but entirely manufactured by external suppliers .

Feet: shoes combining safety, comfort and aesthetics, resistant to shocks, crushing, perforation, cuts, burns, risks of electrocution, chemical and biological risks… 75% of products are manufactured in-house.

Fall arrest: segment divided into two sub-families, personal protection (harness, fall arrest device, anchoring systems) and protection intended to equip structures (guardrails, anchoring, lifelines, ladders, etc.) . The entire range is manufactured in-house. 4 patents have been filed on this segment.

Breakdown between internal production and external production on Delta Plus Group’s revenues in 2021. Source: DEU

Change of positioning on the vertical channel

Delta Plus is therefore a company whose 45% revenue comes from products manufactured in-house. The remaining 55% are manufactured by partner suppliers. Historically, this report was very different and it may continue to change in the future. Moreover, around thirty patents are being developed for fall arrest devices. The strategy behind this dynamic is simple: acquire or retain know-how relating to the design and production of equipment, develop industrial sites in strategic regions and improve the group’s margins.

Strong international presence and recourse to external growth

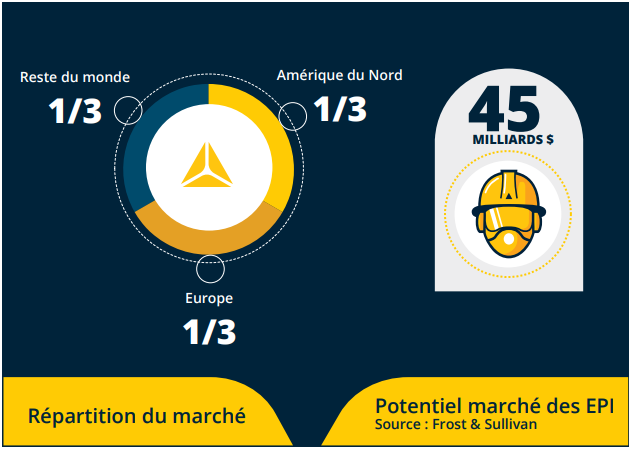

The PPE market is valued at more than €45 billion, split between North America (€15 billion), Europe (€15 billion) and the rest of the world (€15 billion). Contrary to what one might think, it is not a cyclical market, it exists all year round and is maintained by the regulations relating to the wearing of equipment in the various regions of the globe. In the USA and in Europe, it is up to the employer to provide the necessary equipment to its employees, it is exactly this kind of measure that holds the market. The development of these practices has also been observable in recent years in emerging markets.

PPE market. Source: DEU (Study by Frost & Sullivan)

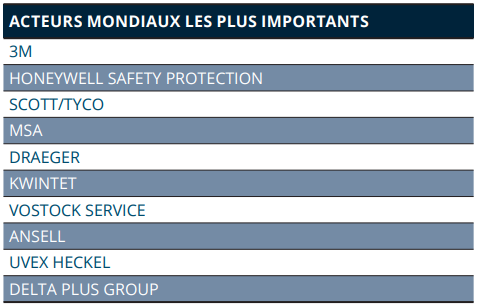

Delta Plus is a small cap which nevertheless ranks among the top 10 stocks in its sector. Very early on, the management made the choice to develop internationally through acquisitions.

Top 10 companies in the PPE market worldwide. Source: DEU

In this market, the number of takeover operations is growing, “with a tendency towards the disappearance of national mono-product manufacturers as well as the emergence of the consolidation of the various players (distributors and manufacturers)” underlines the management in the document. universal record. The actors must therefore, to continue to exist, differentiate themselves through innovation and rapidly grow in financing a significant number of operations.

Development strategy

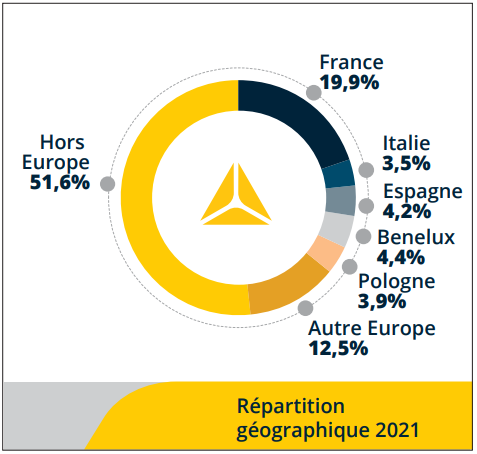

Delta Plus is therefore one of the rare players to offer a complete offer covering all five product families. Only 20% of turnover is generated in France and the company intends to maintain its place in the top 10 of the world players in the PPE market.

Geographical breakdown of Delta Plus Group’s turnover. Source: DEU

The company has 5 logistics platforms (3 in Europe, one in China and another in India), 35 distribution subsidiaries (17 in Europe, 18 outside the territory) as well as 13 production sites in Europe, America, Middle East and Asia. These are the distributors who directly supply the major user accounts (construction companies, Oil & Gas infrastructures, or heavy industry companies).

The group’s marketing plan is quite important, their objective is to refocus on a strong and above all unique brand image: Delta Plus.

Good use of leverage and a solid balance sheet

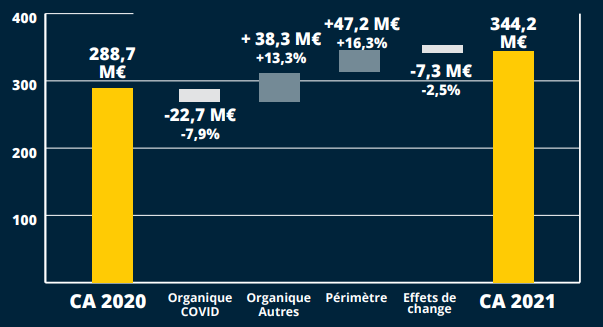

Delta Plus Group presents interesting financial characteristics specific to a company that develops through external growth internationally. Turnover in 2021 stands at €344.2 million, up +19.2% compared to 2020. This figure is quite different when the scope and exchange rate effects are eliminated: the group’s organic growth is by +5.4%. Moreover, over this same financial year, the unfavorable exchange rate effect did not go unnoticed, the company lost €7.3 million following the depreciation of South American currencies against the Euro in the first half of the year. year.

Delta Plus Group revenue growth breakdown. Source: DEU

The 2021 financial year was also characterized by the drop in “covid-19” activities (masks), largely offset by the strong recovery in the segments which had particularly suffered from the economic slowdown in 2020. It should be noted that the covid crisis did not prevented the group from conducting its external growth policy: 7 acquisitions have been finalized since the start of 2020.

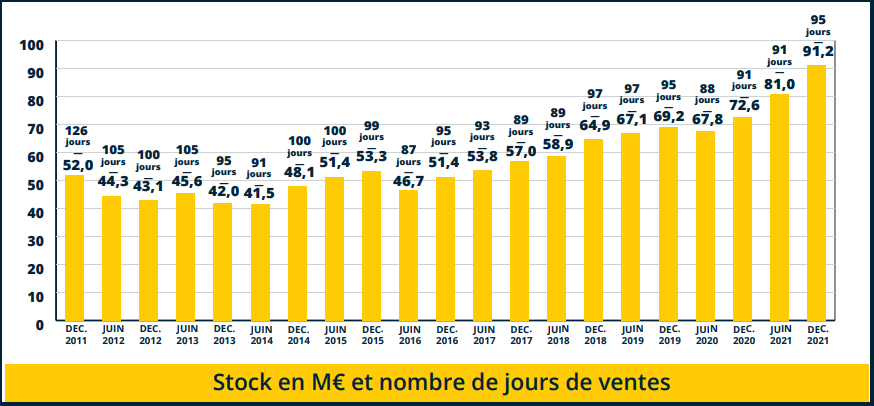

By studying the financial statements of the company, we are able to calculate its economic profitability after tax. With an apparent tax rate of 24%, this profitability is about 11.3%. Among the capital invested that makes it possible to obtain this ratio, we note the presence of a very substantial WCR of €102.2 million, or 107 days of turnover. By studying the results of the previous semesters, however, we note that this WCR is currently at historically low levels. To form a clearer opinion on the management of this WCR, it is necessary to analyze the evolution of stocks over the last few years in relation to the group’s turnover. It is obvious that with the growth of the turnover the company is led to change its stocks, but the analyst must ensure that the rhythm of these changes is of the same order of magnitude, it is also for this reason that it is customary to express inventories and other WCR elements in days of turnover.

Evolution of Delta Plus Group inventory levels. Source: DEU

Remember that in a context of very low short rates like the one we have just gone through, the financing of WCR is facilitated, good management also consists in not managing it. Unsurprisingly, in this favorable environment, logistics stocks or those operating in high BFR sectors are doing quite well. With the rate increases (current and future), this management will once again become an area of vigilance for this type of company which manages a very large quantity of inventory.

The group’s financial profitability stands at 16.8%, 5.5 points above the economic profitability. This attractive leverage is created through competitive debt at an apparent rate of around 2.4%. Over the 2021 financial year, financial expenses relating to €90.8 million in debt represent 4.8% of operating profit. This information, as well as the maintenance of debt ratios at satisfactory levels (Net debt / CP = 46%), implies that the group still has room to finance new acquisitions over the following years.

Vigilance point

Delta Plus Group is a company with “quiet” organic growth, the creation of wealth for the shareholder is done mainly through the growth of the balance sheet and the rapid integration of new acquisitions. Over several decades, the group has demonstrated that it is able to buy at a good price and that its relations with funders are healthy. However, external growth presents significant risks: a company can sometimes take more than 5 years to catch up with the errors resulting from a bad operation.

When a medium-sized group decides to rapidly expand abroad, it does not immediately have the same skills and tools to protect against currency effects as multinationals. The 2021 financial year proves to us that working with several currencies can have significant consequences. An unfavorable effect of 2.5% of turnover in organic growth of 5.4% hurts.

Admittedly, the PPE market is not cyclical, but there is no doubt that contracts between distributors and end customers do not automatically extend over time. A client company can change references from one financial year to another if the quality does not suit it.

The fact that this company 1- is developing through external growth and 2- has a high working capital requirement should alert analysts: it is vital to monitor changes in debt ratios and the exposure of the company balance sheet at rates. This type of company requires a lot of short-term and long-term capital.

Strong points :

- Small-cap with potential in a niche market

- Efficient use of debt and control of leverage

- Excellent acquisition and integration history

- The company is gradually establishing itself across the entire value chain

- Impeccable evolution of all profit and loss account items

Weak points :

- External growth requires a lot of capital and mistakes are expensive

- The company manages a large quantity of inventory, a BFR of 107 days of turnover represents a freezing of funds penalizing for the company.

- Investors who favor internal growth and companies with a MOAT will not find their account on this kind of values.

Find the interview with Arnault Danel, Financial Director of Delta Plus Group HERE.