Between prices, services, advantages and disadvantages, it is not always easy to choose your next bank card. Here is an overview of the best cards by category to better guide you in your choice.

The bank card is still the most widely used method in France today. Banks are well aware of this and the banking offer is therefore so plethoric that it is difficult to know which type of card to choose, whether for a main or secondary account. Depending on the needs, desires for freedom or control of one’s budget and the banking products to subscribe to, making a choice is far from child’s play.

So, which credit card to choose? Several elements are to be considered such as the type of card (physical or virtual), the monthly or annual price, the range and the organization of the card, but also the type of debit or the authorized limits, etc.

In this article, we’ll list the types of offers, their pros and cons, and the cards we recommend.

Free cards, a good idea?

If, a few years ago, talking about free bank cards was not yet a subject, today most online banks and even traditional banks have largely taken the plunge. It must be said that the commercial argument has a lot of impact in addition to creating an ideal loss leader.

So inevitably, in the batch of questions that we can ask ourselves: are these bank cards really free? Can I use this card anywhere? Will I be restricted in my purchases? Are there any clauses to respect under penalty of paying? We have selected the three best free cards on the market so that you can make a better choice.

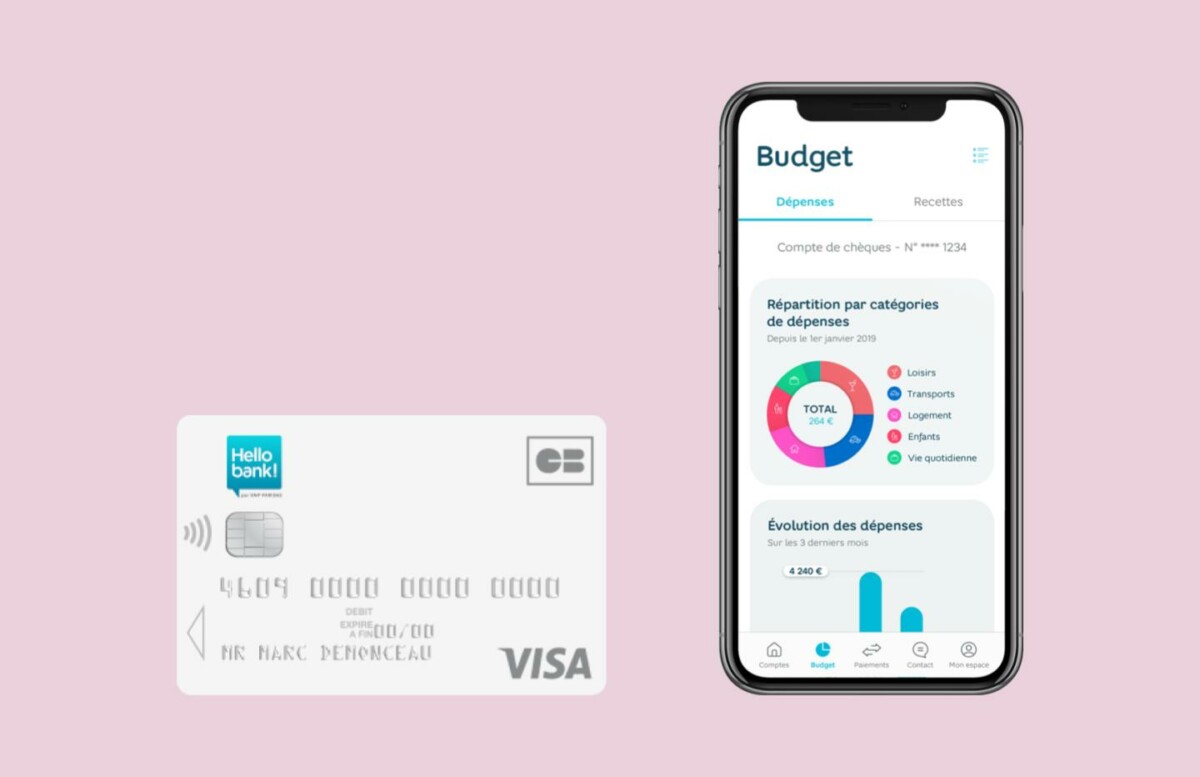

Hello Bank: Hello One, the benchmark!

In the department of free bank cards, the Hello One Card from Hello Bank is a benchmark. It is perfectly designed for daily use or secondary use for small expenses. She also benefits from the package “ zero fees » of its paying counterpart Hello Prime with, in addition, no account maintenance or inactivity fees or commission on transactions; in addition to free payments abroad. However, keep in mind that even if withdrawals are unlimited and free, they are only via ATMs from BNP Paribas or their subsidiaries abroad and those of the Global Alliance network. Also note that the Hello One card is available as a Duo offer for a Joint account.

If you want to know more, do not hesitate to consult our complete opinion on Hello Bank.

Boursorama Banque: Welcome and Ultim, the outsiders

Boursorama Banque is one of the most popular online banks in France with over 4 million customers. Its success is also explained by its offer of cards, in particular free with the Welcome and Ultim offers. However, they are not 100% free, you have to count on maintenance fees of 0 euros, provided you use your card at least once a month. There are other conditions to take into account, such as the amount of income or a mandatory initial deposit. These are not the only advantages since even payments and withdrawals are free of charge abroad (in the Euro zone) and you are entitled to a free withdrawal (1.69% of the amount beyond) outside the Euro zone. .

If you want to know more, you can consult our complete Boursorama Banque review.

Fortuneo: The Gold CB Mastercard in ambush

You read correctly, a free Gold card and it’s at Fortuneo that it happens. With the upcoming shutdown of the CB Mastercard, it is the Gold that takes over. It enjoys more or less the same advantages, namely the total absence of fees on all payments and withdrawals by credit card, anywhere in the world as well as the premium insurance guarantees of the Mastercard organization. However, if it is accessible for free, some elements are to be taken into account such as the 1800 euros of monthly income to be justified for registration and the fact of having to use the card at least once a month under penalty of incurring costs. It is therefore aimed at a more affluent public wishing to make Fortuneo a main account. The Fosfo MasterCard, on the other hand, is less advantageous when compared to the offers above.

If you want to know more, feel free to read our full Fortuneo review.

Standard and Premium cards, a good draw?

Today, online banks or neo-banks have been largely inspired by the offers of traditional banks to add to their offers more advanced advantages than a simple bank. We can think of banking products such as credits, savings books or insurance, all at more affordable rates and much less strict conditions than before. The so-called “standard” and/or “Premium” card offer has also evolved in this direction and for once, you will see that it is mainly the neobanks that are doing well.

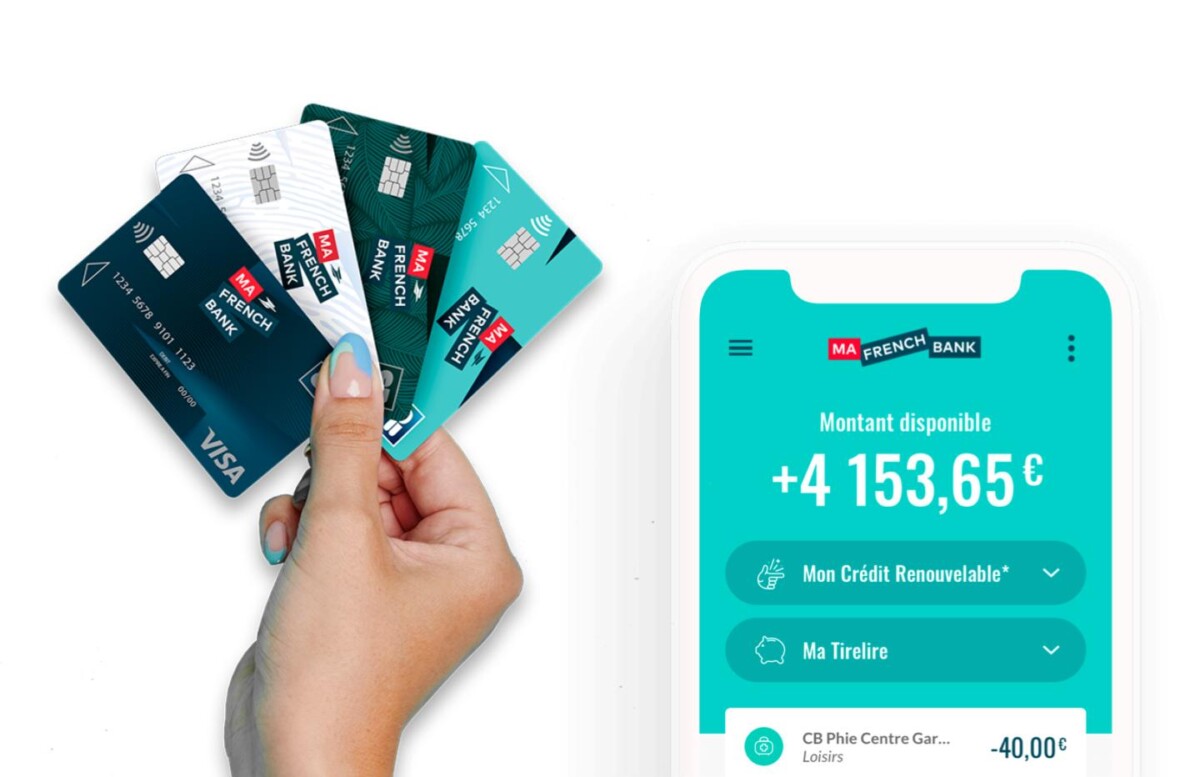

My French Bank: An ideal first account

If Ma French Bank is a neobank focused on young people, this does not mean that its offer remains competitive. The accountidealaccessible at €6.90/month proves it well thanks in particular to the accessibility of a few banking products such as subscription to consumer credit or a Cashback offer directly activated on the account and which is becoming more and more extensive. The “Ideal” account also does not charge any fees on payments and withdrawals abroad, regardless of the account chosen, even outside the Euro zone, which is rare enough to be underlined.

To find out even more, do not hesitate to read our full review of Ma French Bank.

Orange Bank: The Premium card with arguments

Orange is one of the historic players in the Mobile, Fiber and ADSL package market and has also entered the world of neobanking for a few years. Its offer is comparable to other leaders of the genre such as N26 or Revolut. If the bank offers a free card, but quite limited, it is its Premium card which is much more interesting. This is available for only €7.99/month (€4.99/month for one year for 18-25 year olds). The latter offers free payments and withdrawals whether in France or abroad, even outside the Euro zone. There is also no defined cap on payments or withdrawals. Banking products are also varied, such as the possibility of having authorized overdrafts and of benefiting from all Mastercard insurance (practical for travel). Orange Bank also offers a Cashback system with up to 10% refunded on all purchases made in the Orange online store or in store (mobile, accessories and connected objects). 5% of the amount of your Orange invoices are similarly reimbursed.

To learn more about Orange Bank, do not hesitate to consult our complete review.

Monabanq: a unique card, and even more

Monabanq is an online bank that tends to be forgotten in the face of other more prestigious brands. However, it benefits from the know-how of a traditional bank being a subsidiary of the Crédit Mutuel Alliance Fédérale Group. But it is above all through its card offers that the bank is doing well, and in particular the Uniq + offer. For a relatively low monthly fee (9 euros), it offers premium services that some online banks reserve for their most advanced cards. First, it offers free payments and withdrawals, regardless of the zone, which is a definite advantage. But it also includes high levels of insurance such as purchases on the internet or on a telephone, but also the establishment of an authorized overdraft in addition to payment ceilings adjustable according to income.

If you want to know more, you can read our full review of Monabanq.

Platinum or Black cards: is your money worth it?

Used as a term by credit card organizations such as Visa or Mastercard, Platinum refers to so-called “high-end” cards generally aimed at a more affluent public capable of spending more than the average. Inevitably, online banks and neobanks have for some integrated this type of card into their offers. Beyond the luxury of owning one, the advantages can be various such as special services and insurance or reductions when purchasing in partner shops, etc. Let’s see which cards in the field are likely to appeal to interested parties.

N26: Metal for your money

The Metal card from N26 is first and foremost an object. This card entirely made of stainless steel has a small effect once taken out of the wallet. This has a price: €16.90 per month, or nearly €203 per year. Its main asset concerns its payment and withdrawal ceilings which are particularly high and above all customizable from the application. It also offers the best possible insurance and coverage, especially for travel, mobility and health, much more than any other Premium card. The card also gives access to telephone support 7 days a week, no matter where in the world you are. Of course, payments and withdrawals in and outside the Euro zone are free and unlimited with a limit for withdrawals in Euros (a maximum of eight free transactions per month).

Click the link for our full N26 review.

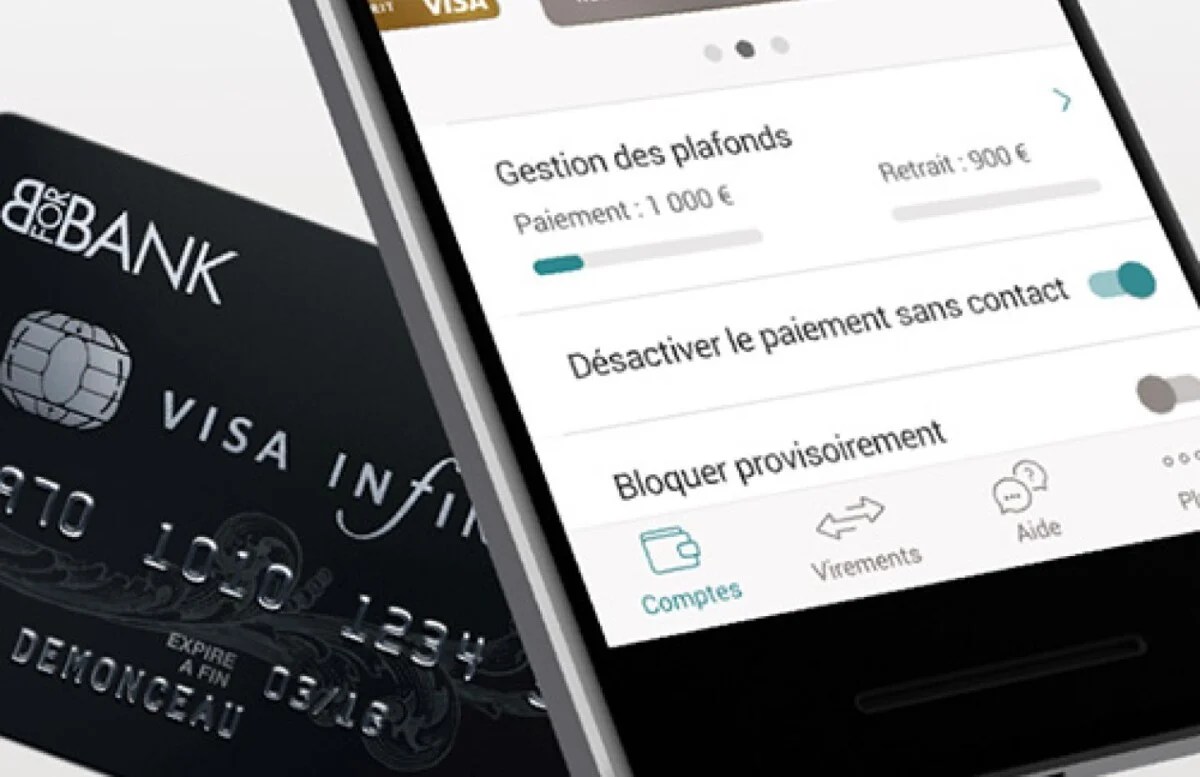

BforBank: Towards infinity and VISA

BforBank is one of the only online banks to offer the most prestigious card in the entire VISA range. It must be said that Crédit Agricole’s Premium online bank cultivates a top-of-the-range philosophy aimed at a wealthy public. The card costs 200 euros per year, its price is justified by the contribution of many advantages not found in a range of intermediate cards. It first offers flexible ceilings with a base of 3,000 euros over 30 days for payments and 1,000 euros over 7 days for withdrawals. It is especially in terms of travel insurance that it is worth it with complete protection ranging from flight cancellations or modifications or loss / theft of luggage and medical assistance taken care of wherever you are. La Infinite also offers a personalized concierge service: an advisor is dedicated to you for many situations, whether it’s when booking a trip, a table at the restaurant or tickets for VIP events. However, it is limited for use abroad, because if it offers free withdrawals wherever you are, payments are still subject to fees (1.95% outside the Euro zone).

If you want to know more about BforBank, you can refer to our full review.

To follow us, we invite you to download our Android and iOS application. You can read our articles, files, and watch our latest YouTube videos.