Golden times for Nvidia

“We underestimate what else can come out of AI”

By Diana Dittmer

08/24/2023, 5:13 p.m

Quarterly sales doubled, stock market value tripled – things are going well for Nvidia. The high demand for special chips for AI catapults the Californian company into spheres that Intel or AMD can only dream of. Fund manager Daniel Kröger even sees room for improvement in this area.

The Californian chip manufacturer Nvidia is rising into fantastic spheres: the expectations before the announcement of the tech company’s figures were high. But the result once again exceeds all expectations.

The AI boom has exploded the business in the past quarter: “In this quarter there was a 46 percent operating margin. Nvidia has existed for 32 years, in all these years Intel has never achieved such a margin. The highest was 32 percent.” , says Daniel Kröger, fund manager asset management Ehrke & Lübberstedt, ntv. Nvidia not only doubled its sales in the past quarter to $13.5 billion year-on-year. Profits also climbed from 656 million to 6.2 billion dollars (5.7 billion euros).

Anyone who plays computer games or dives into virtual worlds uses chips from Nvidia – mostly without knowing it. But it is above all the field of artificial intelligence that has recently turbo-charged the growth of the Silicon Valley company. In general AI fever, Nvidia has the advantage. Because its chips and software are particularly well suited for AI applications. Among other things, they are used to teach programs such as the hyped chatbot ChatGPT.

The tech company has left its competitors far behind, says fund manager Kröger. “Nvidia has an 80 percent market share, which is huge. The company is far superior not only on the hardware side, but also on the software side.” On the software side, it is “years ahead” of competitors like AMD.

For experts like Kröger, this is no coincidence. “The hype didn’t fall from the sky,” says the fund manager ntv.de. “Research in this area has been going on since 2015. It’s been known for a long time that Nvidia can do something. First they developed for gamers, then came Bitcoin. They’ve always been evolving. What wasn’t foreseeable was the great demand in the area of AI, that we see today.”

It’s the moment for the company: Data centers are being converted on a large scale. Nvidia has developed a family of high-performance chips to do just that. To the delight of CEO Jen-Hsun Huang, “A new era in computing has begun. Enterprises around the world are transitioning from general-purpose computing to accelerated computing and generative AI.” The figures show that there was a particularly large jump in the past quarter in the business with technology for data centers. Sales rose by a good 170 percent over the previous year.

Can success last?

Kröger does not expect an abrupt end to the hype. “The boom and the demand in the field of AI is still gigantic. Especially if you look at the server landscape. In recent years, chips worth a trillion dollars have been installed at cloud providers. That’s exactly (Nvidia’s) market ,” says fund manager. Only 50 percent of the demand can currently be supplied. Serving future demand will be a challenge. “You can see how the market has turned completely.”

The stock market apparently has no doubts that Nvidia can meet this challenge. The Shares have a run that stockbrokers rarely see. Analysts had previously expressed concerns that the company might not be able to secure enough production capacity from contract manufacturers. Because Nvidia itself does not have its own factories for the production of chips. Instead, it uses various contract manufacturers such as Taiwan’s TSMC and UMC groups for mass production. But guidance for the next quarter seems to allay concerns.

Apparently, a good agreement was reached with the pavers, says Kröger. It remains to be seen to what extent Nvidia can adjust the production figures at TSMC in its favor. Kröger assumes that long-term contracts will secure supplies at the previous level. Overall, the chips that Nvidia needs account for only five percent of total chip production.

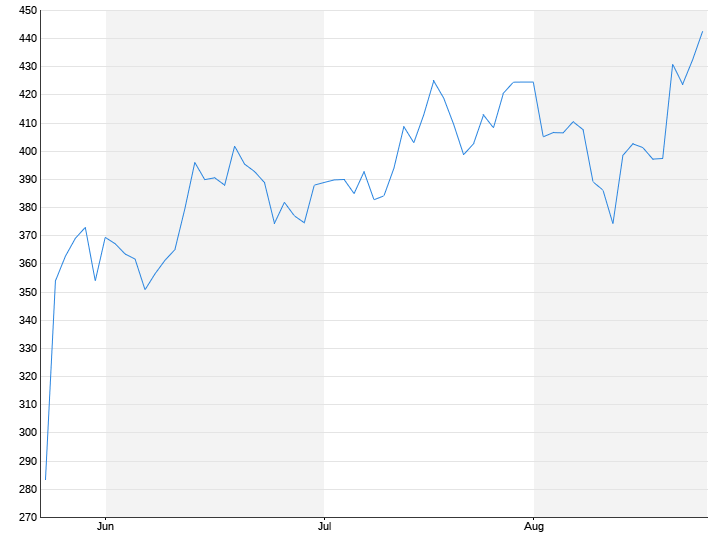

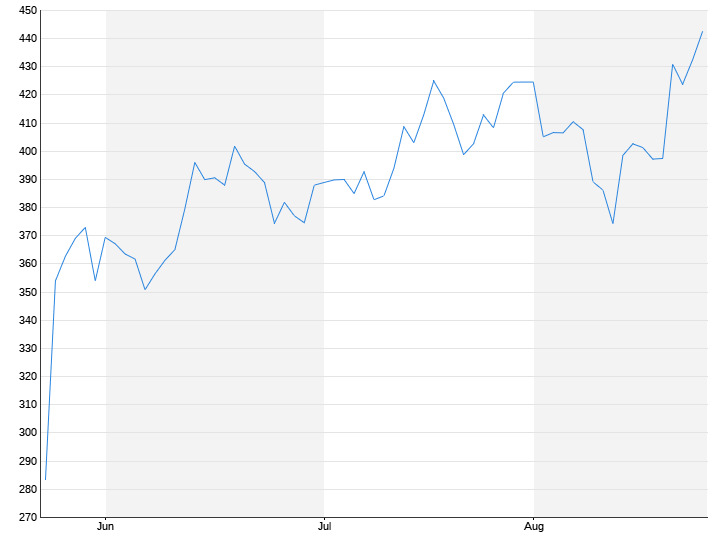

Meanwhile, Nvidia papers cost more than three times as much as at the beginning of the year. The company is worth around $1.2 trillion on the stock exchange. By way of comparison, the long-dominant semiconductor giant Intel weighs in at just over $143 billion.

AI – hype in the short term, underestimated in the long term

“In the short term, the hype may have reached an unhealthy point. Whether you should still start at this level is a legitimate question,” says Kröger. “But in the long term, it’s a bet on know-how. We underestimate what else can come out of AI.” Kröger assumes that there will be a lot of room for improvement in development and applications over the next five to six years. “Bill Gates once put it this way: Things are hyped in the short term, but underestimated in the long term. It’s the same with AI.”

Nvidia fuels this fantasy: The company expects sales to increase further to around 16 billion dollars in the next three months. The company had realized almost as much in the entire financial year that ended at the end of January 2021. “The outlook underscores Nvidia’s role as a key beneficiary of the artificial intelligence boom. As demand for chatbots and other tools skyrockets, companies are stocking up on the company’s processors,” writes market analyst Konstatin Oldenburger of CMC Markets. It seems as if Nvidia could soon push even Apple from the stock market throne of the most valuable companies. On the other hand, the trees for Nvidia would not grow to the sky. The announced capital increase could indicate that it will become more difficult to find areas in which Nvidia can expand in the future. “This is also a warning to the AI fans,” says Oldenburger.

“As of yesterday, the market valuation seemed too high,” says Kröger. “Let me say, with the figures for the next quarter, the valuation comes down a bit: But of course Nvidia has to maintain this growth for a very long time in order to justify the valuation. I’ll quote Jeff Bezos: ‘Your margin, is my opportunity’, (translated: Your margin is my challenge). With the high margins, competitors will jump on it, they want a piece of the cake.” This catch-up race could still take “two to two years”.