Are you renting an apartment or a house, renting it unfurnished? Like more than 4 million tax households, you receive property income! But declaring this rental income can turn into a headache: they are not pre-filled, you must choose between real and micro-property regimes, without forgetting the deductible charges… The procedure to follow, depending on your situation.

Do you have a painful memory of the complex categorization of work in the 2020 declaration? Rest easy, in 2022, as in 2021, back to routine. Here is how to declare your property income.

Micro-land tenure or real regime: an irrevocable choice

If the rents received each year do not exceed 15,000 eurosyou have the choice between real tax systemwhich requires a strict count of charges, and the simplified regime says micro-land. More than a third of taxpayers declaring property income opt for this simplified regime, which allows you to avoid filling out an attached declaration, and to benefit from a flat-rate deduction rather than listing the detailed menu of your rental expenses.

This choice is made at the start of step 3 of the online declaration. In the Revenues section, you must either tick the Micro property box: gross receipts not exceeding 15,000 euros for the simplified scheme, or the Land revenue / unfurnished rental box.

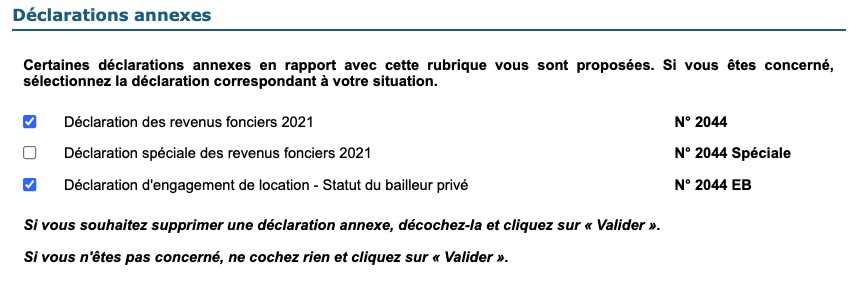

If you check the box Property incometo choose the actual regime, a window opens immediately, asking you which annexed declaration corresponds to your situation: the 2044 in most cases, the 2044 special more marginally for specific tax measures (15% of households declaring property income are concerned), and the 2044 EB if you are concerned by rental investment schemes (Pinel, Denormandie, Scellier, etc.).

Check the boxes that correspond to your choices and types of rental income.

Please note: if your rental resources exceed 15,000 euros, you must necessarily opt for the real regime by filing an annex declaration 2044. On the other hand, if your property income is below this threshold and you choose the real regime, this choice is irrevocable, and it commits you for 3 years, therefore for 2021 income but also for 2022 and 2023 income. the tax office in its documentation: this choice necessarily concerns all of your assets.

What about income from an SCPI?

Part of your property income comes from holding SCPI shares? This does not prevent you from opting for micro-property, as long as all the resources are below 15,000 euros. On the other hand, if your property income comes only from SCPI, you are forced to opt for the real regime.

Other exceptions: you must complete appendix 2044 special if you have invested in a tax SCPI subject to a specific regime (depreciation in Robien or Borloo), or form 2047 dedicated to income from foreign sources for certain SCPIs. In this case, it is advisable to rely on the tax receipt provided by the SCPI manager.

Micro-property: simplicity and flat rate reduction of 30%

Opt for the micro-land is clearly the simplicity option! No attached declaration: you only need to fill in the amount of your gross rental income received in 2021, without reducing any charge, the box 4BE of the classic declaration 2042. The tax authorities will ask you, in addition, the number of properties concerned, the address or addresses, and the identity of the current tenants: this information is the only ones that are pre-filled if you have been renting these properties for several years.

A flat-rate allowance of 30% will automatically be applied by the Public Treasury to these gross receipts, in order to compensate for one-off and recurring charges related to your property. If this flat-rate deduction does not seem to you to be up to your rental expenses, you can opt for the real regime, but be aware that this choice commits you to the next two declarations.

What about the 4BK line?

This box is located just below the 4BE. This is land income from foreign sources if you are eligible for the micro-land regime. They are isolated because they are not subject to withholding tax. Important note: you must not subtract this income from that shown on line 4BE, which must take into account all of your property income. This foreign source income is therefore shown in both line 4BK and line 4BE. You may, for example, be concerned if you own SCPI shares drawing certain income from buildings located abroad, following the instructions of the SCPI manager.

Actual plan: detail all deductible expenses

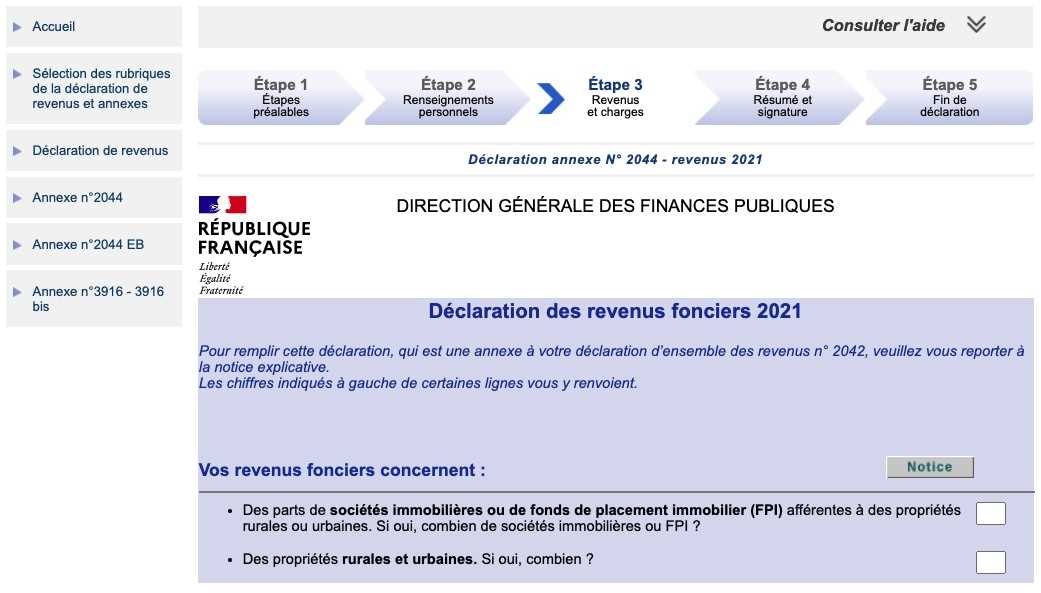

L, it gets complicated! Mission: list all the costs related to your unfurnished property(ies) for rent. For most donors, the annex declaration 2044 is sufficient, the special declaration remaining marginal. On the online declaration, this appendix sheet automatically appears in the left column if you have ticked the Property income box and then Declaration of property income (2044) at the beginning of the Your income step.

To access the attached declaration, use the left column: appendix n2044.

It is up to you to list your assets then, for each building, the receipts on the one hand, and the various costs settled in 2021 on the other hand (administration costs, insurance, repairs, taxes, loan interest by also filling in the section 410via the detail tab next to the corresponding box – co-ownership charges, etc.).

Good point of the online declaration: the tax authorities calculate and report many amounts over your declaration, which offers you considerable help. In case of difficulty, consult the detailed instructions dedicated to the real regime. Given the complexity of this regime, in some cases, the help of a professional (wealth management advisor, rental manager, etc.) may be necessary.

Taxes 2022: who can help you for free with the 2021 tax return?

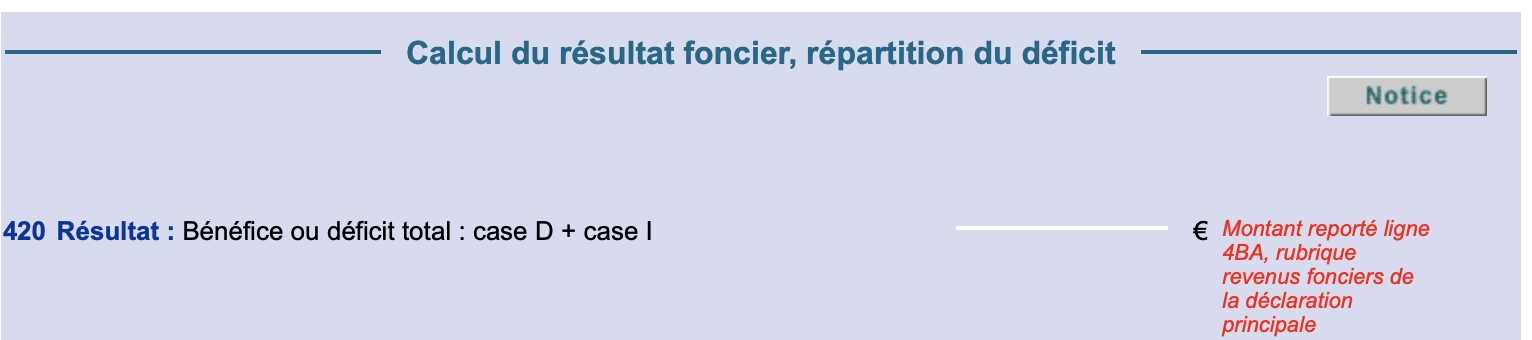

The amounts obtained using this annexed declaration must then be transferred to the lines 4BA (taxable income) and possibly 4BL if a part comes from assets located abroad in the classic declaration. In the vast majority of cases, you only have to fill in line 4BA, based on the result obtained using the appendix. The tax office also shows you in red the amount reported in the main declaration.

The DGFiP tells you here the amount reported on line 4BA of the main declaration.

To know: you did not attach supporting documents to your declaration, but the tax authorities can claim them from you. You must therefore keep for at least 3 years all the necessary documents (invoices, proof of co-ownership charges, etc.).

Land deficit: if you have done work

It gets complicated if you paid for work in 2021 and want to declare a land deficit. A choice that obviously involves the real tax system. The principle: reduce your taxable income by charging the cost of your work in 2021 to your rent received in the same year. If the cost of the work is greater than the amount of your property income, then you generate a property deficit: this deficit then allows you to reduce your taxable income.

The list of charges that can reduce your property income (and then possibly create a property deficit) is long: property tax, agency fees, insurance premiums, bank credit interest, and above all all maintenance and improvement work. rental property.

save up to 50% on your borrower insurance

Using real diet schedule 2044you are going to detail your work: on the one hand the amounts of the repair, maintenance or improvement expenses line 224on the other hand the details of this work (contractor, date, etc.) lines 400. Obviously without forgetting to indicate the other loads in the same table. By following the instructions of the tax authorities, you will then obtain a result report the line 4BC of the classic declaration: it is the land deficit that will reduce your taxable income (overall income) for the year 2021. Or even an amount carried over to 4BB if your land deficit ever exceeds the annual ceiling of 10,700 euros.

Here again, in the event of work and if the declaration proves to be too complex, the help of a professional can be invaluable.

Pinel reduction: the 2022 declaration

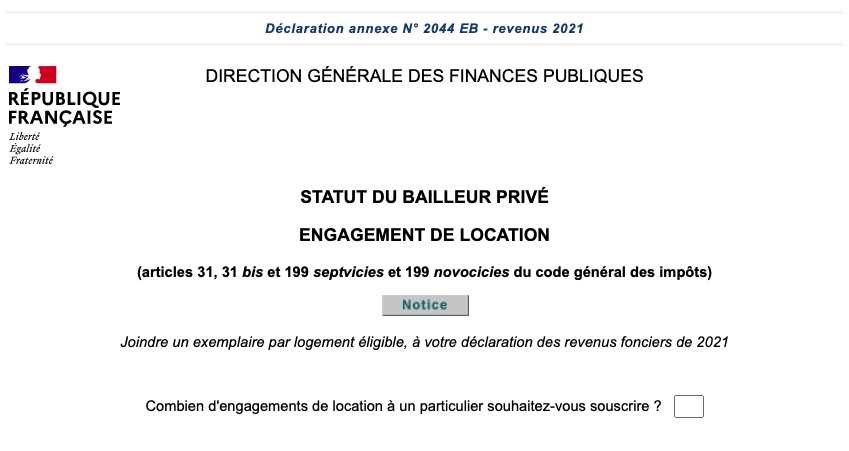

Are you renting an apartment or a new house in Pinel? Or a renovated accommodation in Denormandie? Annex 2044-EB allows you to declare your rental commitment: it must be completed if 2022 is the first year for which you are requesting this tax reduction. In other words if you bought a new property in 2021, or completed the renovation work in 2021.

Form 2044 EB: one copy per rented accommodation.

You must complete the process by entering the amount of the investment under the heading Tax reductions and credits / Pinel rental investments: an amount indicate box 7QA if you acquired a property in mainland France in 2021 that you agree to rent for 6 years , or 7QB if you agree to rent it for 9 years. The following lines concern tax reduction carryovers, complete if you invested before 2021.

Note, line 7RR, this box must be completed if you agree to rent for 3 additional years under Pinel conditions, for an investment made in 2015 and which therefore comes to the end of the 6-year cycle. Must be completed if you want to continue benefiting from the tax reduction.

How do I declare rents from furnished accommodation?

If you receive income from furnished accommodation, especially if you rent out a property on a platform such as Airbnb, you are subject to a totally different regime, most often that of non-professional furnished rental (LMNP). Furnished rental falls within the scope of industrial and commercial profits (BIC) and not property income.

Taxes: how to declare a Pinel or Scellier extension

Should tax installments be checked at source?

If your property income is recurring, you have paid income tax installments, as part of the withholding tax, in 2021. The amounts appear pre-filled on line 8HW at the end of the statement. As these are installments deducted directly by the tax authorities from your bank account, these amounts cannot be modified.

End of rental: a checkbox to stop the installments

If you no longer receive property income in 2022, you must now tick the box 4BNwhich will allow you to no longer pay monthly installments for this source of income.