|

|

| Tops / Flops of the week |

Tops Teva (+35%): The market welcomed the agreement reached by the company to extinguish a legal action in the case of opioids which is shaking the United States. The laboratory that produces generic drugs will pay up to $4.35 billion in total.

Phase / sunrun (+30%): Like other players in the sector, the two companies benefited from the agreement reached between American parliamentarians on the United States’ climate plan, which includes spending on clean energy.

Worldline (+17%): Investors appreciated the dynamic growth of the French payments operator in the second quarter of 2022. The publication is reassuring after a complex phase for the sector.

Hapag-Lloyd (+17%): The maritime carrier also exceeded the objectives at the end of the first half. HSBC noted to reduce to keep its recommendation, with a target of 300 EUR.

Hermes (+10%): The leather goods sales jumped in the second quarter, driven by strong growth in the West and the strong recovery of the Chinese market in June. flops

Fresenius Medical Care (-19%): The German group lowered its 2022 forecast due to a rapid deterioration of the American labor market and the persistence of high cost inflation. Confirmation of 2025 targets did not lessen investors’ disappointment.

Stanley Black & Decker (-15%): The manufacturer of power tools disappointed heavily in the second quarter. It also sharply lowered its earnings projections for the year. Wolfe Research has lowered its opinion and changed from buying to neutral on the issue.

Charter Communications (-10%): The operator was fined $7.37 billion for a systemic security breach that led to the theft and murder of an elderly woman in the United States.

Eurofins (-10%): Half-year results are solid, because organic growth is a bit disappointing. “The guidance for fiscal 2022 has been revised upwards, but the implied margin decline to around 20% and the subdued free cash flow update may raise questions,” says analyst Jefferies. |

| Raw materials |

Energy : The nervousness remains palpable on the oil markets, which await the next meeting of OPEC+ on August 3, in order to refine their projections of world supply. In the very short term, Russian production should decrease in the coming months, a decline partly offset by the rise of Libya, whose supply should drop from 800,000 barrels per day to 1.2 million barrels per day. On the gas side, prices reached new highs this week in Europe. The Dutch benchmark, the TTF, jumped to over 200 EUR/MWh at the week’s high. Russia continues to exert pressure on prices by reducing flows passing through Nord Stream 1.

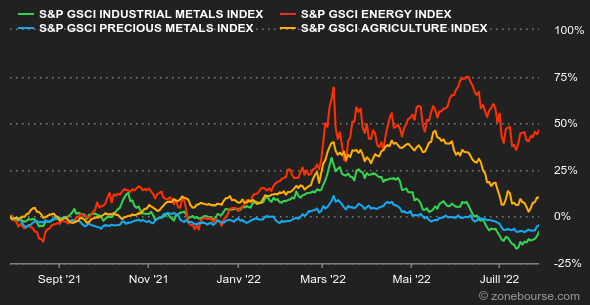

Metals : Metal prices have picked up again this week, helped in part by the weaker greenback. Weak prices should also impact global supply. Some mining companies, such as Freeport-McMoRan, have warned that they cannot continue to operate some unprofitable mines. This should help to tighten the balance between supply and demand. On the LME, a ton of copper is trading at 7700 USD. As for precious metals, gold offered a nice rebound of 2.20% to 1760 USD.

Agricultural products: Ukraine and Russia have signed an agreement on grain exports to Turkey, a step forward which should allow Ukraine to ship its wheat from the port of Odessa. On the other hand, a Russian bombardment on this same port last weekend revived concerns about the respect of this agreement. Wheat prices thus recovered in Chicago, to 8,036 cents a bushel. |

|

| Macroeconomics |

Vibe : Don’t throw any more. The week was rich in macroeconomic events: Fed rate hike, second quarter GDP and the latest inflation figures in the United States and the euro zone… is that the slack in the US economy was rather well received by investors…because they saw it as a valid reason for the Fed to slow down its rate hikes. The US central bank had, shortly before, raised its rates by 75 basis points as expected, remaining determined to combat rising prices. For the rest, inflation was higher than expected in the euro zone in July (estimated 8.9% over one year). We therefore remain in a configuration where the central banks seek to curb inflation without causing the economic dynamic to waver (too much), or sinking into stagflation. A real balancing act.

Rate : The second consecutive quarter of (modest) contraction in the US economy caused US bond yields to ease. The 10-year fell back to 2.7%, because investors slightly lowered their expectations of the aggressiveness of the Fed in terms of rate hikes. The shorter maturities (6 months, 2 years and 5 years) are always better remunerated than the 10 years, given the economic slowdown at work. In Europe, the German Bund stands at 0.89% over 10 years, the French OAT at 1.45% and Italy at 3.10%.

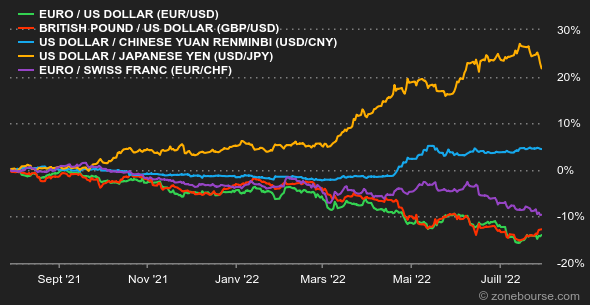

Currencies : The euro came back around USD 1.02 after breaking the parity threshold in the middle of the month. An improvement based on comments deemed a little more accommodating than expected by Jerome Powell on the sidelines of the announcement of the rate hike this week. On the other hand, the single currency has recently suffered against the Swiss franc (at 0.9741 CHF) and the pound sterling (at 0.8401 GBp for 1 EUR). “Short-term rates will rise in Europe, but the ECB is really between a rock and a hard place“, recalls Nordea, which means that the potential for rate increases is always higher across the Atlantic than on the old continent.

Cryptocurrencies : For the second week in a row, crypto-assets continued their ascent in the wake of US stock indices. Bitcoin is back above $23,400 and ether above $1,650 at the time of writing. Note that ether has clearly outperformed bitcoin since the beginning of July, posting +56%, its best monthly performance since January 2021, against +18% for the market leader. Caution is still required with macroeconomic conditions that are not really favorable for a definitive return of capital to risky assets.

Calendar : The first week of August will be marked by several statistics on the labor market in the United States. The JOLTS survey of job openings (Tuesday), weekly jobless claims (Thursday) and June employment data (Friday). On Thursday there will also be the Bank of England’s decision on its monetary policy and two activity indicators in the United States, the manufacturing ISM (Monday) and the services ISM (Wednesday). |

|

|

| Items of the week | ||||||

|

| *The weekly variations of the indices and stocks displayed on the dashboard relate to the period from Monday when the respective markets open to Friday when this newsletter is sent. The weekly variations of raw materials, precious metals and currencies displayed on the dashboard relate to a period over 7 rolling days from Friday to Friday until the sending of this newsletter. These assets continue to trade on weekends. |

Zonebourse.com 2022