Split payment, release of savings, credit… Many solutions exist to avoid falling into the spiral of bank overdraft. However, it is better to react before it is too late.

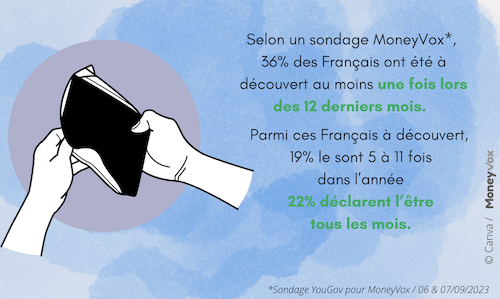

More and more French people being discovered? According to a YouGov survey carried out at the beginning of September for MoneyVox, 77% of people who have already been overdrawn believe they have been overdrawn more regularly over the last 12 months. And unfortunately, the shift into the red seems to be repeating itself. Among those surveyed, 29% estimate that they are discovered 3 to 4 times a year, 19% are discovered 5 to 11 times, and 22% even claim to be discovered every month.

The problem is that not all French people have an overdraft authorization. And the amount of unauthorized overdraft increases significantly. People overextending are thus on average 317 euros in 2022, compared to 284 euros in 2021, or 11% more than last year, according to a study by Panorabanque published last year.

A discovery that can be very expensive

When it is authorized, the overdraft risks costing you a few euros in interest charges (the famous agios). If you exceed the limit agreed with your bank, on the other hand, the bill goes off very quickly. Because the bank will also invoice, for each operation occurring on the account in the debtor position, an intervention commission. These can reach 8 euros per rejected operation, within the limit of 80 euros per month. Sending a letter of information for an unauthorized debtor account, rejection fees if a direct debit is refused… The bill can very quickly increase and push a customer already in difficulty a little further.

An overdraft is expensive, and it is dangerous, because if a direct debit does not go through, this will result in letters being billed. There are a lot of things that can pile up and it can happen quite quickly. There is a lot of bank charges which can be added and put people in even more difficulty, explains Pauline Dujardin, lawyer and spokesperson for Crsus, a network of associations fighting against over-indebtedness.

Example of fees that may arise in the event of an overdraft

Mr. X has an authorized overdraft of 200 euros. At the end of the month and having only 4 euros left in his account, he has to pay 400 euros to the mechanic because of a mechanical problem with his car. He therefore found himself in a deficit of 396 euros, including 196 euros of unauthorized overdraft.

From there, Mr. In certain cases, for authorized overdrafts and if you have a group offer from your bank, your advisor will not charge you interest. But the establishment can, conversely, charge interest in the event of an authorized overdraft, even if the latter is lower than in the case of an unauthorized overdraft.

In the case of Mr. Exceeding the overdraft will also result in the sending of an information letter for an unauthorized debtor account, billed around 13 euros.

But the difficulties do not stop there. The next day, a check for 55 euros must be cashed by MX’s kin. The latter is refused by the bank. At the same time, a direct debit of 13 euros, corresponding to a telephone bill, is also refused. For these two operations, MX will therefore have to pay 50 euros for check rejection fees and 13 euros for direct debit rejection fees for lack of funds.

Worse still, MX will now be registered with the FCC, the central check file. He is therefore now prohibited from issuing checks until his situation is regularized. In total, MX will therefore have to pay 81 euros, not counting the premiums.

If you are already overdrawn, the first thing to do is to call your bank as soon as possible, to negotiate a staggered reimbursement. If you are uncovered too often, it means that your salary does not cover your expenses. If you are unable to pay your charges, things risk getting worse, so you should not hesitate to quickly file an over-indebtedness file, assures Pauline Dujardin.

Split payment, a parsimonious solution

It is best to avoid being discovered at all costs. But then, how to do it? It all depends on the origin of the bank overdraft, explains Pauline Dujardin. However, several solutions can be implemented. In the case of a one-off overdraft, linked to an unexpected expense for example, it will always be better draw from your Livret A or in available savings, than risking a payment incident.

Overdrawn bank account: do you have to dip into your Livret A to get out of the red?

Then, the most important thing remains to make your budgetand to be aware of one’s remaining life, but also to ensure that never have a major expense when it can be spread over. The overdraft can be due to charges which are not monthly, reveals the Croesus lawyer. It’s necessary always think about monthly payments to avoid being in difficulty for a month.

In the same vein, the split payment could be a real solution. It’s very practical for people with a small budget, who need to make a big expense, on household appliances for example, confirms Pauline Dujardin.

These split payment solutions are widely developed in France, agrees Marc Lanvin, deputy general director at Floa. When it comes to a purchase of a certain amount, most players offer payments in three or four installments, with or without fees. This can help cover an unexpected expense.and gave control to the client, both over the duration, which can be controlled, and over the costs which are fixed.

Difficult, moreover, to multiply split payments in a reckless manner, according to Marc Lanvin: We question the FICP every time (file of individual loan repayment incidents, Editor’s note) to ensure that the client is not over-indebted. We also have algorithms that allow a fairly detailed analysis of the situation to estimate whether the customer has the capacity to make this payment. Finally, we also ask the bank if the customer can pay the first payment, which corresponds to 25% of the amount. We therefore have several lines of control.

Pay attention to your rest

Finally, Floa launched the buy now, pay whenever concept a few months ago.(buy now, pay another day, editor’s note), which allows you to use split payment days or even weeks after having paid for your purchase in store or on an e-commerce platform. This allows the customer to pay for their purchase when they need it, but to repay the amount when he can, develops Marc Lanvin. A solution which can, once again, help avoid getting into the red in the event of an unexpected difficulty. Be careful, however, because this is a mini-credit, therefore paying approximately 2% of the purchase according to Floa.

But you have to be very careful and have a real vision of your budget because otherwise, it can still put you in difficulty. You cannot make split payments for everyday purchases, such as shopping, for example. This really means that there is something wrong, you have to be aware of it and not hesitate to get help, advises Crosus.

Another possibility for anticipating a large expense, salary advance requests. This is the solution offered by Spayr, which allows employees to access a fraction of their already earned remuneration during the month. And the model is popular, since according to the company, the average amounts of deposits released by employees jumped by 66% between the months of June and August 2023 and the same period in 2022. Thus, in 2022, the average deposit used was 123 euros compared to 205 euros in 2023. Again, if the request for a salary deposit can be a one-off solution, it cannot become a solution taken at the risk of facing other difficulties in the future.

Finally, last solution, if the expense is planned in advance: take out a loan. It will always cost less than an overdraft, confirms Pauline Dujardin. But here again, a credit binds you and must be repaid. The most important thing therefore remains tohave a good vision of your monthly budget and your remaining livingto avoid disappointment as much as possible.