MONEYVOX INFO. Since the launch of the Ciclade forgotten asset recovery platform in 2017, more than 100 million euros have been returned almost every year to individual customers. But the banks continue to supply Ciclade abundantly. Another 366 million euros for 620,000 inactive bank accounts in 2023!

Livret A, LDDS, youth savings account, current account, home savings plan, etc. All “pure” banking products, to be distinguished from insurance products (life insurance, retirement savings plan, etc.), are grouped in the “pure” category. Bank accounts ” on Ciclade.fr, the Caisse des Dépôts platform which since 2017 has allowed you to search for your savings forgotten in an old bank account. Or looking for money that should have come to you via an inheritance but for which neither the notary nor the bank or insurer has managed to make the link with your identity and address.

When does your money go to the Caisse des Dépôts?

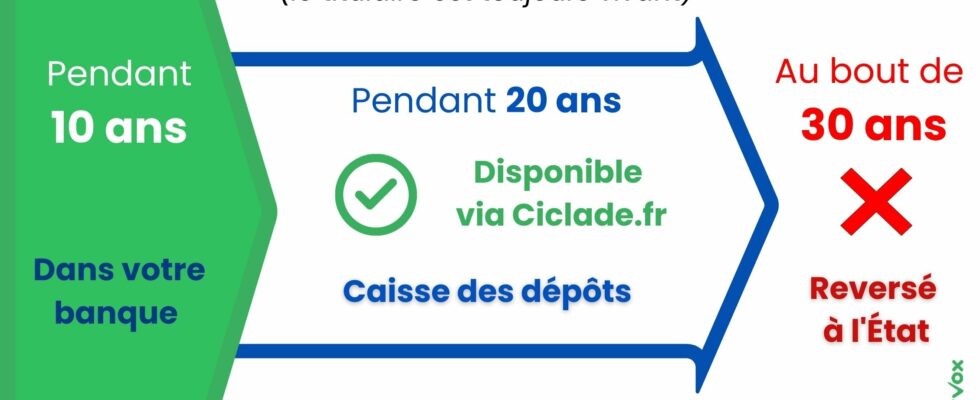

In a bank, an account or savings account is not categorized as inactive right away. Your current account is considered as inactive after 1 year without any movement or sign of life, on this account or another held in the same bank. For a savings account, inactivity is recorded after 5 years without any sign of life.

Once your bank account, your savings account or your PEL is considered inactive and unclaimed, your bank is then supposed to activate to let you know. Banks are thus obliged by law to inform account holders (or beneficiaries) of the inactivity of accounts, to limit account maintenance costs, to inquire about the possible death of its customers, etc. ., and finally to transfer the unclaimed sums to the Caisse des Dépôts et Consignations (CDC) after 10 years of inactivity. It is therefore only after 10 years and once transferred to the CDC that your money can be searched on Ciclade.fr.

Inactive bank account: what the law provides

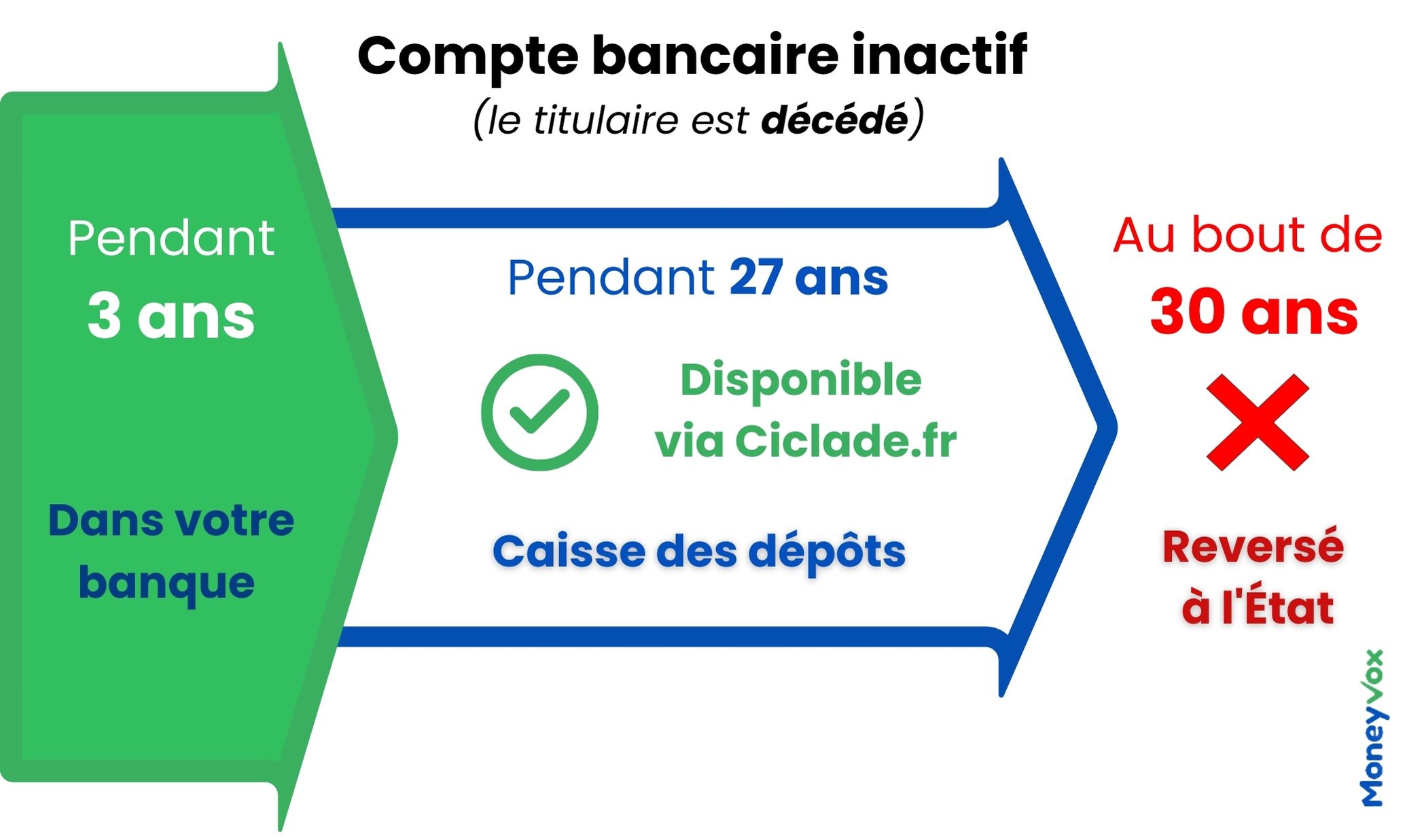

In case of death of account holder, the timetable accelerates: the account or investment is immediately considered unclaimed if the bank or insurer does not identify the beneficiaries (and they do not come forward). And he only remained in the bank for 3 years, before being transferred to the Caisse des Dépôts.

Abandoned bank or savings account: how much money ended up in the state coffers?

Nearly 60% of the sums transferred to the Caisse des Dépôts come from banks

More than 7 years after the launch of the Ciclade platform, the counter of sums returned to individuals who come forward via this portal climbs regularly, every year. Enough to empty this incredible envelope of “forgotten” money? No. Because the flow of inactive accounts, company savings plans and unclaimed life insurance contracts is not slowing down.

After the billions transferred when the service opened, banks and insurers continue to supply Ciclade every year. 632 million euros had been transferred in 2022, including 404 million euros from banks. In 2023this annual flow is almost similar: 590 million euros overall, including 366 million euros from inactive bank accounts.

| Bank accounts (booklet, current account, PEL, etc.) | Life insurance | Employee savings | |

|---|---|---|---|

| Number of accounts and contracts transferred | 620,000 accounts | 50,000 contracts | 80,000 company savings plans |

| Amounts transferred | 366.47 million euros either 62% amounts transferred in 2023 | 106.14 million euros either 18% amounts transferred in 2023 | 117.82 million euros either 20% amounts transferred in 2023 |

| Average amount per transferred account | €587 | €2,143 | €1,441.50 |

Source: Caisse des Dépôts.

How can we explain that the banks also provide the Caisse des Dépôts abundantly? Certainly, the fact that they transfer more accounts, in number, is quite logical: an individual will easily combine bank account, booklet A and PEL, for example, for a single life insurance contract. But the life insurance jackpot is such, in France, at 1,923 billion euros, that this savings product outperforms all others in volume. The Livret A and its 418 billion euros is small compared to life insurance. So how can we explain that life insurance is not on par with inactive bank accounts in terms of “forgotten” money transferred to the Caisse des Dépôts?

“The fact that there are more inactive accounts transferred than other non-bank savings products is largely explained by their higher number”

The Caisse des Dépôts has no explanation. Requested by MoneyVox, the French Banking Federation (FBF) gives us the following arguments: “In France, there are more than 170 million current accounts and banking products (livrets A, LDDS, LEP, PEL) which are held by customers banks. French banks, as part of the application of the Eckert Law, identify each year inactive accounts or banking products which they transfer to the Caisse des Dépôts according to the terms provided for by law. The fact that there are more inactive accounts transferred than other non-bank savings products is largely explained by their higher number and the work carried out by establishments to identify them. »

On the life insurance side, certain establishments have suffered heavy fines due to lack of sufficient research to identify the beneficiaries. Constrained and forced, insurers have had to improve their practices in finding beneficiaries… And insurers have long brought together their efforts via the Agira associationwhich lists searches for recent deaths (before the 10 years prior to transfer to the Caisse des Dépôts) for all insurers.

As long as the flow of inactive bank accounts is so significant, the Ciclade system will always have a bright future ahead of it.

| Bank accounts (booklet, current account, PEL, etc.) | Life insurance | Employee savings | |

|---|---|---|---|

| Number of accounts and contracts transferred | 10.5 million accounts | 950,000 contracts | 700,000 company savings plans |

| Amounts transferred | 4.96 billion euros either 59% amounts transferred since 2016 | 1.86 billion euros either 22% amounts transferred since 2016 | 1.59 billion euros either 19% amounts transferred since 2016 |

| Average amount per transferred account | €470 | €1,953 | €2,069 |

Source: Caisse des Dépôts.