Are you about to buy a property and go through a loan from an online bank or a neobank tempts you? We explain what you need to know before you start.

In the collective imagination, online banks and especially neobanks (N26, Revolut, Orange bank, Bunq, etc.) are above all designed to provide a secondary or backup account, practical in the event of glitches. money or specific needs that traditional banks simply cannot provide. We are thinking in particular of neobanks accessible without conditions, practical for people in a situation of banking bans, such as Nickel or Lydia, or those which promise better advantages for travelers such as Revolut, Vidid Money or Bunq.

There is however a point on which these banks have a weakness by their nature, it is the question of services, loans and particularly real estate loans. In the majority of cases, in France, a mortgage is taken out with a bank, ideally with its regular bank. But what is the point of subscribing to a mortgage with an online bank or a neobank? Which ones offer it? Under what conditions and is it ultimately a good idea?

What are the financial criteria for subscribing to a mortgage?

The basis of a mortgage is the debt capacity. The bank must be able to be certain that a borrower can collect debt over time without being in difficulty. If we talk about figures, it is practically impossible to devote more than 35% of your income to reimbursements, a rule imposed by the High Council for Financial Stability (HCSF), the body that regulates credit in France. In the vast majority of cases, banks calculate this possibility of indebtedness from the net salary before tax and do not take into account your possible tax advantages.

Real estate credit: online banks VS neobanks

The big structural difference between an online bank and a neobank is the provision of a banking license. The latter is essential to offer personal loans, real estate, but also overdrafts on the current account.

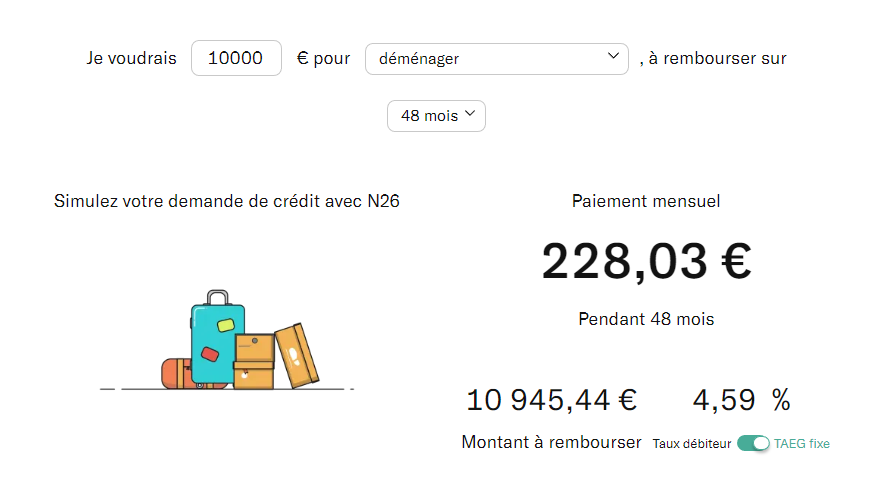

Online banks are mostly beneficiaries of solid financial institutions, most often from a traditional bank. They are therefore able to offer credit-based banking products with the potential for indebtedness. By their nature, neobanks generally choose to opt for an easy-to-access banking license, which is also the least expensive and the least restrictive and may even call on service providers to manage service provider flows. We can for example think of brands like Vivid Money or Helios which are dependent on BaaS (Bank As A Service) Solarisbank which offers turnkey banking solutions. The counterpart is that, in the eyes of French law, these establishments are only considered as payment establishments. As such, credit in all its forms, even for an overdraft, is strictly prohibited. However, they can also call on service providers to take care of the credit part, such as N26, which has partnered with Younited Credit to offer loans to be repaid over 12 to 84 months. Please note, this is in no way comparable to a real mortgage, the amounts and conditions of which are much more regulated.

If we dwell on the side of online banks, the main difference with a traditional bank concerns the management of financial services. As they do not have a physical agency, it is inevitably impossible to meet a financial adviser. Everything is managed online by phone or email or instant messaging. On this point, they tend to attract borrowers better, since they tend to offer cheaper financial services, faster and more efficient customer follow-up. It is very easy to exchange and communicate with an online bank unlike traditional banks which are only open during office hours. And this is precisely the weakness of online banks in the context of a mortgage. If you want a local service and in particular to speak to an advisor, the traditional bank is more suitable. Also, conventional banks are less restrictive and accept more complex real estate projects. Depending on the profile, which will be much more complex to obtain from an online bank.

So, shall we sign?

As with each type of loan involving large sums of money, it is better to ensure that you can count on a maximum of guarantees. If we talk about online banks, the offers seem attractive, but each of them offers special conditions that can have an impact on your budget. As part of a mortgage, the application fees are generally low and sometimes even offered, unlike traditional banks. The rates are also very attractive and negotiable in the event of direct debit of income with the lending bank, which therefore includes the fact of having to choose an online bank as the main bank. Another advantage is that online banks allow you to manage all your banking operations via their applications, including credits and loans.

The main disadvantages relate precisely to real estate loans. Online banks have fairly restrictive conditions and the offers mainly concern conventional home loans. So don’t expect to rely on complex financing plans for your future luxury real estate portfolio.

Note also that it is mandatory to be a customer to take out a mortgage with an online bank. The majority of them offer minimum loan offers between €50,000 and €100,000. Then, they rarely accept loans for rental investments, the construction of a house and the acquisition of new off-plan housing. It is the same for loan buybacks, bridging loans and zero rate loans which are not accepted by all.

On the side of neobanks, the subject is less complex. Rare are those who offer mortgages in their offers. Some, like N26 or Revolut, provide consumer credit for a car, equipment or cash needs, but that’s where it ends. The only neobank to have entered this market is French and it is Orange Bank. Inevitably, itself tinkered with the remains of Groupama Banque, it has traditional banking experience in addition to a license allowing it to offer this type of product. On the other hand, it seems that it is no longer possible to take out a mortgage today, the bank preferring to focus on more traditional consumer loans.

Want to join a community of enthusiasts? Our Discord welcomes you, it’s a place of mutual aid and passion around tech.