The equity markets went through all the emotions yesterday, with only one real constant: there is great confusion in the minds of investors. In Europe, the most cyclical indices took the upward slope, which earned the CAC40 a rise of 2.5%. The Swiss SMI, much more defensive with its aristocrats such as Nestlé, Novartis and Roche, only gained a few points. It must be said that the juggernaut Roche suffered a rare correction after experiencing a setback on a very promising drug candidate.

In the United States, the situation has been interpreted quite differently. The fault with the publication of an inflation of April in slight fall certainly, but always in weightlessness. If there is a price drop, it may be desperately slow. Therefore, the Fed may have to act longer to regain control of operations. So that increases the risk of a central bank blunder. So the scenario of an economic soft landing is weakened. Because if you followed well, we went in a few weeks from a “anyway, inflation is transient, growth is strong” has a “either way, the fight against inflation will lead to sluggish growth at best, recession at worst“. Race report last night, the Nasdaq lost 3%, while the more defensive Dow Jones dropped 1%.

In such an environment, investors sometimes look like headless ducks. It must be said that the sanctions seem to fall a little randomly on the actions according to the moods of the moment. With one constant all the same, the systematic demolition of technological stocks whose valuation was extravagant. When the follies come to an end, they can only explode in sound and fury. Especially when big financial interests are at stake. Look at those stocks, look at the cryptocurrencies, look at the NFTs. None of this is a bad idea per se, but the speculative ecosystem can corrupt any fad-like concept. Especially when the money was free and flowing like it had been for a good dozen years. You will find below the course of the ARKK Innovation investment fund, a concentrate of madness and good ideas. It is compared to the Berkshire Hathaway fund, which is more of a conservatism temple. The first loses more than 60% in 2022, when the other is in positive territory. A quarrel between the ancients and the moderns revisited.

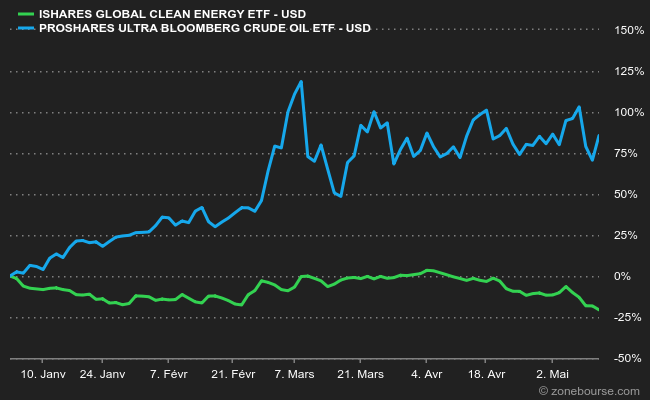

Not all the craziness is purged – it never is – but we are definitely entering a more sober economic era, by force of circumstance. We will have to adapt and start counting more seriously again, because the cornucopia of global “whatever it takes” is disappearing. Everyone knew it. But it’s easier to realize that the door closes when you take it in the face. And I am not even going into this morning, for lack of time, a paradox which is probably one more madness: if some investors are doing so well, it is because they have massively repositioned themselves on fossil fuels. I put a second graph, which compares an oil ETF and a clean energy ETF since the 1er january. We’ll talk about that another time.

This morning, the European markets will correct because of the large gap with the US close. There is a differential of more than 5% between the CAC40 and the Nasdaq. On the Asian and Pacific markets, the declines range from -1.65% in Sydney to -0.1% in Shanghai. In China, the 4and The country’s promoter, Sunac China, defaulted on a bond but the market seems to have other fish to fry at the moment. North Korea has recorded its first “official” cases of covid, leading to containment measures that we imagine to be rather tough, given the regime’s standards. There are still quite a few corporate earnings reports, which show good earnings but all of which mention price increases and geopolitical tensions as factors of instability. The publication of US producer prices for April, at 2:30 p.m., will bring grist to the mill of the debate on inflation.

Economic highlights of the day

In the United States, the weekly jobless claims and the producer price index will be published at 2:30 p.m. All the “macro” agenda here.

The euro/dollar pair is holding around USD 1.0518. An ounce of gold trades at 1858 USD. Oil rebounded yesterday, with North Sea Brent at $106.15 a barrel and US WTI light crude at $103.09. The yield on US 10-year debt fell further to 2.89%. Bitcoin drops back to $27,800.

The main changes in recommendations

- Boliden : Deutsche Bank goes from sell to hold targeting 380 SEK.

- Credit Suisse: Jefferies remains to be kept with a reduced price target of 7.30 to 6.90 CHF.

- Genmab: Jefferies remains to be held with a price target reduced from 2500 to 2350 DKK.

- Lanxess: Berenberg remains long with a price target reduced from 67 to 54 EUR.

- Meyer Burger: UBS goes from buy to neutral, targeting CHF 0.46.

- Nel: Citigroup goes from buying to neutral, aiming for 14 NOK.

- Nordea: AlphaValue shifts from lightening to accumulating aiming for 107 SEK.

- Roche: Julius Bär reduces his target price from 400 to 360 CHF.

- Royal DSM: Jefferies remains to be kept with a price target reduced from 168 to 161 EUR.

- Seb: AlphaValue remains long with a reduced target price of 147 to 144 EUR.

- SSE: Berenberg goes from holding to buying, aiming for 2200 GBp.

- ThyssenKrupp: Jefferies remains long with a price target raised from 12.65 to 13.25 EUR

- UBS: Jefferies remains long with a price target raised from 22 to 24 CHF.

- Victrex: Jefferies remains to be held with a price target reduced from 2100 to 1860 GBp.

- Wendel: AlphaValue remains long with a price target raised from 123 to 142 EUR.

In France

- Bouygues: the annual forecasts are confirmed, barring further deterioration in conditions.

- Ubisoft: the software publisher should generate €400 million in operating profit for the 2022/2023 financial year.

- Veolia: the group also confirms its forecasts after sharply rising Q1 results.

Important (and less important) announcements

- STMicroelectronics publishes its medium-term objectives during an investor day: by 2025-2027, the group is targeting $20 billion in annual revenue, a gross margin rate of around 50% and an operating margin of over 30% .

- Renault confirms its intention to list its electric activities separately in 2023, probably with the presence of Nissan and Mitsubishi Motors in the capital.

- Emirates will receive its first Airbus A350 in August 2024.

- Eiffage and Vinci only obtained 2.2% of the capital of the Société Marseillaise du Tunnel Prado-Carénage, whose minority shareholders were up against a takeover.

- Hydrogène de France announces the launch of the HyShunt project for the development of the first French hydrogen shunting locomotive.

- NFL Biosciences obtains a patent in South Korea.

- Bone Therapeutics enters into exclusive talks for a proposed reverse merger with Medsenic.

- Bénéteau, Colas, SII, Neurons, Chargers, Parrot, AirwellEutelsat, Altamir, Neurones, Jacquet Metals, Genfit, Fermentalg have published their accounts.

In the world

Company results

- Allianz: maintains its operating profit target for the full year.

- Hapag-Lloyd: the group generates exceptional profits in Q1.

- Merck KGaA: profit in the first quarter of 2022 increased by 18.2%. Organic growth is expected between 6 and 9% this year.

- Siemens: the group will take a charge of €600 million for the closure of its activities in Russia.

- Telefonica: Q1 results are above expectations.

- The Walt Disney Company : the number of subscribers to Disney+ is higher than expected, but the results are at half mast.

- Zurich Insurance: 2022 targets will be exceeded.

Important announcements (and others)

- The capitalization ofAramco exceeds that of Apple.

- Vodafone is reportedly negotiating a merger of its UK business with local rival Three UK, reports the Financial Times.

- Google extends its offer of connected objects.

- Promoter Sunac China in default on a bond.

- The SEC is investigating how Elon Musk built his initial position in Twitter, according to the WSJ.

- The Boeing Company is struggling to produce B737MAXs due to parts shortages.

- Anglo American returns to Zambia with Arc Minerals copper deal.

- Walgreens Boots Alliance sells 6 million shares of AmerisourceBergen for $150 per share, reducing its stake from 28.1% to 25.2%.

- Instacart prepares its IPO on Wall Street.

- Main results publications of the day: Siemens AG, Allianz, Merck KGaA, Hapag-Lloyd, Zurich Insurance, Verbund, Telefonica, KBC, Veolia, Atlantia, CNP Assurances, Fortum, Nexi… The whole agenda here.

Readings