The latest developments

The most important answers to the crisis surrounding the Chinese real estate group Evergrande.

The Evergrande headquarters in Shenzhen, China.

The latest developments

- Troubled real estate developer Evergrande is facing for the first time local creditors who have refused to extend the payment period for a bond. The decision concerned a yuan-denominated bond issued by Chinese Evergrande division Hengda Real Estate, which wanted to extend its payment deadline by six months beyond July 8. The refusal was communicated by mandatory notification via the Shenzhen Stock Exchange. “This is the first time Evergrande has failed to roll over an onshore bond, which would mean a default,” said Li Kai, CIO at Beijing Shegao Private Equity Fund Management.

With more than $300 billion in debt, Evergrande is the most indebted real estate developer in the world. After sales had plummeted in recent months, the Chinese group was unable to pay several interest payments that were due.

In mid-September 2021, the editor-in-chief of the state-affiliated newspaper “Global Times” wrote that the company’s bankruptcy did not pose a systemic risk for the Chinese economy. A government bailout therefore seems unlikely.

Shortly thereafter, angry private investors and customers of the company stormed the company’s headquarters in Shenzhen and demanded their money back. About 1.5 million houses and apartments have already been paid for but not yet built. The buyers are afraid that they paid their deposit in vain.

The Chinese leadership is regulating more and more economic sectors and areas of life, such as gaming, the tech sector and, most recently, the gambling industry. The real estate industry has also fallen victim to government intervention after years of state protection.

The construction boom is an important pillar of the economy; the real estate sector has an estimated share of 29% in Chinese economic output – more than in any other industrialized country.

Huge areas are available to real estate companies for the construction of new apartments. The residential area has quadrupled since 2005. Land sales to real estate companies are the main source of income for most local governments. In China, all land belongs to the state.

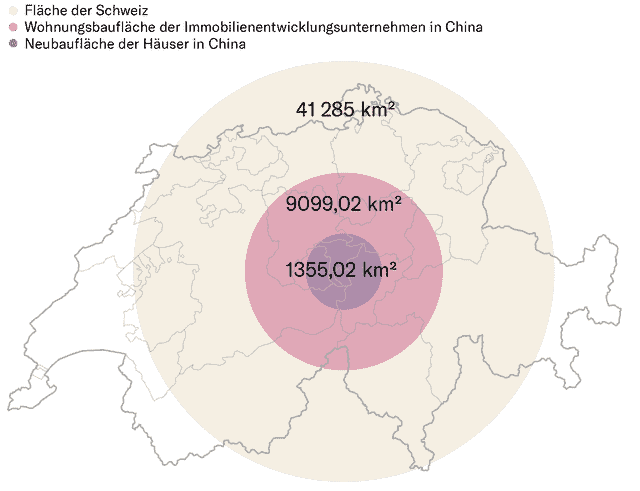

Huge areas are available to Chinese real estate companies

Construction area from January to August 2021, in square kilometers, for comparison the total area of Switzerland

The industry is mainly supported by loans that have largely been issued by state-controlled banks at low interest rates.

Evergrande’s business concept was based on aggressive expansion on credit. Not only were properties sold before they were built, the group also owned a football club, developed electric cars and did banking. Since the end of September, the group has been trying to sell individual areas in order to obtain liquidity.

In order to curb debt and minimize the risk of a crisis, China’s central government decided on “three red lines” for the real estate sector in 2020. In doing so, it limited the issue of mortgage loans, limited the debt ratio of real estate companies and allocated less land for development.

However, the highly indebted real estate groups such as Evergrande depend on consistently high sales in order to be able to settle their liabilities. If cash flow dries up like it is doing now, they’ll be in trouble.

The Evergrande Crisis brings back memories of the financial crisis that began with the collapse of Lehman Brothers in 2008. Evergrande’s liabilities are roughly the same as Denmark’s GDP — or about half the GDP of Switzerland. However, Lehman Brothers had accumulated much higher debts of well over 600 billion.

However, a comparison with other major bankruptcies of US companies shows that an Evergrande bankruptcy would still be one of the largest bankruptcies in history – right after the Lehman bankruptcy.

Due to the size of the real estate sector, Harvard economists assume that the crisis is very likely negative will affect growth in China, although spillover to the banking sector can still be avoided. In addition to the Corona crisis, the turbulence on the real estate market in the current year is one of the main risks for the economy.

Low-rated Chinese bonds have been hit the hardest, while less risky Chinese paper has remained more stable so far. It still seems as if investors are assuming a temporary negative trend, but are ruling out the big crash.

Evergrande has already hired external restructuring consultants to help the company with a debt restructuring. At the same time, it is desperately trying to get liquidity.

Investors have already been offered parking spaces or apartments at extremely low prices should they agree to give up their money. Investors who still insist on cash can only expect a full payout in two and a half years. Evergrande also wants to sell its stake in the e-car business, a building management group and the company’s headquarters in Hong Kong in order to get fresh money.

At the same time, the panic of the collapse has also gripped Evergrande’s executive floor. It became known that six high-ranking managers received an early payment on their investment products. The executives had already liquidated the same investment products for which retail investors cannot currently receive full repayments.

Ultimately, the fate of Evergrande depends on the Chinese government. She has been covered for half a year and is sending signals that make it seem unlikely that she will save Evergrande. The Chinese banks would probably be less affected by a collapse of the group than the many small investors and real estate owners. A financial crisis is still unlikely in the event of uncontrolled bankruptcy, social unrest and discontent are more likely.

In the past, the CP did not allow this to happen and intervened before the crisis escalated. But President Xi Jinping seems serious this time around and wants to subject the real estate sector to market discipline and push home prices down. The question remains as to where the pain threshold lies for the Chinese government and at what level of upheaval it still intervenes.

Without a doubt, Evergrande is the real estate group that is currently in the greatest difficulties. But the difference to other large real estate developers such as R+F and Fantasia is only gradual. They, too, are sitting on huge mountains of debt and massively overvalued real estate. Your bonds are also only trading at a fraction of their face value.

The entire Chinese real estate sector is on shaky foundations. Should apartment prices plummet, that would certainly also be a problem for other groups. At the latest then the state will probably intervene. The communist leadership cannot afford the political risk of a mass movement of cheated and impoverished property owners.