If you were born after 2015, you probably didn’t know that Engie was called something else before. And since you are seven years old, we wonder why you are reading this paper instead of playing Subway Surfers©. Engie is the result of the union and disunion of several companies since the middle of the 19th century. Among them, the Société Générale de Belgique, a bank, then the Compagnie du Canal de Suez, which operated the eponymous canal, the Lyonnaise des eaux, a public network operator and Gaz de France, the gas counterpart of EDF. The merger between GDF and Suez is relatively recent (2008). It also took place shortly after GDF went public in 2005. After the marriage, not really successful in the opinion of specialists and shareholders, two major operations should be noted: the takeover of International Power in 2011 and the final exit from the scope of Suez Environnement (which has just been acquired by Veolia).

After the acquisition of International Power, the perimeter of GDF Suez represented a production capacity, in group share, of 86 GW, with a fairly homogeneous international distribution. This is what it looked like:

Reading: in 2012, 54% of the group’s energy production capacities came from natural gas (Source: 2012 reference document).

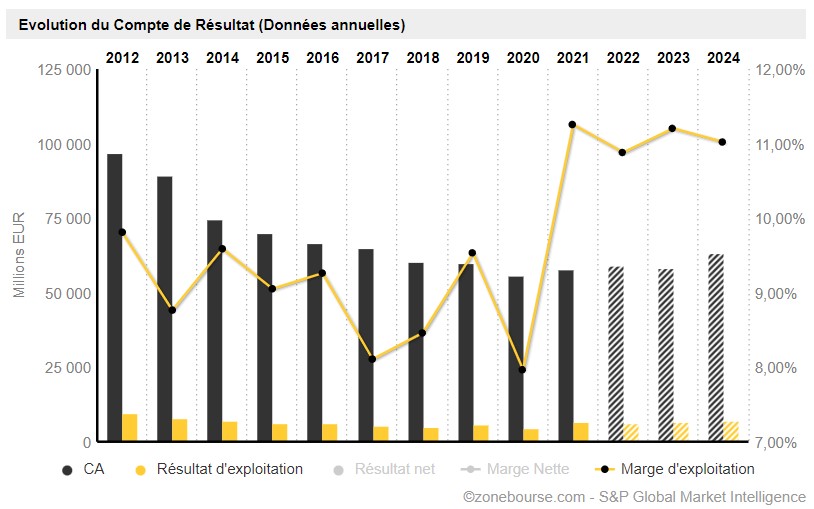

A capricious profitability

In 2012, the group was active not only in energy production, but also in the exploitation and transmission of gas, in network infrastructures and in energy services. He still retained a residual stake in Suez, which was intended to leave the scope. Financial performance has been particularly chaotic since the integration of International Power, as shown in the operating margin trend chart between 2012 and 2020:

Lots of mistakes

How to explain the problems that have befallen Engie? Gossip would say he can only blame himself. The others would find it difficult to contradict the gossips. One could cite the nuclear debacle in Belgium, where the accumulation of technical problems and provisions has burdened activity, to such an extent that the Belgian exit from nuclear power (although recently called into question) is almost good news. One could add the fiasco of the acquisition of International Power, an overpaid British company whose exposure to coal still haunts the scope. We could talk about the quarrels of egos at the controls of the group.

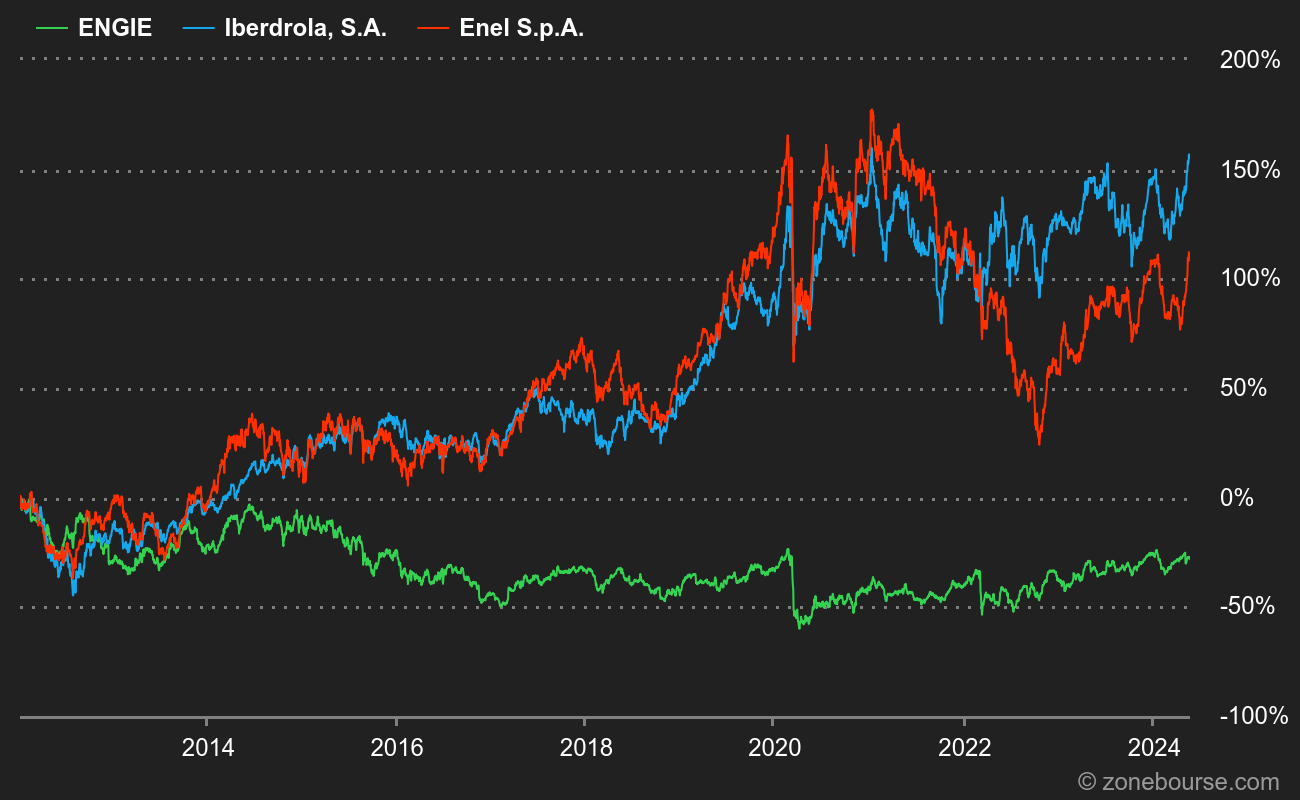

But I think we must also talk about the permanent promise of a greening of the activity with the backing of advertising campaigns, when the reality was very different. By dint of broken promises, investors have stopped seeing the company as an alternative to traditional energy companies. Worse, other players in the sector have started a shift towards renewable energies that Engie has completely missed so far. A very visible fiasco in the stock market journey of the Frenchman against big rivals like the Spanish Iberdrola and the Italian Enel. In 2008, Engie (then GDF Suez) weighed more than €90 billion, more than its two rivals combined. In 2022, Enel and Iberdrola each capitalize more than €60 billion and Engie less than €30 billion.

The journey of Engie, not Iberdrôle since 2012 (humor certified without CO2 emissions)

After yet another upheaval in management, the group has put in charge a duo composed of Catherine McGregor as general manager and Jean-Pierre Clamadieu as president. These two have redefined the perimeter into four branches plus two special entities:

- “Renewables”: glop energies (46% Ebitda margin)

- “Energy Solutions”: decentralized production infrastructures and efficiency services (8% EBITDA margin). Part of the services business (called Equans) is being sold to Bouygues.

- “Infrastructures”: serenity insurance (61% EBITDA margin)

- “Thermal & Supply”: energies not glop, nicely described as “provide balanced and flexible power generation” (40% Ebitda margin).

- There are two separate entities: the Belgian nuclear assets on the one hand (plus some rights held on French power plants) and GEMS, which deals with the supply and optimization of the assets.

Engie has a “net zero” target for 2045 in terms of CO2 and greenhouse gas emissions. The group also intends to phase out coal in 2027. Currently, the installed capacity exceeds 100 GW, including 34 GW in renewables, 60 GW in thermal and 6.2 GW in nuclear. In 2030, renewables should reach 80 GW. By way of comparison, Iberdrola has 60 GW of renewable capacity and is aiming for 95 GW in 2030. At Enel, these figures are 54 and 129 GW respectively.

One last thing: France still holds 23.6% of the capital and 33.2% of the voting rights of Engie. Investors generally view the presence of public authorities in capital with a critical eye.

As you will have understood, Engie ceased to make investors dream a long time ago, scalded by years of broken promises and referral errors with serious consequences. The future looks brighter, if not bright, if we are to believe the financial projections. But it will take a little more to convince the market. So, Engie, Engie, when will the clouds disappear? (a reblochon to be picked up at Zonebourse to the first person who sends me the reference).

“Fallait pas l’invite” identifies companies that are going through a complicated period on the stock market. You never know, they could recover! Latest articles in the section: