Vallourec of course. A few figures to start with concerning the action of the company:

- -99% over 10 years.

- -97% over 5 years.

- -88% over 3 years.

- -66% over 1 year.

Obviously seen from this angle, should not invite Vallourec

I remember that in my young years, coming out of the famous “internet bubble burst“, Vallourec was the “tube” of the years 2003, 2004 and 2005 on the Paris Stock Exchange. May the financial journalist who has not played on words with “tube” and “Vallourec” throw the first stone at me. those who need a reconditioning, the best-selling music in France in 2003 looked like this, Finding Nemo broke cinema records and Harry Potter and the Order of the Phoenix sold out at 1.17 million copies.In short, Vallourec was the stock market must-have at a time when Facebook did not yet exist and when Yahoo and MSN had as much market share in Internet search as Google.

Vincent Bolloré, already on the lookout, had smelled the right shot. The investor had made a very lucrative medium-term round trip, before making a second one a few years later. Subsequently, the beautiful machine went wrong, then everything went from bad to worse. During its prosperous period, Vallourec had been able to rely on a solid economic model that generated cash to ensure its development and take the sector leadership. The first warning shot came from the 2008 crisis, which caused Brent to sink from almost 150 to less than 35 USD in a few months, and investments in the sector with it. But Vallourec had above all followed the movement of the market, before rebounding in concert with it from 2009. The action, however, never regained its 2007 levels, without however demerit.

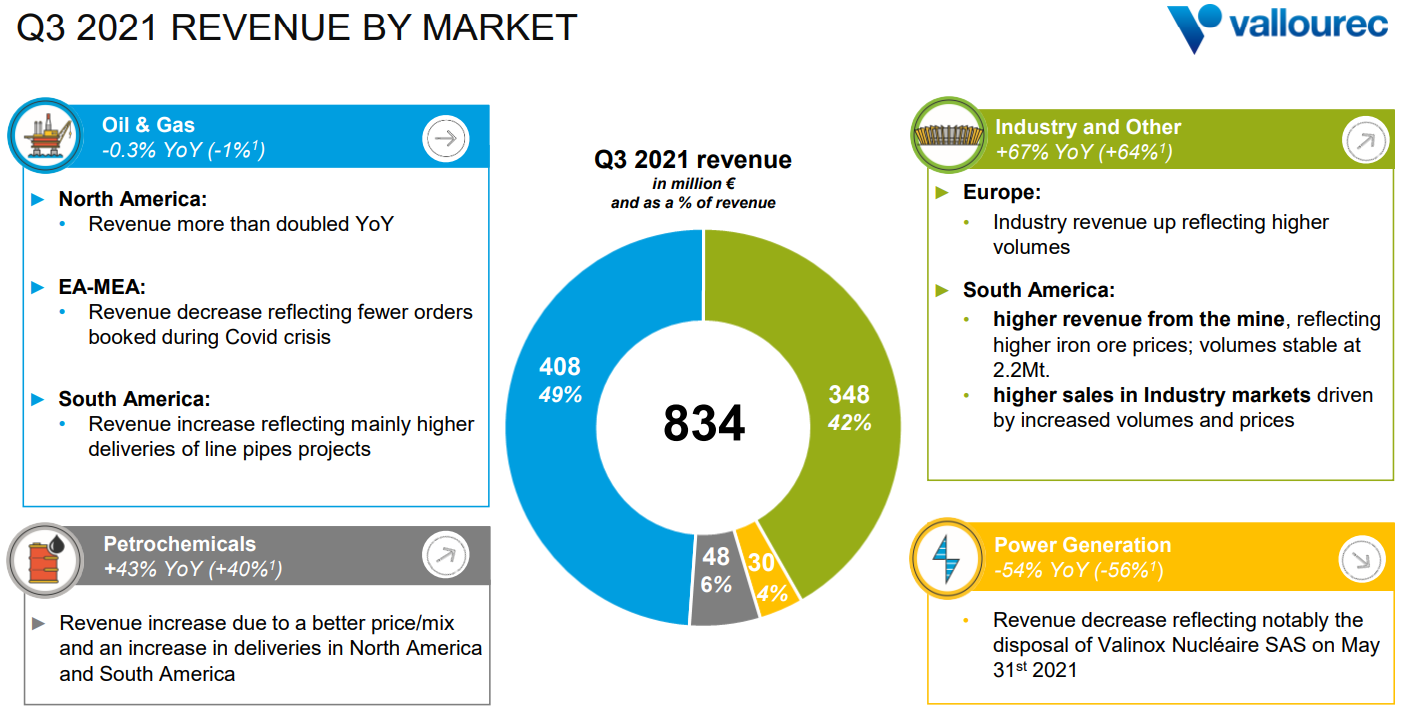

Vallourec generated half of its activity with the oil sector in Q3

An unsustainable debt

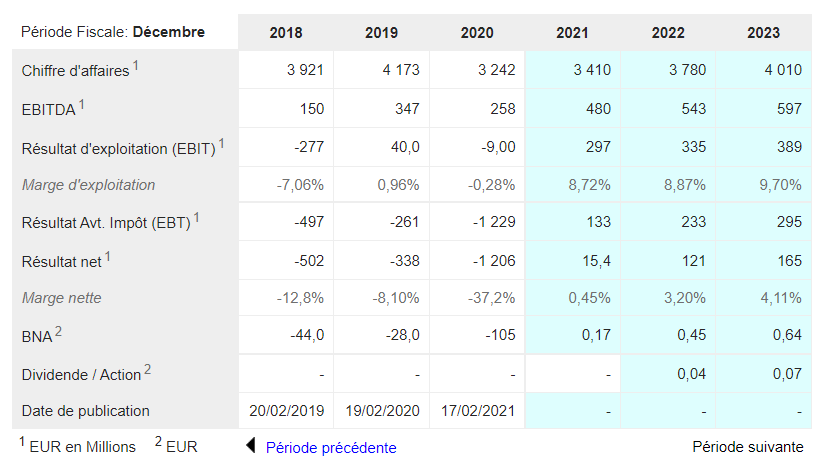

At least until the end of 2011. From this point, Vallourec was considerably indebted. The market became more complicated and more competitive, until the plunge in oil prices in 2014, which again dried up the projects of the majors in the sector and left the entire oil services ecosystem on the floor. The debt quickly became unsustainable in view of the erosion of margins. From €1.29 billion at the end of 2016, net debt rose to €2.21 billion at the end of 2021. In the meantime, Vallourec burned cash despite successive savings plans, and had to rely on convertible bonds and capital increases to ensure its survival. In the past ten years, the company has only been in positive free cash flow twice, in 2014 and 2015.

The recovery in oil prices in recent months, which has put several projects back on track, is a breath of fresh air for Vallourec. But a little late to avoid a new financial restructuring, passed by a classic of over-indebted companies in great difficulty: a conversion of debt into shares, which transformed the creditors of yesterday into main shareholders. Bpifrance and Nippon Steel, which had come to the rescue of the 2016 recapitalization group, were largely diluted after losing most of their stake.

The last of the last

It is now said that the company’s balance sheet is more in line with its financial structure. This is not the first time that shareholders have heard this little music. Others have also heard it on issues such as CGG, another flagship French oil services company which owed its survival only to a multiplication of fundraisers until the shareholders were flushed out by a conversion of debt into capital. Investors are scalded by the disappointments and talk of the ultimate financial restructuring, “the last of the last before the return to normal“.

If all goes well, Vallourec could become a “normal” company again. If all goes well (Source Zonebourse / S&P Capital IQ)

If we are to believe the projections of the eight analysts who are still following the file, free cash flow could return to equilibrium this year. And the PER could become correct again in 2023. If everything goes as planned of course. To remain competitive, Vallourec has greatly reduced its industrial footprint in Europe (the German rolling mills are in the process of being sold or closed), optimized its export capacity from China and Brazil and increased its control over its North American assets. . In the end, the Brazilian workforce should soon represent 45 to 50% of employees.

“Fallait pas l’invite” identifies companies that are going through a complicated period on the stock market. You never know, they could recover! Latest articles in the section: