The context: a rally without excess to end a good year

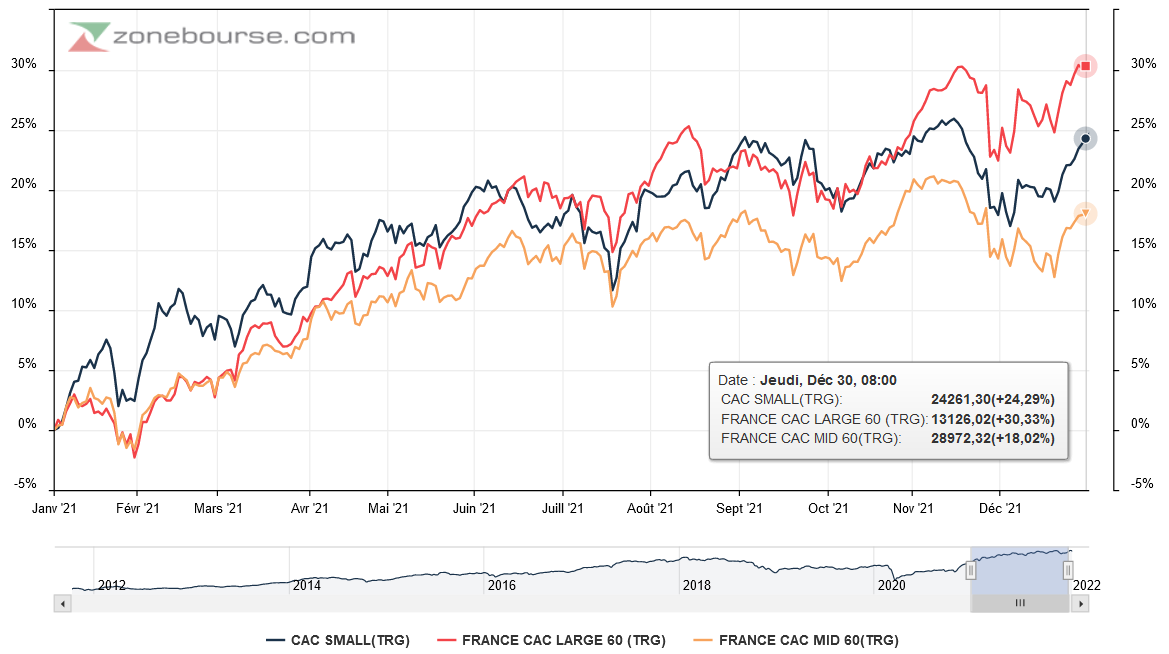

The month of December amplified the annual trends observed for small caps, namely a sustained increase, although less than for large caps. The French index, the Small 90, and the European index, the MSCI EMU Small Cap, both ended the year at +23%.

Source: Genesta, Euronext

In a column published on January 5, 2022, Amiral Gestion’s nugget researchers recall the interest of this market segment:

- Higher growth potential and better alignment of interests : easier to grow when you’re small, low follow-up by analysts, alignment of the manager’s assets with the company’s long-term value creation;

- Attractive valuations and possible catch-up : 20% capitalization/equity ratio discount compared to large caps, valuation in line with their historical average vs 20% premium for large caps while small caps outperform over the long term;

- An investment that makes sense in terms of employment and regional support : “SMEs and ETIs indeed create seven times more jobs in France than large groups” points out Amiral Gestion, adding that “by positioning themselves on this segment of the stock market, investors engage in the financing and development of the real and local economy, support employment in France, industry and services in the regions”.

Investor in this segment of the rating for more than 20 years, I fully subscribe to this analysis, adding that investing in what you understand avoids many errors of assessment. However, proximity to the company, its products, its leaders, its language of communication, its network of customers and suppliers, etc. enriches the quantity and quality of information available. However, information is the key to investing as you know it as readers of Zone Bourse.

Will 2022 be, as we hear almost every year, the year of stock-picking, value, and small caps? I would say yes, and maybe even with more conviction this year. But for this, the resumption of inflows into small and medium-cap funds, penalized in 2021 by the attractiveness of index management and the lack of SRI certifications for SME funds, will be decisive.

Evolutioncapitalized dividends, French equity indices by capitalization size in 2021

It should be noted that over 5 years, when dividends are included, French large caps (CAC LARGE 60 TRG index) beat the small (CAC SMALL TRG) and mid-cap (CAC MID 60 TRG) stock indices.

Evolutiondividends included, equity indices by capitalization size for 5 years: the big ones win

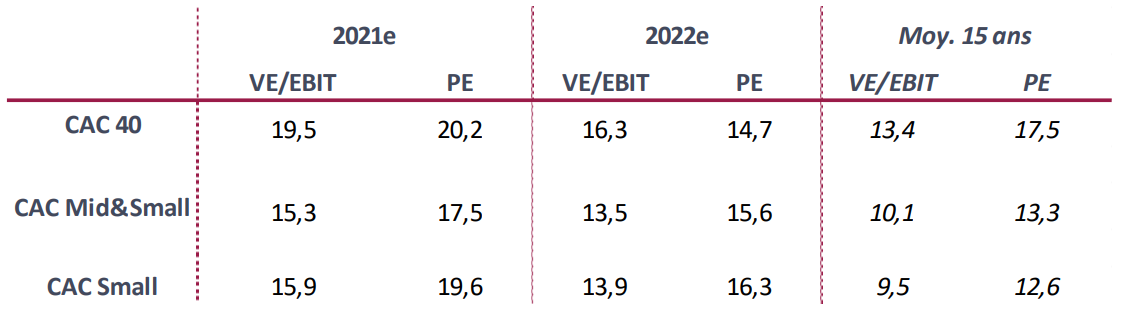

In terms of valuations, the table below shows reasonable valuation multiples for French small and mid caps over 2022. visible growth stocks whose multiples often exceed 50.

Median valuation ratios (Source: Genesta and InFront as of December 31, 2021)

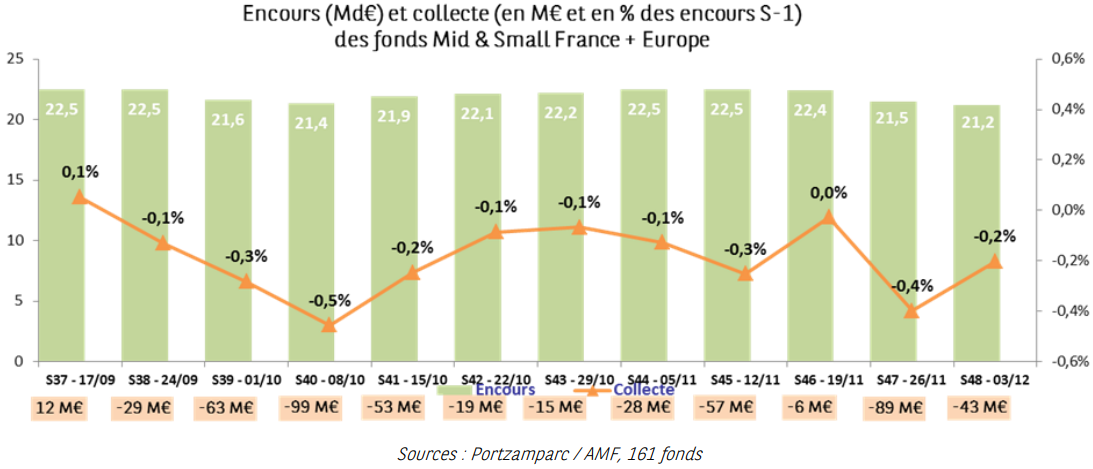

Concerning the evolution of outstanding funds linked to inflows/outflows, the data provided by Portzamparc confirms a slight outflow in the small caps compartment, which does not favor the performance of the asset class while the primary market, characterized by a record number of IPOs this year, captures part of the flow.

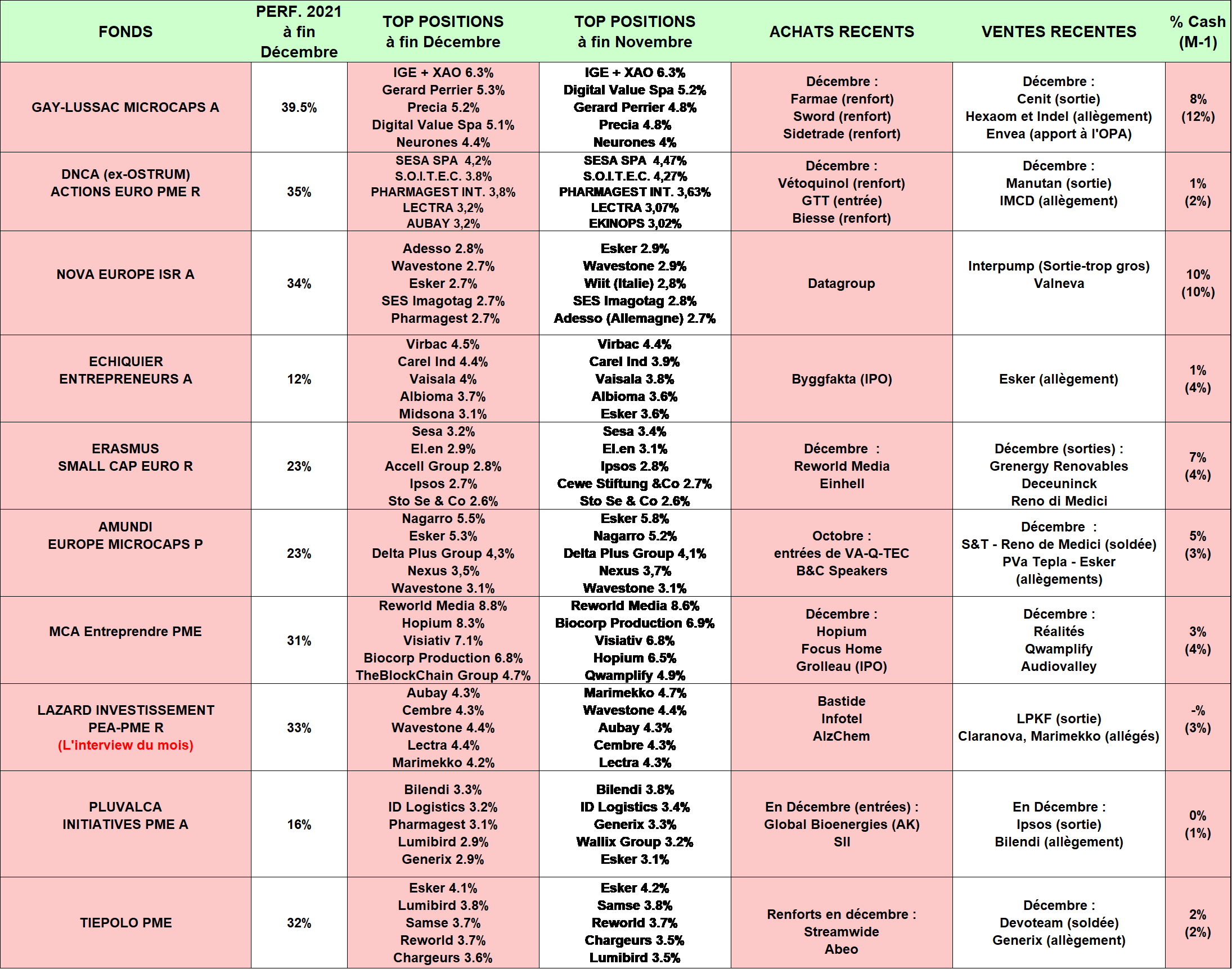

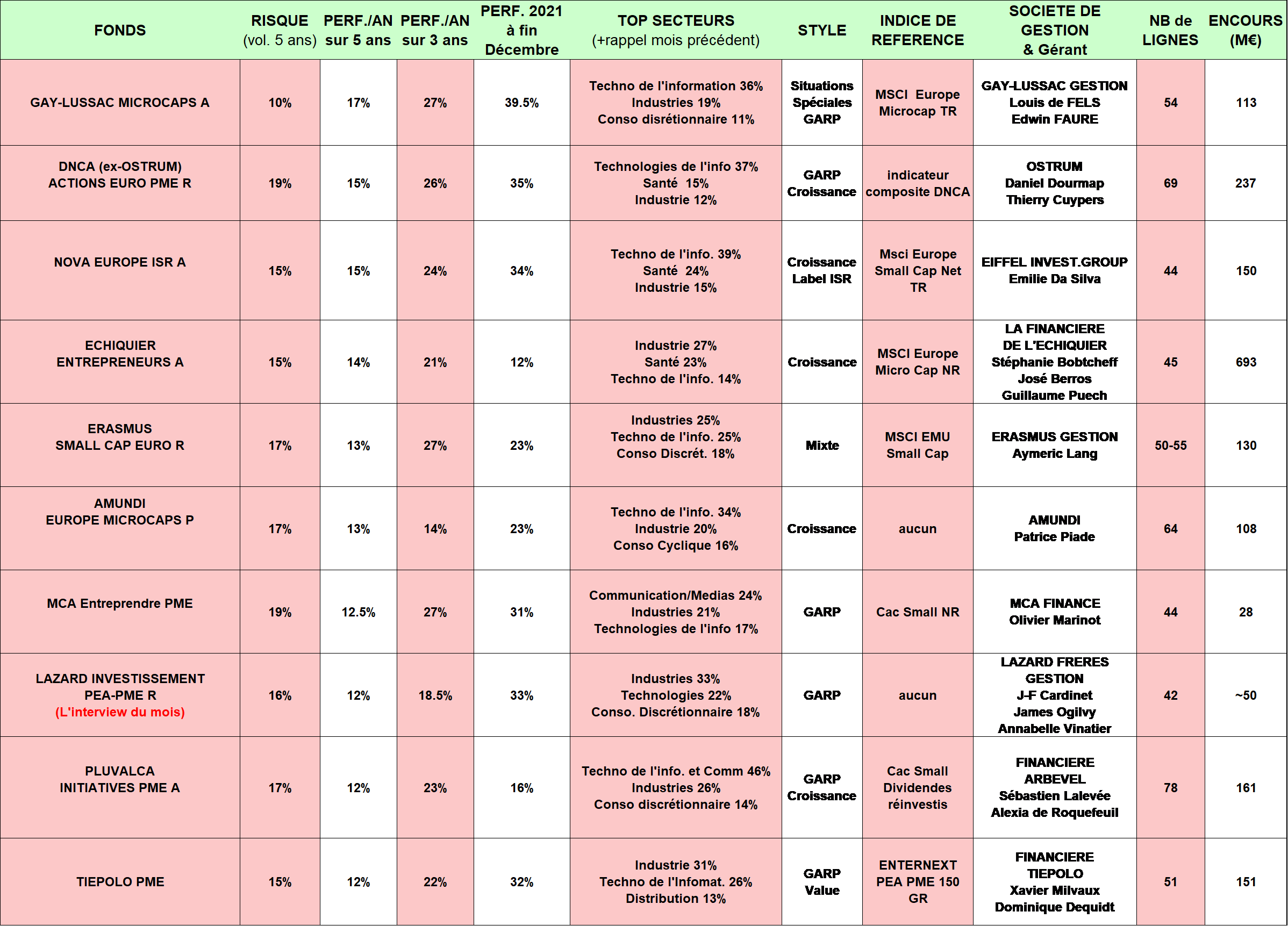

Review of the best Small Caps funds at the end of last month

(Source: Quantalys, monthly management company report)

The context being established, let’s come to the movements of our flagship funds through our summary table.

In general, we notice that:

- The average performance of the funds in the selection in 2021 (+27%) stands out above the French and European small cap indices (+23% for the CAC Small as well as for the MSCI EMU Small Cap)

- Information Technology, Industrials and Healthcare are the sectors best represented in the very best funds, which is hardly surprising given their appeal for growth stocks which largely outperform over 5 years.

- Investment rates are stable overall, as are outstandings.

More specifically, we note that:

- The bottom Gay-Lussac Microcaps is by far the best performing fund in the short, medium and long term. In 2021, it shows a 39.5% increase, despite much lower volatility than the competition. The takeover bids and takeover bids launched on a large number of securities held by the fund played on this high performance obtained despite reduced volatility. Like its sixth line, ENVEA, which benefited in December from a second takeover bid by its majority shareholder with a premium of 25%. The position will be contributed given a now acceptable valuation. Regarding the main movements, note the exit of “Cenit AG in this period of managerial transition and the resulting uncertainties on the new strategic axis to come. We are continuing our reduction on Indel in this context of pressure on 2022 margins, partly linked to the rise in copper. Same observation for Hexaom which will be under pressure on margins due to the inflation of raw materials and wages in 2022. On the reinforcement side, we continue to increase our line in Farmaè, the current price of which does not seem to us to reflect the group’s intrinsic value or its growth prospects over the next 4 years. We have also strengthened our position in Sword Group, which continues to outperform its 2024 strategic plan and which should record good growth in its operating margin in 2022. Finally, we increased our stake in Sidetrade after taking advantage of a fall in the share price following the slight slowdown in growth last quarter.”

- Pluvalca SME Initiatives saw “values linked to reopening like Lisi or Fountaine Pajot” progress. “Groupe Gorgé also outperformed following the exceptional distribution of Prodways shares to its shareholders as well as its confirmed interest in acquiring iXblue in order to strengthen its expertise in advanced autonomous, marine and photonic technologies (…) Conversely, technology stocks suffered from sector rotation like Wallix, Soitec or Generix”. Regarding entry-exit, the fund indicates: “we have sold our position in Ipsos, whose year 2022 seems more challenging from a growth and profitability point of view. In addition, we initiated a line in SII, which should continue to benefit from the dynamics of digitalization and the recovery in aeronautics, while its valuation remains consistent. The fund also participated in the capital increase of Global Bioenergies in order to help them accelerate the industrialization of their solution for waterproof cosmetics. More generally, the managers start “2022 with confidence” adding that “earnings growth expectations for 2022 seem quite cautious while the valuation of the asset class is reasonable. »

- Exchequer Entrepreneurs looks back on a year of underperformance in 2021 (+3.70% over the month and +12.13% in 2021) after years at the top of the rankings. “2021 will have been a disappointing year for Echiquier Entrepreneurs despite its absolute progress. The fund underperformed its index for the first time in a calendar year since its launch in 2013. This underperformance can, in our view, be summed up in three points:

-Underexposure to cyclical stocks or stocks exposed to the reopening of economies, which were very penalizing at the start of the year.

– Operational disappointments on certain titles, including MIDSONA, STORYTEL or NEOEN.

-Our cautious approach to the valuations of growth companies, in a year in which stocks with very high multiples performed best. However, we remain convinced that the quality of the stocks in the portfolio, their growth potential and their reasonable valuation will result in a rebound in our strategy over time. Our consistent approach has been, since the launch of the fund, the engine of the performance coupled with its low volatility.

We assume our underweighting in cyclical or very high multiple stocks, and believe that our strategy could perform well in an environment of normalization of valuation multiples. »

- The bottom Erasmus Small Cap Euro ended the year with an increase of 23.5% against 23.3% for the MSCI EMU Small Cap. “Accell Group (+25% in December) announced figures well above expectations for the first 11 months of the year, which led to nice upward revisions in the consensus. GTT (+16% in December) has multiplied the announcements of new contracts, and has a well-filled order book for 2024/2025. Conversely, Apontis Pharma (-5.5%) and Italian Wine Brands (-4%) fell for no fundamental reason. IWB announced an attractive acquisition of a US distributor on December 31. A few movements to close the year. We have finished disposing of our remainders in Grenergy Renovables and Deceuninck and we tendered our Reno de Medici shares for the takeover bid. Opposite, we initiated a position in Rothschild, which should benefit from a well-filled mergers and acquisitions pipeline for the start of the year. And we also bought Reworld Media, which could accelerate in terms of external growth in 2022, and Einhell, a quality company perfectly positioned in the DIY niche with its range of cordless tools for DIY and gardening. »

Finally, here is some additional information on the ten selected small value funds:

(Source: Quantalys, monthly management company report)

The funds were selected according to their long-term performance (we have chosen a duration of 5 years, the duration generally used for investment in equity funds) and their heavy weighting in French stocks capitalizing less than one billion euros ( minimum 20% of the fund).

We note that the “growth” or “growth” management style largely dominates the selection and that the number of securities in the portfolio varies easily from simple (40 stocks) to double (80 stocks).

Glossary: Management styles

The “Growth” or “Growth” management style favors growth stocks. These stocks are chosen for their strong development potential, putting their stock market value in the background with regard to the turnover and the results currently achieved. These companies are indeed often popular and expensive because their outlook is high and their valuation anticipates continued earnings growth. The best growth stocks will be able to grow beyond cycles and regularly take market share through organic or external growth.

Over-represented sectors: technology, health, renewable energies. Examples of growth stocks: Virbac, Voltalia, Esker, Pharmagest… Typically, their PER exceeds 20 or even 50x.

The “Value” or “Value” management style favors discounted, poorly valued and often unloved stocks. The managers then focus on the published figures, which are more reassuring than uncertain forecasts by nature, and on the value of the assets on the balance sheet.

Over-represented sectors: cyclical stocks, automotive, banking, construction. Example of value: Quadient, Hexaôm, Plastivaloire, ALD, NRJ Group… Typically, their PER is less than 10x.

The “GARP” management style or Growth At Reasonable Price or Growth at a reasonable price, seeks to find a happy medium between the two, to unearth growth stocks of course, but not at any price.

Example of value: LNA Santé, Ipsos, Beneteau… Typically, their PER is between 10x and 20x.

Let’s end with a quote from Warren Buffet: ” Better to buy an extraordinary company at an ordinary price than an ordinary company at an extraordinary price. »