L’Europe counts thes three largest western producers ofstainless steel mainly used for appliances, transport, architecture and medical services, but with operations that remain international to say the leastare : the Spanish Acerinox (ACX), Luxembourgish Aperam (APAM), separated from the largest steel producer ArcelorMittal (MT) a decade ago and Finnish Outokumpu (OUT1V).

In the field of steel, stainless steel represents only a fraction of production but sDemand is constantly on the rise with the rise in the standard of living. However, the sub-specialty does not completely escape the global trend of the steel industry: the cyclicality is strong and the capital intensity very high. This results in levels of mediocre profitability over the long cycle and long sequences of underperformance. There was a big round of sector consolidation during the previous cyclewhich did not deliver the expected results but which will have made it possible to limit the breakage.

The area (of steel in the broad sense) also remains under constant pressure from low-cost Chinese producers who practice aggressive dumping on international markets to dump unabsorbed production surpluses on the domestic market. In Europe and North America, significant surcharges are also imposed on Asian players to protect domestic producers from aggressive competition. Outside of these markets protectedChinese groups reign supreme because they remain unbeatable on cost.

So much for the overall context. If the sector is coming back to the fore, it is because of rumors of reconciliation Between Acerinox (who had been a successful investment in 2021 within the Europe PEA portfolio of Zonebourse) and Aperamwhich does not have not really surprised industry connoisseurs. Besides, it’s notas the first time such speculation has surfaced. We now know that the operation fell through, at least on the basis of the initial terms, but we were not going to throw away our summary, so we are nevertheless examining the ins and outs of the sector.

Over the last cycle, Acerinox and Aperam both delivered very similar performances: identical turnover or almost and roughly 2 billions of dollars cash profits (free cash–flow) over the period 2011-2021 in aggregate. Their current valuationaround 3.2 billion euros, is around 17 times what they have brought in in a decade, which seems high and may signal a cycle top. As such beware, it is always tricky to buy a cyclic at the top of the cyclethat is, when it delivers record resultss. Illustration with current figures: despite a profitable cycle and abnormally low interest rates, profitability remains barely equal, or even significantly lower than the coût capital. So even if they are the two best students in the class, Aperam and Acerinox have not created any value. The third thief, the Finn Outokumpuhas only delivered half of the free cash flow of its peers over the 2011-2021 cycle, despite a higher turnover. The dossier has always been uninvestable at cause of one cost structure too high.

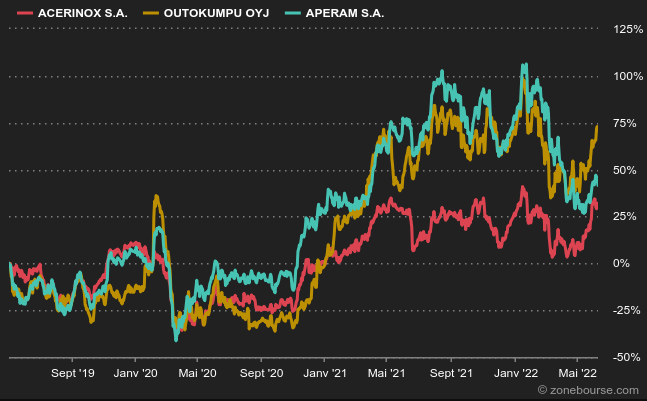

Evolution of the three players since August 2021

In short, an Aperam/Acerinox merger, which both have a reputation for being well managed, could make sense on paper. But the steel industry has a tendency to always play the same tune: consolidation will compensate for historical difficulties. By generating economies of scale, optimizing production capacities, internationalizing sales or sharing costs. Just look at the courses ofUS Steel orArcelorMittal to realize that the problem is complex. Added to this is regional protectionism, which prevents smooth international development.

If history is any guide, it is therefore prudent to cast a skeptical eye on a possible merger between Aperam and Acerinox. The question no longer seems to arise in the short term after the end of inadmissibility sent by the Spaniard to Aperam. But the above decryption will remain valid at the next opportunity.

Focus on Acerinox

Acerinox (ACX) is one of the world leaders in the production and marketing of stainless steels. The activity is essentially organized around three families of products, molten and molded steels, hot-rolled steels and cold-rolled flat steels. The Spaniard dominates the stainless steel market in the USA, with 35% market share. 50% of the group’s sales are made across the Atlantic. It is the leader in high performance alloys, with 27% market share in the EU and 12% worldwide.

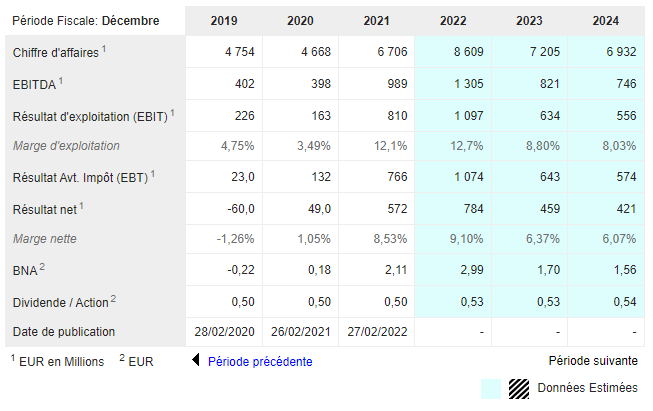

Acerinox recorded record figures in 2021. Its net profit increased 11 times to €572 million, thanks to the increase in demand which sent steel prices soaring around the world. Revenues amounted to €6.7 billion, or 44% more than for the same period of the previous year. “This is the best result in our history,” said the company at its annual meeting, allowing in particular a buyback program of 4% of the capital.

Historic results

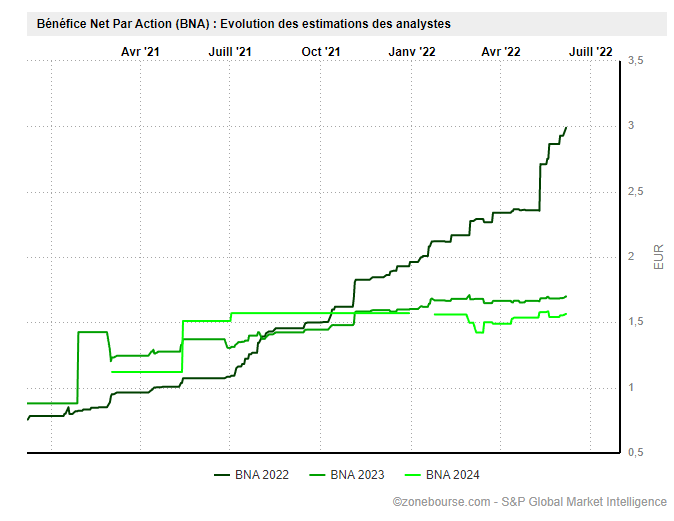

The outlook looks solid for the current year, which has earned the company a sharp upside adjustment.out of consensus. As the chart below illustrates, the projections for the next two years are much more conservative.

BPA revision of Acerinox for the year 2022

Indeed, the sector is facing galloping inflation after a decade of accommodating central bank policies. This is reflected in the sharp rise in energy pricesenergy necessary for the operation of the electric furnaces which make it possible to produce steel. Capital-intensive companies (steelmakers, cement manufacturers, etc.) initially benefit from a resurgence of inflation – as revenues are adjusted in real time, while fixed assets are carried at amortized cost – but this momentum stops as soon as new investments are made.

Soaring inflation leads to soaring capital needs, even as lenders place less value on long-term commercial contracts following a discount rate of “free cash flow” more raised – because a euro received tomorrow will be worth much less than a euro received today – and requires higher interest rates.

Conclusion :

Steelmakers recorded record profits, following a very special year in 2021. The various exogenous shocks and a V-shaped recovery of the post-covid world economy which led to price increases on steel and its derivatives benefited producers of raw materials who are favored by Zonebourse’s quantitative filters, which can reflect a cycle high for steelmakers.

It is in this context that it remains prudent to approach the securities of steelmakers on the equity side (Acerinox, Aperam, Outokumpu and ArcelorMittal) as trading instruments to play on a favorable momentum at the bottom of the cycle rather than from a heritage perspective long-term, because it is always a trap to buy a cyclical at the top of the cycle when it delivers record results…