All retail players face the same difficulties: their costs are rising due to inflation of goods, wages, logistics, operating expenses, etc. They were able to pass on part of this increase to selling prices, but these have now reached the bearable limit for customers. In this context of a combination of unfavorable factors, distributors are therefore forced to cut back on their margins.

At Target, inventories are piling up when they once rotated at a record pace of 7-8 times a year. Among the items that make up unsold items, we find a majority of “big items”, household appliances or garden furniture. The group’s turnover increases by 4% but with inflation which has returned at more than 5%, growth in real terms is actually negative. Inventories increase by 43%. The dynamic is similar at Walmart: turnover is up slightly (2%) but inventories are up 32%.

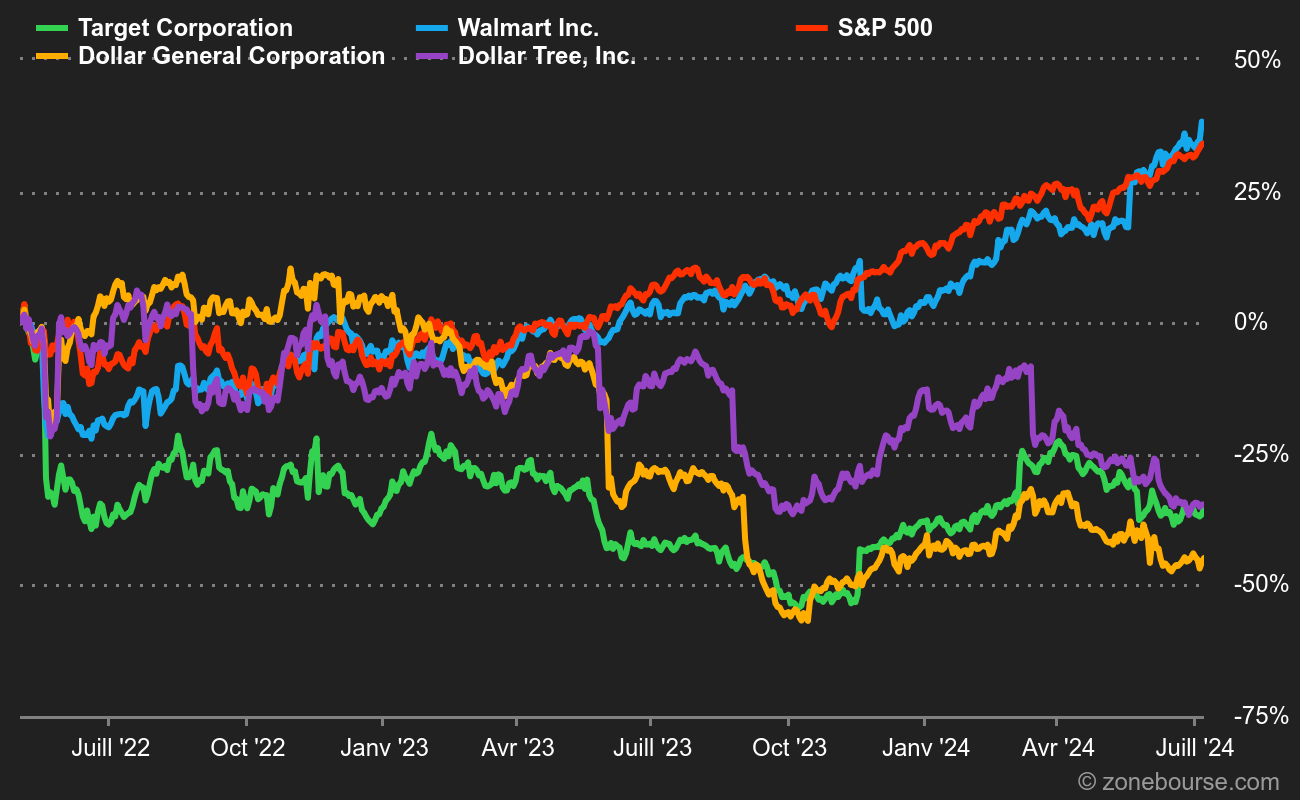

The recent stall of the two titles

Depreciations in sight

Depreciations (or “markdowns” in English) therefore seem inevitable on these stocks, because they will have to be sold to liquidate them, which should lead to billions of dollars in losses. On the other hand, this should considerably boost cash flows because working capital requirements will be lower, as in 2020. It should be remembered that distributors are still adjusting to the economic situation with a 6 to 12 month delay (they replenish their stocks when demand increases and destock when demand decreases).

The two groups pay for their overconfidence because the pandemic has only reinforced their domination of the distribution market in the United States: Target in peri-urban areas (suburbs) and Walmart in the counties at lower population density.

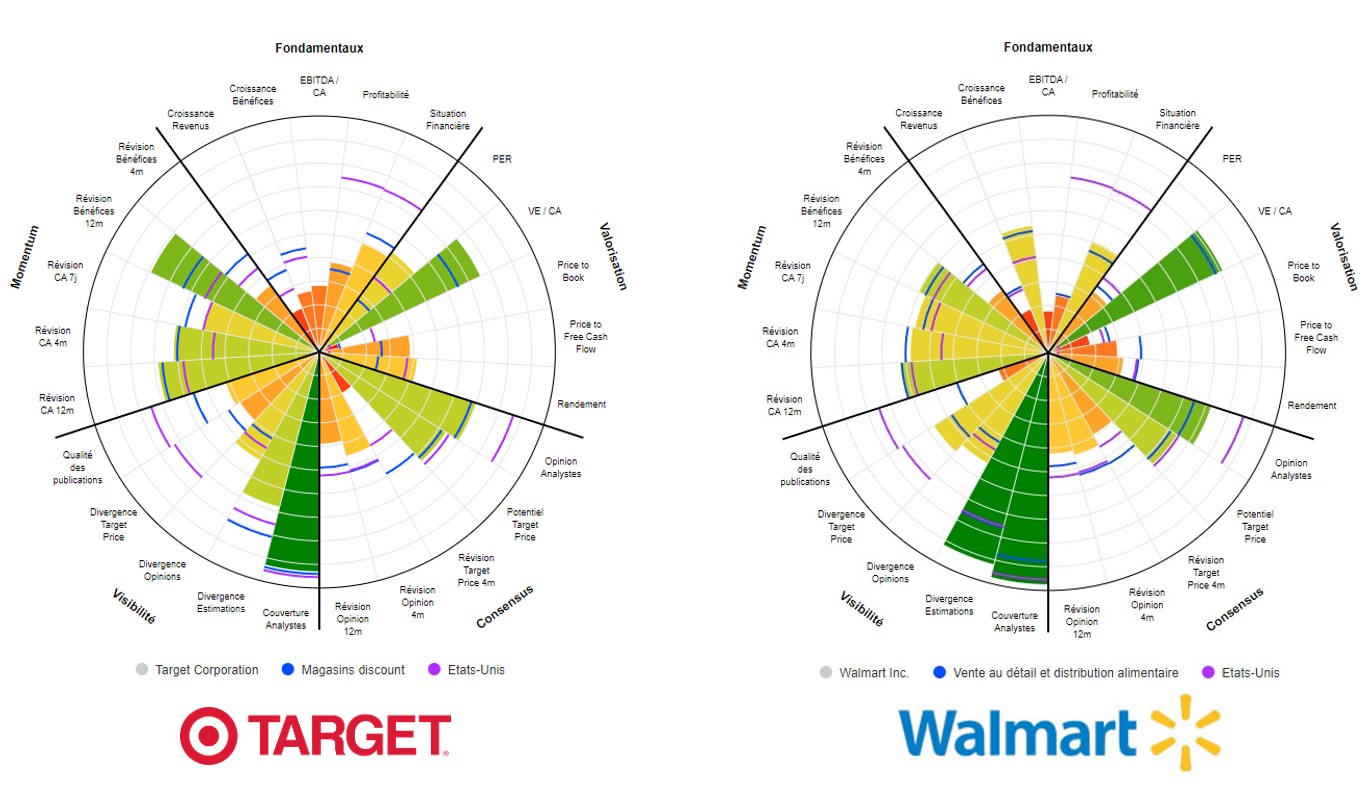

Two different profiles

Target has 2,000 stores and has a market capitalization of $71 billion. It can boast of strong growth since the pandemic thanks to a winning strategy: an “upscale” positioning. and a catalog extended to new product categories. Choices that were contested at the time but which paid off after a long cycle of stagnation. Indeed, experience proves that consumers appreciate finding everything under one roof. The group’s margin profile is excellent: the average operating margin is above 5%, with between 4 and 6 billion dollars of free cash flow per year, as well as an ROE of 25%, without the company makes excessive use of leverage.

walmart, meanwhile, has a much larger footprint with 10,500 stores and a more developed international presence. Its market capitalization, of 327 billion dollars, is much higher than that of its rival, but the group, which has always defended a low-cost positioning, displays lower margins than those of Target. Still, Walmart pays itself a lot more than Target, perhaps because the market is betting that in a recession consumers will naturally favor the low-cost alternative, and thus Walmart over rival Target.

Different profiles but common characteristics (Polar Chart Zonebourse – Click to enlarge)

It was also noted yesterday that low-cost distributors Dollar General and Dollar Tree raised their forecasts: a sign that low-income and median-income consumers are moving towards these brands as prices rise.

The same chart as the first, with reactions from Dollar Tree and Dollar General

In both cases, the groups have exceptional competitive advantages and an absolute network of the territory. Target dominates the suburban landscape populated by a more affluent clientele. Walmart has unparalleled purchasing power in global distribution, it is able to make incomparable economies of scale and thus enjoys the ability to systematically offer the best prices.