|

|

| Tops / Flops of the week |

|

Tops Pinduo-duo (+26%): The Chinese group, which sells food products online, was boosted by the publication of sharply rising profits in the second quarter. Internet sales were supported by the confinements which continue to hit different areas in China, as part of Beijing’s zero-covid policy. In addition, the group made a first foray abroad by launching its Temu platform in the United States, in the hope of competing with Amazon.

Nutanix (+22%): The Californian software publisher escaped the sectoral punishment this week thanks to the announcement of stronger than expected results. Losses were reduced despite a revenue contraction in the last quarter of the 2021/2022 financial year. The forecasts for the new vintage are a little higher than what the market expected.

InPost (+13%): The market welcomes the good half-year results of the Dutch parcel operator. JPMorgan raised its target price from 9.60 to 10.20 EUR in stride.

Cameco (+11%): Financiers looking for an opportunity in the nuclear industry, a mode of energy production that is central to the game, continue to favor the Canadian mining group specializing in uranium.

Snap (+9%): If Snapchat employees are looking gloomy, investors have appreciated the weight loss treatment proposed by management, which will part with 20% of its workforce and refocus its efforts on its core business.

unicredit (+9%): European banks are benefiting from the prospect of increased betting on the pace of ECB rate hikes. This configuration is good news in the short term for financial institutions. In the longer term, it is more debatable.

EuroAPI (+7%): The company born recently from a split with Sanofi published good results, which made people forget the difficult period around the controversy over Zantac which hit its former parent company.

Verbund (-19%): The Austrian energy company is a collateral victim of the setbacks of Wien Energie, the company to which the country’s authorities had to grant a €2 billion loan to cover its margin calls due to soaring prices of the market. There is no link with Verbund, but the context is heavy for European energy companies, caught between an exploding supply cost and consumer tariff protection measures decided by the States. BioMerieux (-15%): The half-year results were not at all convincing. This despite the slight increase in targets. Midcap Partners takes note of a publication without great surprise, but goes from buying to keeping by reducing its objective from 124 to 97 EUR, in particular because the competitive environment requires more R&D expenditure. Nvidia (-14%): The United States has asked the company to limit its exports of sophisticated chips to China. An announcement that comes as the week was already complicated for the company, which suffered heavy releases in the wake of the entire semiconductor industry, expiatory victim of the firmness of the Fed. glencore (-11%): Like the rest of the mining rating, except for uranium, as we saw above, the stock fell heavily, due to fears that weak economic momentum is weighing on demand for raw materials. |

| Raw materials |

Oil : Concerns about the dynamics of oil demand have intensified again this week as China decided to lock down one of its cities, Chengdu, which has more than 20 million inhabitants. Oil prices are therefore approaching the USD 90 line, a threshold that could push OPEC+ to tighten production to support the market. In this regard, the extended organization of oil producing countries will also meet on Monday to update its production targets. At the time of writing, Brent is trading at USD 94 and US WTI at USD 88.50. In Europe, the price of natural gas eased significantly to 209 EUR/MWh. Gazprom is likely to resume gas flows to Europe via the Nord Stream pipeline according to Bloomberg.

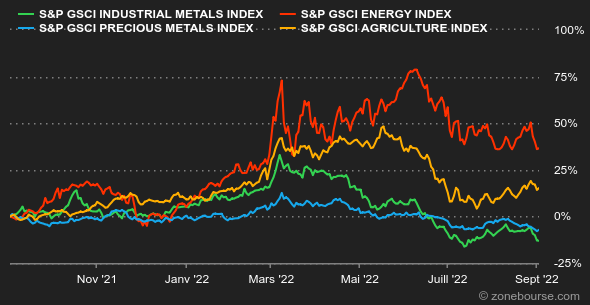

Metals : The strengthening of the dollar weighed on the compartment of industrial metals and precious metals. Copper thus fell back below the line of 8000 USD to 7600 USD per tonne. The same dynamic for the barbaric relic, which temporarily traded below the USD 1,700 per ounce mark.

Agricultural products : Grain prices have generally stabilized in Chicago, where wheat and corn are trading at 800 and 660 cents a bushel, respectively. The latest report from the United States Department of Agriculture (USDA) highlights that 54% of corn crops in the United States are considered “good to excellent”, compared to 60% last year at the same period. A drop in yields that can be attributed to the drought, which is also affecting North America. |

|

| Macroeconomics |

Vibe : Perfect Storm. The Fed banged its fist on the table last Friday to remind investors not to get too excited and that the monetary tightening cycle still has a long life ahead of it. Message received apparently. It is in Europe that the pressure has increased a notch, after the publication of inflation of 9.1% in August. The market thinks the ECB will have to raise rates by 125 points by the end of October, which implies a tightening of 50 and another 75 points to be split between the September and October meetings. The trap is closing on the old continent, between economic slowdown, rate hike and major (historical?) energy crisis.

Rate : Bond markets entered their first bear market in decades on Friday. Meaning they have lost 20% from their peaks as yields climbed. The 10-year US debt is now remunerated at 3.26% and the 2-year at 3.50%. In Europe, 10-year rates range from 1.59% in Germany for the Bund to 4.22% for Greece. France is at 2.20%, the United Kingdom at 2.91% and Italy at 3.93%. What can we conclude from this? That the major economies continue to adjust to an environment of higher policy rates.

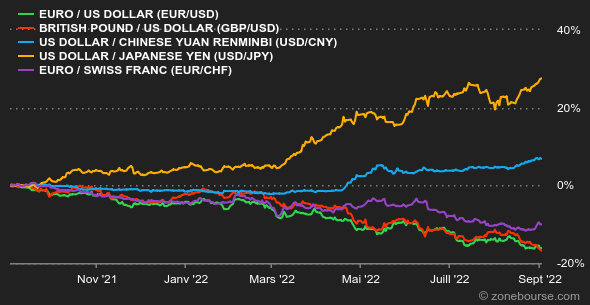

Currencies : The competition of firmness between central banks leaves the euro/dollar pair around parity. However, the single currency has gained ground against most other currencies. In particular the CHF at 0.97641 and the GBP at 0.86177. The outlook for a rate hike by the ECB, which meets next week, explains this good performance. The greenback is generally taking advantage of its safe haven status to drain purchases, which have led the Dollar Index (USD against the currencies of Europe, the United Kingdom, Canada, Sweden, Switzerland and Japan) close to 110 points, for the first time in twenty years.

Cryptocurrencies : After shedding almost 20% of its capitalization over the previous two weeks, bitcoin breathes a little bit by coming to grab more than 4% since Monday. The digital currency is thus returning to settle just above the psychological threshold of 20,000 dollars at the time of writing these lines. On the other hand, while still evolving in an anxiety-provoking macroeconomic context, the slightest technical rebound is proving to be relatively fragile and, for the moment, the positive catalysts that would herald a lasting return to the upside are rare on the asset market. digital.

Calendar : For once, it is the back-to-school meeting of the European Central Bank that will generate the most interest next week. See you on Thursday. It should be noted, however, that Fed chief Jerome Powell will also deliver a speech on Thursday afternoon, which, given the schedule, will collide a bit with Christine Lagarde’s comments after the ECB’s monetary policy decision. Finally, note that the American markets will be closed on Monday for a public holiday. |

|

|

| Items of the week | ||||||

|

| *The weekly variations of the indices and stocks displayed on the dashboard relate to the period from Monday when the respective markets open to Friday when this newsletter is sent. The weekly variations of raw materials, precious metals and currencies displayed on the dashboard relate to a period over 7 rolling days from Friday to Friday until the sending of this newsletter. These assets continue to trade on weekends. |

Zonebourse.com 2022