Mutuals or even complementary health are obliged to communicate on the estimates, their rate of redistribution, that is to say the percentage of contributions paid back to their customers. Supposed to inform the (future) client about the organization’s strategy and its pricing policy, it is too often devoid of clear explanations to bring competition into full swing. Above all, it does not replace the individual guarantees offered.

Every year, it has become a ritual, contributions to mutuals, complementary health insurance and other provident institutions increase. In 2023, the price rose by an average of 7%, according to estimates by the consumer association UFC-Que Choisir. Based on 594 contracts studied, the increase is 126 euros per year. According to the comparator Meilleurtaux Assurances, families and seniors are the most affected by high prices. The annual contribution for a family with two children had thus reached an average of 1,172 euros in 2022, up 6.55% over one year.

The fact remains that beyond the annual bill, the policyholders subscribe in particular to complementary health insurance to limit the remainder charged after a visit to the doctor or the purchase of a new pair of glasses. And the amount redistributed in 2021 is 31.6 billion euros according to Department of Research, Studies, Evaluation and Statistics (DREES). A rising total which brings us back to the level of the insured is no longer calculated in euros. We then speak of the rate of redistribution.

What is the redistribution rate?

The redistribution rate corresponds to the ratio between the amount of benefits paid and the amount of contributions collected. Clearly, and on average, the difference between what I pay and what I receive each year from my mutual. Still on average, it is 80%with differences depending on whether you are a customer of a mutual insurance company (81%), a provident institution (86%) or an insurance company (77%).

Concretely, for 100euros of contributions in 2021, provident institutions paid an average of 18 euros in optics against 13 euros for insurance companies and 11 euros for mutuals. In dentistry, they redistributed 20 euros against 15 euros for insurance and mutuals, details the DREES in its annual report.

Another distinction to be made to assess the quality of the redistribution: the individual or collective nature of the contract. Indeed, since 2016, all employers in the private sector have the obligation to provide a collective health mutual fund for their employees and to participate at least up to 50% of the price of the contributions. Individual contracts (51% of the total) are more profitable for organizations because the level of reimbursement is often there… less interesting for the insured only with a collective contract.

A very smooth redistribution rate

Since December 1, 2020, it is possible to terminate your health mutual at any time, after 1 year of commitment, without justification or costs. On this occasion, UFC-QueChoisir had denounced the opacity of the sector concerning the communication of the redistribution rate to potential insurers.

According to the association, this lack of transparency undermines free competition in the market. In 2023she always asks better information for individuals and a better understanding of the figure, explains Maria Roubtsova, economist, specialist in health studies at UFC-QueChoisir MoneyVox. This is still not the case with most organisms.

As shown in the table below produced by MoneyVox, the redistribution rate of market players is provided when a simple quote request is made. However, it remains difficult to access on the website of health organizations. Moreover, even communicated, you have to look for the information because its position is not fixed in the estimate. For one, we had to push page 49 of the information notice when others write it in a very small font.

Conversely, its drafting is mostly standardized and smooth:

The ratio between the amount of benefits paid and the amount of contributions received is XX%. The ratio between the amount of benefits paid for the reimbursement and compensation of costs caused by illness, maternity or accident and the amount of contributions or premiums related to these guarantees represents the share of contributions or premiums collected, excluding taxes, by the insurer under all the guarantees covering the reimbursement or compensation of the aforementioned costs, which is used for the payment of the benefits corresponding to these guarantees

The figure given is therefore not necessarily explicit and it is difficult to understand how 20 point cards exist between two organisms:

| Body | Redistribution rate |

|---|---|

| Mutual Harmony | 84.83% |

| ProBTP | 84.16% |

| MGEFI | 84% |

| Matmut | 81% |

| Macif | 79.4% |

| Complete | 79.1% |

| MGEN | 78.8% |

| AG2R La Mondiale | 76.86% |

| Groupama | 75.61% |

| Malakoff Humanis | 74.98% |

| FMG | 64.4% |

Redistribution rate: ratio between the amount of benefits paid and the amount of contributions collected, excluding taxes, by the insurer.

Source: quotes requested by MoneyVox since March 1, 2023

Redistribution rates for health supplements vary from one organization to another according to various criteria (collective or individual contracts, distribution costs, miscellaneous costs, etc.). Each insurer is free to apply its own terms and conditions, replies France Assureurs MoneyVox.

save up to 70% on your borrower insurance

Fuzzy management fees

In the bullseye, everyone does what they want, without justifying it to the insured. Despite an average weight of 20% of the total contributions received according to the DREES (22% among mutuals, 14% among provident organisations), management fees are not better detailed than redistribution.

Management costs include the costs incurred for the design and marketing of offers, for the management of contracts (collection of contributions, management of the life of the contract, terminations, etc.) and services with the reimbursement of health costs, assistance, but also make it possible to finance prevention actions, explains Samuel Bansard, the president of Meilleurtaux assurance. They may be considered high by some, but this also results in the quality of the service provided to policyholders.

Harmonie Mutuelle has for its part taken an 80/20 commitment with its customers. The 20% not paid to reimburse benefits are also used develop teleconsultation, finance preventive actions or provide social support for people in difficulty.

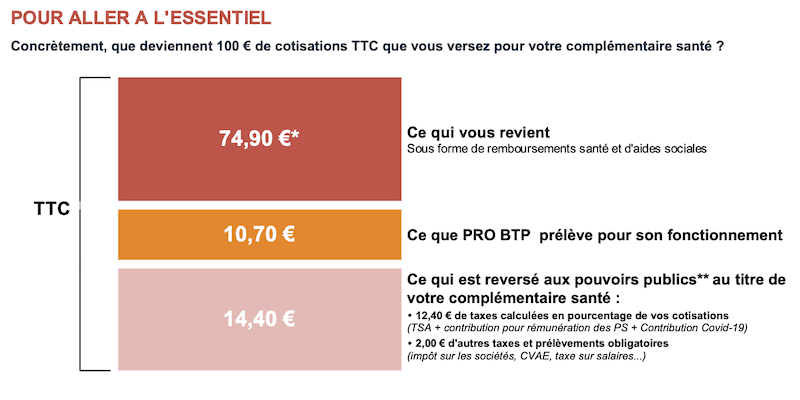

There remains one last pick the good information of (future) customers. The redistribution rate is exclusive of tax. Fortunately, ProBTP, which displays a high level of redistribution, also offers an informative infographic, in addition to entering the details of its management fees:

Out of 100 euros, only a little more than 74 are paid to policyholders despite a posted rate of more than 84%. The difference is mainly explained by the additional solidarity tax (TSA) and the exceptional COVID-19 contribution which are returned to the State. In addition, since 2021, organizations have denounced the 100% health reform as weighing heavily on their costs.

Is the redistribution rate useful to the insured?

The redistribution rate is indicative, but does not necessarily predict the commercial offer that may be made to the insured. The rate can be low and the level of individual reimbursement high, agrees Maria Rubtsova. Nevertheless, the evolution of management fees over time can give an idea of the evolution of the level of contributions.

If the costs of acquiring new customers are high, it can be deduced that very attractive prices are offered to newcomers and that contributions jump over time. As with damage insurance (auto, home), it is advisable to review your individual contract at least every two years.

The payout rate is not the main factor in choosing your complementary health contract. Rather, it is appropriate to look at the amount of the contribution and the level of coverage for each item, insists Samuel Bansard. Indeed, it is your individual needs that will affect the relevance of this or that contract: optical, dental, alternative medicine or hospitalization conditions in particular. Criteria that change over time and age.