|

|

| Tops / Flops of the week |

Essity (+15%): the quarterly results of the owner of toilet paper Lotus are higher than expected. The price effect made it possible to offset the increase in costs in an unexpected proportion.

Avis Budget (+12.50%): stocks linked to the tourism sector woke up this week. The US vehicle rental company also benefited from Barclays’ recommendation to be underweight to neutral, although the analyst maintains a valuation below current levels.

Rexel (+10%): the French distributor of electrical equipment had a thunderous start to the year, which prompted analysts to revise their expectations upwards.

International Business Machines (+10%): the group’s quarterly results have won over investors. In particular because they were powered by the group’s cloud offer, which until then had been perceived as being a step behind its rivals in this field.

Holcim (+8%): nice surprise for the cement manufacturer, which is emerging from a somewhat negative spiral by publishing results that are significantly higher than expected in the 1st quarter. The figures validate an unexpected “pricing power”.

Renault (+4.40%): the results for the 1st quarter are less degraded than expected. The manufacturer has confirmed that it is considering an IPO of its electric vehicle division next year, an announcement appreciated by the market.

Antofagasta (-11%): Quarterly performance was poor, more than expected, as the Los Pelambres copper mine continues to be affected by drought in Chile.

Shopify (-20%): difficult week for the Canadian star, tormented with the technology sector and the announcement of discussions for the takeover of the technology startup Deliverr.

Didi Global (-30%): the decision to leave the US listing continues to weigh on prices. Shareholders have yet to vote on the project.

Netflix (-38%): the group lost subscribers at the start of the year and the market lost faith in the model. Even Bill Ackman, returned in January in the capital, sold everything. The growth crisis of streaming coincides with questions about the economic model, in particular the absence of advertising and the ease with which customers exchange access. |

| Raw materials |

Bearish weekly sequence for the oil markets, which continue to evolve according to developments in Ukraine. It is more precisely the development of Russian production that is closely monitored, in a context where supply is struggling to meet demand. In this regard, the lowering of global growth by the IMF raises fears of a tightening of demand for oil, which explains the easing of prices this week. Brent thus trades around 106 USD per barrel against 102 USD for American oil, the WTI.

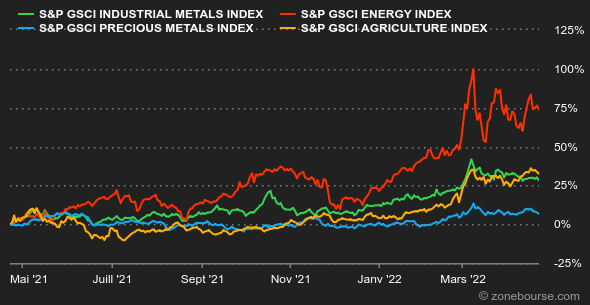

Precious metals took a beating this week, hurt by the Fed’s change of tone, which bolstered the greenback and bond yields, much to the dismay of the barbaric relic. As a sign of capitulation, gold is gradually moving away from the 2000 USD mark. This marked decline also affects silver (which is trading at 24.3 USD) as well as platinum (930 USD). It should be noted that palladium has stalled this week, an outperformance which is linked to the significant weight of Russia in the production of this metal, which accounts for almost a third of the world supply. On the side of industrial metals, the hour is generally breathing room due to the rise of the greenback. Only nickel prices ($33,775) remained relatively firm. Copper has seen an ups and downs and is trading around USD 10,300 on the LME.

A word on agricultural raw materials with structural timber, the price of which rose above 1000 USD, an increase of 15% in five days. Lumber prices had fallen sharply on rising inventories and easing supply chain disruptions. In Chicago, wheat and corn have lost ground and are buying respectively at 1070 and 780 cents a bushel. |

|

| Macroeconomics |

The week was not particularly prolific in terms of macroeconomic indicators, or rather these did not provide much information. Members of the US central bank, for their part, continued their work of preparing investors for a higher rate environment. By reinforcing the message about the speed of the movement, which seems to have gone from allegro to presto. Fed Chairman Jerome Powell himself swept away the last hopes of monetary tightening in small steps on Thursday: his statements raised the probability of a half-point rate hike on May 4 to 100 % or almost.

The Fed’s determination to raise rates quickly drove the yield on US debt higher, with the 10-year maturity at 3.95% at the end of the week, accompanied by a further inversion of the yield curve and then the 5 years was remunerated at the same time just above 3%. In Europe, the German Bund reached 0.94% and the French OAT 1.39%. It is the Swiss debt which brings up the rear at 0.84%.

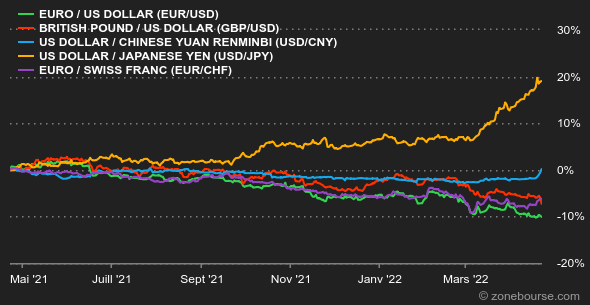

On the foreign exchange market, the dollar continued to rise against Asian currencies, against the yen at 128.398 JPY and against the yuan at 6.4927 CNY. The euro/dollar pair has seen some upheavals, but the greenback is holding its own at 1.0820 USD.

For its part, bitcoin still cannot extricate itself from this zone of 40,000 dollars in which it has been gravitating for more than 10 days now. A lateralization of the course of the digital currency which is enough to put, and a little more, the nerves of crypto-investors to the test. Players in the cryptosphere are letting themselves be carried away by the gloomy macroeconomic situation which inherently has little or no bullish catalyst to revive the crypto-asset market.

Next week, three major events are in sight in the United States: March durable goods orders (Tuesday), the first estimate of Q1 GDP (Thursday) and March PCE inflation (Friday). Also to follow, the German Ifo activity index for April (Monday) and the estimate of inflation in the euro zone in April (Friday). |

|

|

| Items of the week | ||||||

|

| *The weekly variations of the indices and stocks displayed on the dashboard relate to the period from Monday when the respective markets open to Friday when this newsletter is sent. The weekly variations of raw materials, precious metals and currencies displayed on the dashboard relate to a period over 7 rolling days from Friday to Friday until the sending of this newsletter. These assets continue to trade on weekends. |

Zonebourse.com 2022