The August 1 deadline, the date of the next revision of the Livret A, LDDS and LEP rates, is eagerly awaited by savers, who are hoping for a further rise against a backdrop of high inflation. However, they risk being disappointed. Explanations.

In a little over two months, we will have the answer: will the rates of regulated savings accounts (Livret A, LDDS, LEP, CEL) make a new leap on August 1, one of the two annual revision deadlines?

It is in mid-July, in fact, that the governor of the Banque de France, François Villeroy de Galhau, will decide, as the rule requires. Two scenarios are open to him. Either he leaves rates update automatically, depending on the evolution of inflation and short interbank rates, as required by the rule; either he decides to invoke “exceptional circumstances” to deviate from this rule.

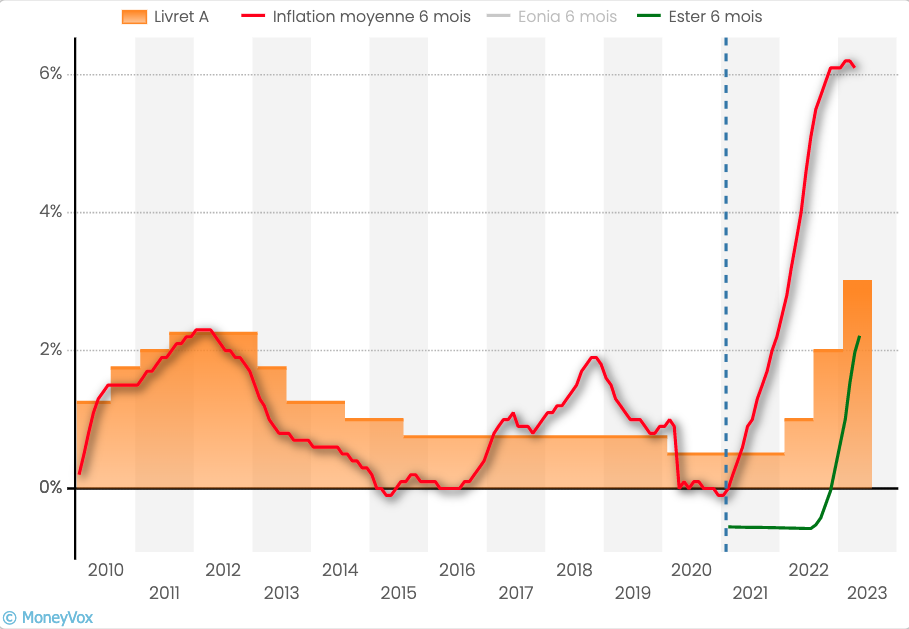

Depending on his choice, the result will be very different for savers. In the first case, the Livret A rate, currently set at 3%, will make a spectacular leap to well over 4%. 4.30%, announces Eric Dor, director of economic studies at the IESEG School of Management, in a recent note: “Inflation excluding tobacco was 6.11% in January, 6.39% in February, 5 .67% in March, and 5.83% in April. A plausible projection would be to estimate it at 5.8% in May and 5.5% in June. The six-month average of inflation excluding tobacco would thus be 5.88%,” explains the economist. “(…) The half-yearly average of the €STR rate from January to June would stand at 2.66%. With these projections for the half-yearly averages of the €STR rate and inflation excluding tobacco, strict application of the formula would imply a Livret A rate of 4.3%. »

A little boost for the Livret A and the LDDS

Bad news: this scenario, very favorable to savers, is unfortunately unlikely. From all sides, voices are raised to call for maintenance of the Livret A rate at 3%. It is the will, expressed publicly, of the banking sector, which distributes regulated savings products and partially bears the remuneration; Caisse des Dépôts, which uses this resource, in particular, to finance HLM organisations; and even, at the top of the State, Olivier Klein, the delegate minister in charge of the city and Housing.

Booklet A: “Why is it not possible to increase the rate on August 1? »

These calls have every chance of being heard. It is therefore the second scenario, that of derogation, which should occur. “It is very likely that the governor opens this possibility”, confirms Philippe Crevel, director of the Cercle de l’Epargne and an excellent expert on the subject. “So there shouldn’t be a strict application of the formula.”

This does not mean that the Livret A rate and, with it, those of the LDDS and the CEL, will not increase. At the beginning of May, the Minister of the Economy, Bruno Le Maire, opened the door to a helping hand. “My first responsibility is to protect the savings of the French, especially in this period of crisis, it is extremely important,” he said. “If ever the conclusion of the formula and the Governor of the Banque de France is that as inflation is very high, we must continue to increase the remuneration of the Livret A, [alors] I will follow the recommendation of the governor “.

“The rate will go up, it would be difficult not to do so”, estimates Cyril Blesson, economist and partner of Pair Conseil, which publishes the Savings Notebooks. “But it will be in smaller proportions, perhaps at 3.75%, the idea being not to create too large a gap with the 3-month monetary rates. » A way of cut the pear in halfbetween the current 3% and the 4.3% promised by the calculation formula.

This scenario wouldslightly improve the actual yield of the Livret A, adjusted for inflation, which is now largely negative. It’s not new. This has even been the case, without interruption, since May 2021. But the gap is widening. It’s been a long time since the differential between the Livret A rate and inflation hasn’t been so high: currently more than 3 points.

LEP rate expected to drop

Second bad news. Another regulated booklet should see its rate drop: the People’s Savings Booklet (LEP). The product reserved for the most modest households is, in fact, designed to align with the average inflation of the previous semester. This is what happened, in particular, on February 1, when its rate rose from 4.60% to 6.10% to align with inflation in the second half of 2022. However, the rise in prices , still very strong, should be a little less so in the first half of 2023: around 5.90%. The LEP rate should align with this mark and suffer a small drop of 20 basis points.