Never has there been so much money deposited in Livret A, LDDS and LEPs. But what is it for? Who holds it? Is it useful? Here are the answers to your questions.

Do you know the Savings Fund? If you are equipped with a Livret A, like 8 out of 10 French people, he, in any case, knows you. It is, in fact, in this common pot, managed by the Caisse des Dépôts et Consignations (CDC), the financial arm of the State, that the majority of the money that you deposit in your Livret A accounts is centralized, LDDS and LEP. Its mission is then to transform these funds into very long-term loansintended to finance areas designated as of general interest.

You probably know at least one: the social housing. Since 1894, money from Livret A has been used to finance the construction of new low-rent housing, allocated on social criteria. A sign of solidarity which allows us to understand, in part, a certain attachment to this unparalleled savings product.

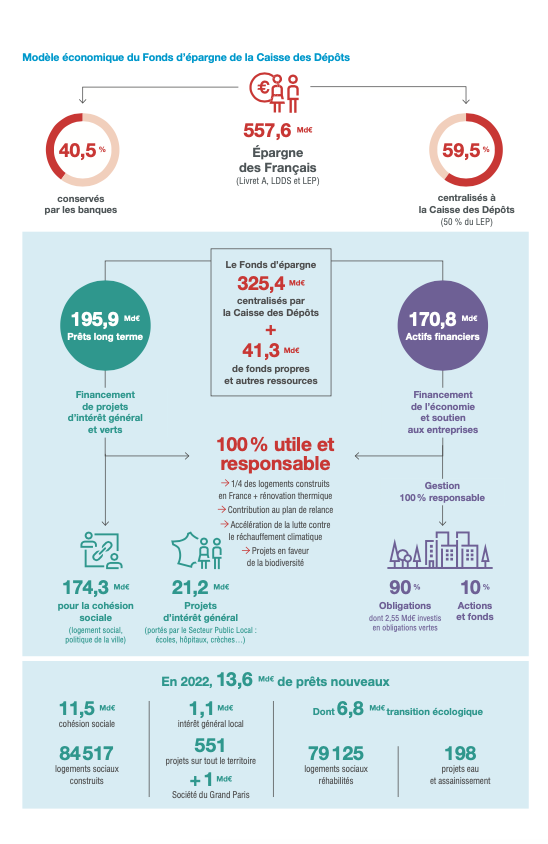

Financing social housing, however, is far from being the only use made of money from settlement books. The recent report from the Savings Fund, for the year 2022, is there to remind us: out of 100 euros invested, only 31 euros (31.25% precisely) are loaned to social landlords. Or 174.3 billion euros, out of the nearly 558 billion deposited, at the end of 2022.

What is the rest of the money used for? Recently, the government considered directing part of it towards Defense SMEs. A perspective that doesn’t enchant you: our exclusive survey (1), produced by YouGov France indicates that only 29% of you are convinced by the idea. To choose, you would prefer that this windfall benefits the public hospital (61% approval), the school (43%) or the police (21%).

225 billion euros for banks

Part of the windfall from regulated savings remains in the banks which distribute and keep the accounts: 40.5% of deposits for the Livret A and the LDDS, 50% for the LEP. At the end of 2022, this represented around 225 billion euros.

Be careful, however: banks can’t do what they want with this money. The State requires them, in fact, to direct it towards the financing of small and medium-sized businesses (80% of outstandings), as well as towards ecological projects (10%) or actors of the social and solidarity economy (5 %). Finally, they can only use 5% of the deposits as they wish. Which represents, all the same, 11 billion euros.

Livret A: what does the bank do with my money?

4.6 billion euros in interest paid to savers, more than a billion to banks

The Savings Fund pays savers the interest on the deposits it centralizes. In 2022, this represented 4.6 billion euros. Much more, therefore, than in 2021 (1.5 billion), but less than the upcoming figure for 2023. Logical, since the rates have increased significantly, and so has collection.

The Savings Fund also pays the banks which collect the money and keep the accounts, amounting to 0.30% of the centralized amounts for the Livret A and the LDDS, and 0.40% for the LEP. This additional interest reached 1.278 billion euros in 2022, an increase of 28 million euros.

Livret A: how much do banks earn from your deposits?

325 billion euros for the Savings Fund

The rest of the money from Livrets A, LDDS and LEP is therefore centralized in the Savings Fund. This war treasure exceeded 325 billion euros at the end of 2022. A figure up more than 9% over one year and which will further increase significantly in 2023.

This is the logical consequence of the excellent years 2022 and 2023 for regulated savings accounts, which have become very attractive again thanks to rates multiplied by 6 (from 0.5% to 3% for Livret A and LDDS, from 1% to 6% for LEP) . The contribution of the Livret A and the LDDS, for the year 2022 alone, reaches 23.2 billion euros, more than double that of 2021 and almost as much as in 2020, the year of confinements and forced savings; that of LEP, back in Greece, reached 4.7 billion, while it was still negative in 2021.

Centralized savings are, moreover, not the only resource of the Savings Fund, which also had 41.3 billion euros in equity at the end of 2022.

11.6 billion euros for new loans

What did the Savings Fund do with this influx of new money? In line with its central mission, 11.6 billion euros were dedicated to financing new loans for the social housing sector, which enabled the construction of more than 84,000 new homes.

1.1 billion was also loaned from local authorities. Because the money from Livret A is also used finance local projects of general interest: energy renovation of schools, nurseries or hospitals, implementation of new environmentally friendly modes of transport, drinking water projects, etc.

In 2022, the Savings Fund enriched its offer with, in particular, a Green Recovery Loan, intended for projects linked to renewable energies, the recovery of waste, biodiversity or the construction of passive or positive energy buildings, or a Recovery Loan tourism, dedicated to financing tourism infrastructure and supporting players in the sector.

Livret A: these amazing new uses of your money

27.6 billion euros for financial assets

The strong growth in centralized assets mainly fueled financial assets of the Savings Fund. To ensure the stability of its economic model, and in particular its liquidity, that is to say its ability to return the money of savers who wish to make withdrawals at any time, the Savings Fund invests part of the money from the Livret A in financial assets: shares, bonds, unlisted funds… At the end of 2022, the Savings Fund held, for example, almost 3% of French debtthe equivalent of more than 61 billion euros.

In 2022, a year of strong inflows, the amounts placed in financial assets increased proportionately: +27.6 billion euros. The total portfolio of the Savings Fund increased from 120 to 170 billion euros, an increase of 50%.

(1) The survey was carried out on 1055 people representative of the French national population aged 18 and over. The survey was carried out online, on the YouGov France proprietary panel from November 28 to 29, 2023.