We have extracted the 20 European stocks that best match these criteria. Their PERs range from 5.9 to 12 times the results expected in 2023, based on stock market prices on April 20, 2022. We have extracted three files whose presence may seem incongruous. The complete list is available at the end of the article.

The Low PER Screener, excluding the least valued sectors

- HeidelbergCement: leaves concrete

The smallest PER of our selection (6.3 times 2022 and 5.8 times 2023). The group based, of course, in Heidelberg is the world number two in cement and aggregates, behind Holcim (some Chinese players are bigger, but their international presence is weak). Cement manufacturers, unlike other producers of building materials such as Saint-Gobain or CRH (which are also part of our selection of small PERs), have mostly experienced the bottom of the wave lately, because of fears about their environmental footprint. The conflict in Ukraine, which has sent energy costs skyrocketing and heightened recession fears, has led to a new wave of caution about them. As one analyst points out, the situation in the sector is paradoxical: demand is strong and there is no substitute material, but investors do not want it. HeidelbergCement shareholders are chomping at the bit by benefiting from a 5% coupon and share buybacks in the company.

- Fresenius SE: (big) holding discount

There are health values without aristocratic PER… that of Fresenius SE is 8.9. The German is the holding company for several activities, in particular Fresenius Medical Care, which it controls through a foundation structure, while it only owns 32%. The umbrella company thus operates in dialysis via Fresenius Medical Care, in hospital management with Vamed and Helios and in clinical nutrition with Kabi. Its two largest markets are Europe (45%) and the United States (38%). The structure of Fresenius is well diversified, but its activities offer relatively few synergies between them, which explains the discount from which the company suffers. Its stock market performance has been marred lately by the absence of any major announcement in the context of the group’s strategic review, while the market was hoping for a little glitter, such as the announcement of the listing of certain branches or the sale of the balance of Fresenius Medical Care.

- STMicroelectronics: bottom of cycle

The presence of the Franco-Italian technology group in this top 20 is surprising to say the least. But the file is only paid for 12 times the results expected in 2023. Of the 16 largest Western listed groups, only the American Micron is less well valued in the sector. It’s all the more surprising that ST has made huge progress in recent years to reach the best industry standards and has become a popular supplier to Apple or Tesla. Its 11-year PER average is 28.7 times, according to S&P Capital IQ data. Despite improved results and higher targets, the market has reintegrated a dose of cyclicality into its expectations, since despite shortages, semiconductors remain a sector correlated to economic curves. He thinks that the context will be less favorable from 2023, with a risk of a downward revision of expectations. This configuration explains the caution from which the sector currently suffers, but less why ST is so poorly valued in its sector.

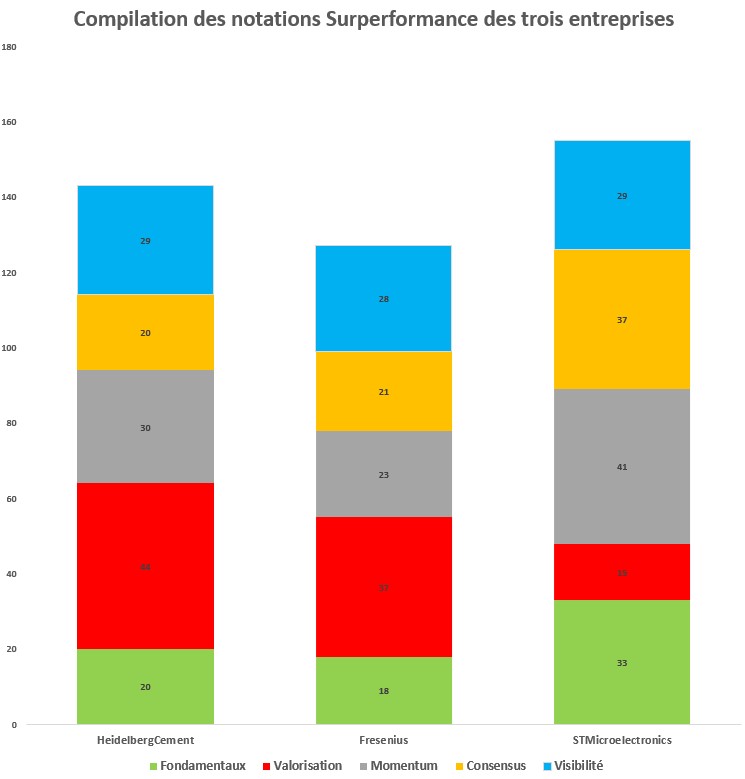

You will find below the compilation of the ratings from the Screeners Zonebourse for the three files.