Nearly four years after its release in France, the Google Pay payment platform, transformed into Google Wallet today, is still far from being unanimous with traditional banks who prefer Apple Pay and other other solutions. . But what is the problem?

It is now almost 4 years since Google set up its mobile payment system in France and despite some geographical disparities in the world, we cannot say that it has been successful. This finding stems from various factors, but above all linked to the fact that traditional banks are literally shying away from service in favor of solutions that are better anchored in the landscape, such as the inevitable Apple Pay.

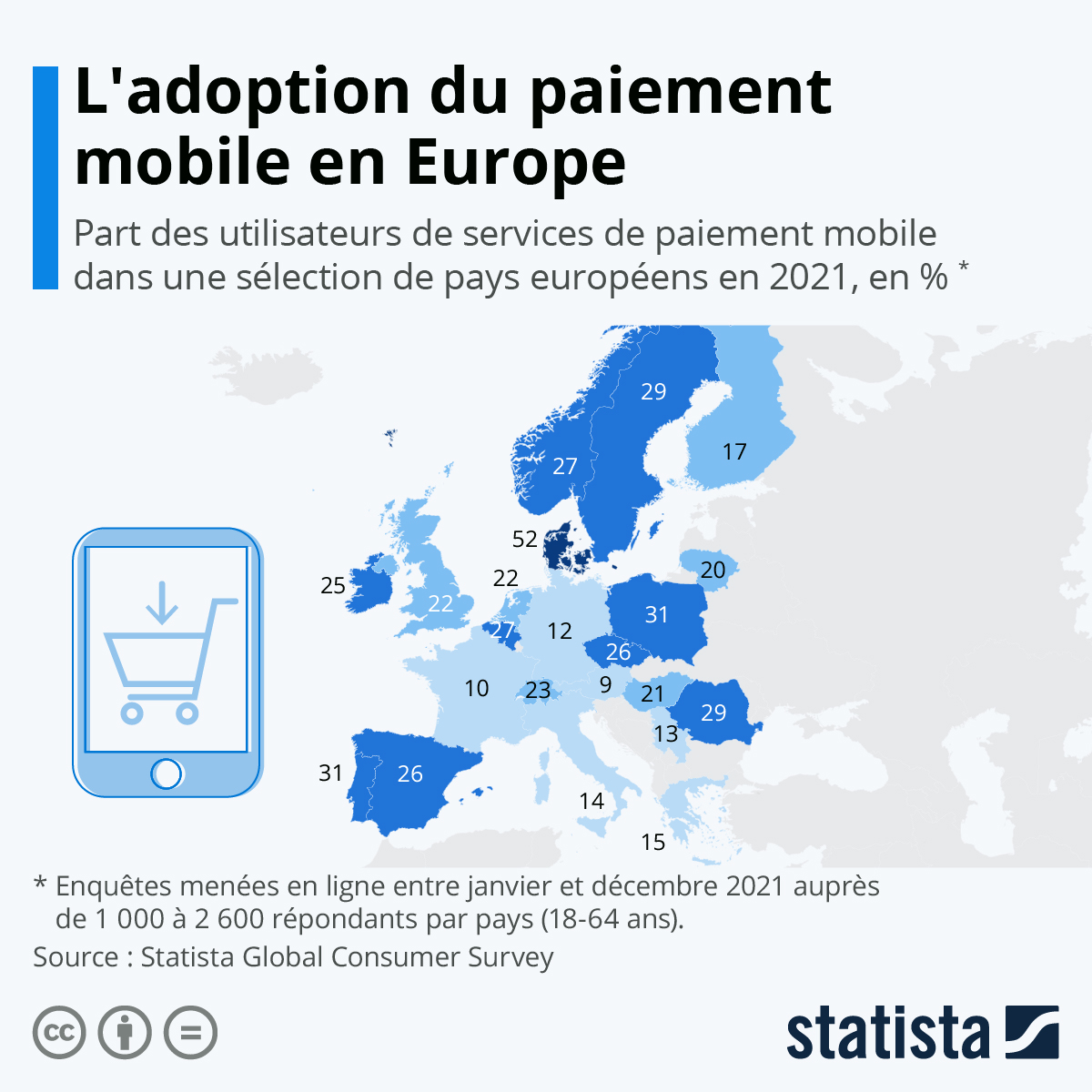

It must be said that with its various redesigns and its vague positioning in the face of competition, the American giant still has a long way to go to establish itself in its sector. In 2022 in France, payments via mobile solutions now represent nearly 3% of in-store transactions. It may not seem like much, but it’s a 177% increase over the previous year and the number continues to climb.

In 2022, only 13 online banks and neobanks are compatible with Google Wallet, such as Boursorama Banque, N26, Hello Bank! or Revolution. No traditional bank has yet taken the plunge. Let’s detail the reasons why Google Wallet is still absent from traditional banks in France.

A platform that changes all the time

First arriving in the United States in 2011 as… Google Wallet, the platform ultimately had the same ambitions as today, with one exception. The principle being to be able to store debit, credit, loyalty cards and even gift cards in your smartphone by using the NFC chips of your smartphones to validate them via a compatible terminal. An application which, however, did not yet act as a means of dematerialized payment until the arrival ofAndroid Pay in 2015 with which it merged to be renamed in Google Pay in 2018, removing the digital wallet functions in the process. Everything has been recently rebranded as Google Wallet and unified in a single platform. You follow ?

In any case, traditional banks have preferred the simpler approach of an Apple Pay despite the fact that Google does not collect any commission on transactions carried out through its platform.

Google’s will

Google does not communicate on the number of transactions that go through its wallet, just like Apple. It is therefore impossible to get an idea of the level of adoption and banks must rely on estimates and their own data. We can decently deduce that if the major French banks have not invested heavily in Google’s solution, it means that we are far from the expected figures. Especially since they are the ones that bring together the vast majority of bankable customers.

For Google Wallet, it is also a strategic desire on the part of the Mountain View firm, which has preferred since its integration in France to bet on online banks and neobanks, leaving the field open to Apple with regard to banks. traditional. A strategy that could have paid off if the release timing had been the right one, as competing services are already well established in this market as well.

Timing, another element to be borne by Google on a strictly hardware level. E-wallets are widely promoted on connected devices and watches whose use lends itself perfectly. But it is unfortunately not with a disappointing Pixel Watch that arrived much too late to impose itself against the Apple Watch and other Galaxy Watches at Samsung that Google will grab market share to impose its ecosystem. And even if the models of watches running on Wear OS are compatible with Google Wallet, the use is still too rare to be really significant.

The Oppo Watch acts as a means of payment with Google Wallet // Source: Maxime Grosjean for Frandroid

The Oppo Watch acts as a means of payment with Google Wallet // Source: Maxime Grosjean for Frandroid

Too little use of e-wallets in France

And if France was not simply too attached to the sacrosanct bank card? In any case, it is a constant that plays in the minds of many banking players in France and the COVID-19 pandemic has changed this habit very little. In addition, contactless payment by card is now much more entrenched in habits. According to the CB observatory, these represent 59% of in-store card payments with 72% of the average basket between 0 and 50 euros. A considerable argument for traditional banking establishments which still see little interest in integrating Google’s solution into their offers.

On the Internet, the observation is substantially similar, but we notice slightly different habits with Paypal, which has largely taken the tangent on the majority of merchant sites. In addition, with new measures taken by banks to combat online purchase fraud (2FA, instant transfer, etc.), payment by card is still widespread and Google’s solutions are struggling to convince e-merchants despite easy API integration.

The competition is already above

If Google was ultimately a forerunner by launching Google Wallet in 2011, it was largely outpaced by a certain Apple Pay in a field that it had not yet conquered despite its potential. Since 2014, Apple’s payment platform has enjoyed success and a conversion rate that is unmatched by that of Google. Appel Pay is much more implemented in traditional banks and is present in a majority of banking establishments, whether they are dematerialized or not.

Worse still, Google is being overtaken and even overtaken by other players like Samsung Wallet (formerly Samsung Pay). It enjoys a higher adoption rate on smartphones from the South Korean brand than that of Google itself.

What future for Google Wallet?

By changing the name and positioning of its platform, Google has understood that it needed to give an identity beyond a simple means of contactless payment. By returning to its initial concept while integrating the technical advances acquired over the years and combined with the maturity of its Pixel hardware ecosystem, Google Wallet still has a chance to impose itself in the coming years on a market that is only asking for to finally explode in France.

However, he will have to do his utmost to convince the banks to finally adopt the platform to reach the most potential customers, otherwise he will be satisfied with a limited audience and confidential success.

To follow us, we invite you to download our Android and iOS application. You can read our articles, files, and watch our latest YouTube videos.