No one knows what will happen to the pension reform project. But in any case, your quarters and years of contribution will be used to calculate your future pension. This is why it is in your best interest to dive into your career statement without delay.

Quarters, full rate, legal age, contribution period, etc. Never has the retirement glossary fascinated so many people! At the end of January, on the most famous of search engines, the word quarters was 5 times more typed than at any time of the past year. Above all, judging by Google statistics, this sudden interest in retirement jargon is unprecedented, in 2023, compared to Macron’s previous reform attempt, in 2019.

Beyond the parliamentary debates and the outcome of the social protest, take advantage of this new curiosity for pension plans to look into your career… in order to unearth errors or omissions now, or simply to better understand the impact of the future reform.

How to find your career statement?

First reflex, simple and basic: connect to your Info-retraite.fr account. You do not have any? All you have to do is use your Impots.gouv, Ameli or your La Poste digital identity to connect via FranceConnect. Then click on My career, see my career and finally Access my career. l, you can download my statement at the bottom of the page, which gives you access to a document equivalent to the one sent to you automatically your 35, 40, 45 and 50 years old.

Supplementary retirement: why you should scrupulously check your career statement

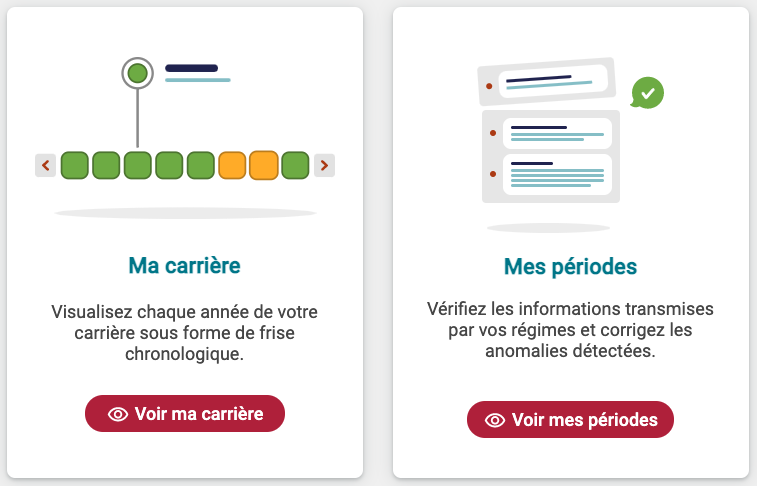

You can also consult on this same page my careermy periods or my rights, information that you will find in your career statement (RIS, individual statement of situation) but presented here in a more interactive and educational way.

For a quick glance, the tab My career allows you to quickly view your periods of employment, unemployment, or even those without information.

tab My rights offers you more details: by scrolling My rights per year, you view the number of valid quarters (or not, for lack of sufficient salary) for each of the years. There, in the right column, you will find the points per scheme, and therefore most often your Agirc-Arrco points.

How to understand your Agirc-Arrco points?

On the tab My rights Info-Retraite.fr or on your career statement, you discover the total Agirc-Arrco points, and the value of the point, of 1.3498 euro on November 1st. Basically, if you have 1000 points, this means that you are entitled to a pension of 1349.8 euros per year, gross, before taxes (so almost 113 euros per month in this example). Warning: you will accumulate other points… and the value of the point can vary, the increase or (unlikely but potentially possible) the fall.

Want even more details? Meeting on LAssuranceRetraite.frThen View my career statement. Admittedly, you will not find the Agirc-Arrco points there, but this is where you will have the precise history of your salaries and other income, in euros and in francs!

The point on your trimesters… for long careers

The pension reform has not yet been adopted… But there is already a system for early departure for long careers and, unless surprised, it is not called into question at this stage. The reform just completes it. This Retirement Insurance statement lets you know if you have 4 or 5 quarters contributed at the end of the year of your 16 or 20 years. Important information to know if you tick the first of the conditions for a future early departure.

Why you should take a close look at your career statement

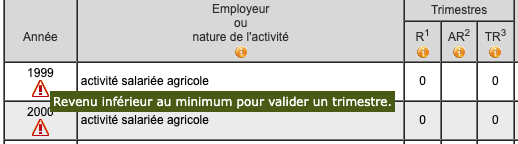

Check that all your professional experience is on this document, explains Valrie Batigne, founder of Sapiendo Retraite. In theory, everything is there, but we regularly get reports of omissions. Check, for example, that there are indeed 4 quarters each year… If there are not enough, you might as well take care of it now by sending supporting documents to the Retirement Insurance. Or by taking steps with a former employer if necessary.

How to point out any omissions?

I realized that I was missing 20,000 francs of salary in 1982 following a transfer (…) and that all my complementary points had disappeared (…) so yes there is interest in being vigilant and not waiting 60 years to look at his career statement, testifies for example Baboune on the MoneyVox forum.

Do not wait until 60 to look at your career statement

In a very detailed Frequently Asked Questions section, the complementary private insurance scheme Agirc-Arrco advises you to check that all the schemes to which you have contributed have recorded your information correctly: If before entering working life, you did odd jobsthese odd jobs may have enabled you to obtain rights (…) to the agricultural scheme for wage-earners (MSA) if you have done some seasonal agricultural workor dots Ircantec if you have given lessons or if you have been pawn in college or high school.

Ditto if in parallel with your salaried activity, or at the end of your career, you do some work or work assignments. consultant or if you have exercised artisan or merchant activityin which case it is necessary to examine points cipav Or ROI.

How to correct errors and omissions?

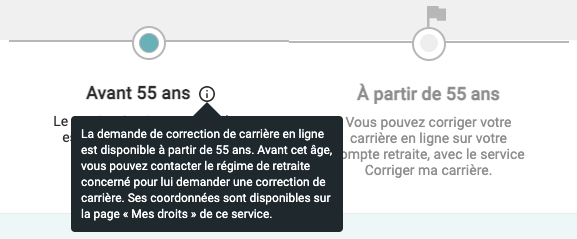

It all depends if you have more or less than 55 years old. If you have passed this milestone, bringing you closer to retirement, you have theoretically received a document entitled overall indicative estimate (EIG), which marks the start of scholarly calculations and corrections for retirement. If you are over 55, you can correct in detail your career statement on Info-retraite.fr and on the sites of the basic and complementary schemes.

Are you under 55? You will have to wait… But a detailed point in your career will now allow you to identify any errors or omissions. And to start hunting for missing documents now… rather than in 20 years when the organizations and companies concerned will have gone out of business (who knows?). Moreover, before age 55, if the correction is not available online, a substantial omission can still be corrected by contacting your pension plan directly using the contact information on Info-retraite.

Keep all your proof of income: ideally, scan all of them

Keep all your proof of income: ideally nothing should be thrown away and everything should be digitized, advises Valrie Batigne, of Sapiendo Retraite. If you forget or correct an error, you must, if necessary, provide supporting documents, point out Agirc-Arrco: pay slips or employer certificates, career statement from the basic scheme but also unemployment certificates, statements of daily allowances, continues the Pension Insurance.

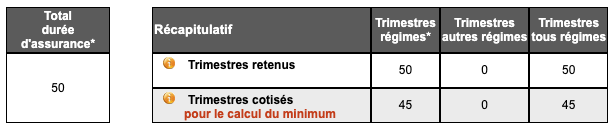

This discreet information to scrutinize in your statement

Do you also find it difficult to understand who is entitled to a minimum pension? Take a look at your Cnav (retirement insurance) statement, look at the table at the bottom of the statement: it details the number of quarters retained, in other words contributions and similar (sickness, unemployment, maternity, etc.) for the calculation of your rights and full rate starting age… and below the number of contribution quarters only, a more restrictive definition retained for your eligibility for the contributory minimum (MiCo)the basis of the famous promise of a minimum pension of 1,200 euros (gross, including supplementary, for a full career).

Why aren’t your 2022 quarters showing up?

Retirement points are calculated as the social declarations made by employers are processed, explains Agirc-Arrco on its site. The recording of the points acquired for an exercise takes place no later than the end of the following year. Do not panic, therefore, if your statement stops at the end of 2021.

Redeem incomplete quarters now?

Clearing your career path can be frustrating. Discovering that you needed a few hundred francs or euros to validate a quarter… Realizing that your first quarter with contributions is late… Are you wondering about buying back quarters? Indeed, buy tt cheaper side, but …

Redeem tt? You don’t buy back dearly but you don’t know what you’re buying back

If you buy back early, you do not buy back expensive but you do not know what you are buying back, cuts Pascale Gauthier, partner at Novelvy Retraite. Clearly, the uncertainties are such between now and your retirement, the uncertainties linked to the evolution of your career, but also the possible reform(s) that a takeover remains risky. For redemptions, or rather payments for retirement, insists Pascale Gauthier, I repeat: wait until you are sure you need it!

Retirement: buying back quarters, is it useful and how much?