Dax looks up

Year-end rally – is it coming or are we in the middle of it?

November 19, 2023, 11:30 a.m

Listen to article

This audio version was artificially generated. More info | Send feedback

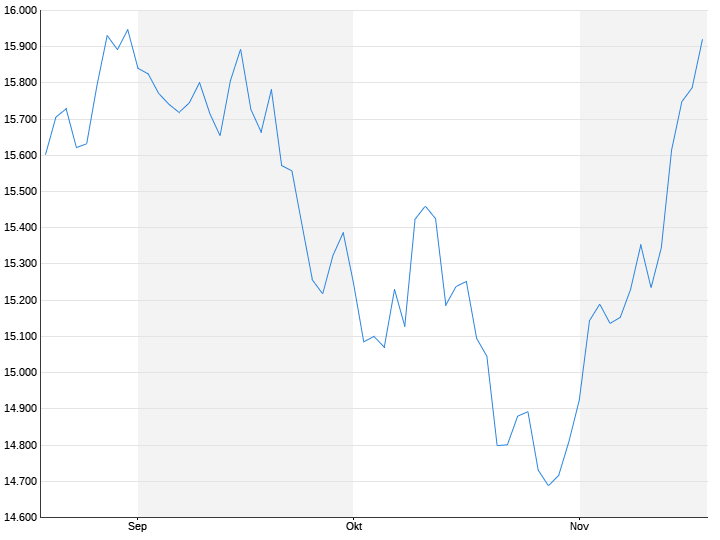

After the slump of the past few weeks, the DAX is making up ground again. The first investors are now already eyeing the annual high of a good 16,500 points. But will the recovery continue? Or is retail already slowly running out of steam?

After the strong November so far, the question of a year-end rally will likely continue to concern investors on the German stock market in the coming days. After three weeks of gains for the DAX, the air could be getting thinner, but experts are certainly optimistic about the continuation of the good run. Fund managers are overweight stocks in November for the first time since April 2022, according to a Bank of America survey.

On Friday, the DAX closed 0.8 percent higher at 15,919 points. On a weekly basis, the leading index was up 4.5 percent. “When fears of inflation and interest rates go, stocks come,” says Baader Bank expert Robert Halver confidently. This has the effect of “like a boost” on the stock markets. The expert sees the greatest catch-up potential in stocks from the MDAX and SDAX. While the DAX has gained around 14 percent this year, the increases of its smaller brothers amount to 5 and 11 percent respectively.

“Technically possible”

Due to the increase of almost nine percent since the October low, the 16,000 point mark is within reach again for the DAX. The leading index is now above the 200-day line – a positive signal. “There is nothing standing in the way of a year-end rally including new records, at least from a technical perspective,” says stock market expert Jürgen Molnar from broker Robomarkets optimistically. The previous record of just under 16,529 points dates back to July.

“Although the Fed (US Federal Reserve) for reasons of credibility raised their moral index finger in the form of a theoretical further interest rate increase,” said Baader expert Halver. However, the imagination for interest rate cuts is growing among investors. The first of a total of four interest rate cuts for next year from May is being priced into the futures markets. ” The slowdown in inflation, poor economic data and the fall in oil prices are fueling hopes of a significant change in central banks’ monetary policy,” says analyst Pierre Veyret from broker ActivTrades.

According to Commerzbank chief economist Jörg Krämer, the latest increase poses the risk that the rally will lose momentum. He referred to the DAX Relative Strength Index, which has reached the 70 mark – a level at which there is talk of an “overbought” market environment. “Fundamentally, the company analysts’ probably overly optimistic DAX profit expectations remain a key reason for us as to why the upside potential for the DAX should be limited in the coming months.” In addition, geopolitical concerns continue to be on the stock market’s agenda with the conflicts in the Middle East and Ukraine.

However, investors’ great hope is that the central banks will counteract excessively long and excessive tightening in good time in order to avoid a stalling of the economy. The monetary authorities, in turn, expect relatively high inflation rates to continue in 2024 and want to wait and see how this develops. “The cat-and-mouse game between capital markets and central banks is entering the next round,” says Bernhard Grünäugl, Head of Investment Strategy & ESG at BayernInvest.

Looking for fuel

There are a few events coming up in the new week that could determine the viability of the November rally. The experts at Landesbank Baden-Württemberg point to the figures from Nvidia expected on Tuesday after the US stock market closes, one – if not the biggest – beneficiary of the artificial intelligence trend. In addition, US citizens are likely to show during Thanksgiving week whether their “consumption is a viable support for the economy.” After the US holiday on Thursday, “Black Friday” once again serves as a signal for the particularly important Christmas business.

The Chinese central bank will decide on the key monetary policy rate, the so-called loan prime rate (LPR), on Monday. In order to strengthen the economic recovery after the corona pandemic, China has made several economic injections in recent months. The central bank has already lowered the reserve ratio for commercial banks twice in order to release more liquidity.

The corporate reporting season, on the other hand, is no longer a driving force. Capital market days of DAX companies could attract the interest of investors. At the beginning of the week, experts expect new medium-term goals from Rheinmetall, a beneficiary of the current rearmament. On Tuesday, there will likely be intensive discussions at Siemens Energy about the fact that the difficult situation of the energy technology group made government guarantees necessary.

Economic signals will be rare in the coming days. At the headquarters of the European Central Bank (ECB) there will likely be a close look at the beginning of the week when producer prices are due to be published in October. Most recently, the data indicated that inflation pressure was noticeably easing. That could happen on Friday IFO business climate index move. “The IFO business climate is likely to improve again,” says an outlook from Landesbank Helaba, following good omens from the ZEW index, which rose for the fourth time in a row in November. This is a positive signal for the IFO.