KDDI is one of Japan’s Big Three telecom operators, alongside Nippon Telegraph and Telephone (NTT) and SoftBank. In the mobile market, NTT was credited in 2021 with 37% market share, KDDI with 27.2% and Softbank with 20.8%. Note that the following figures are given in US dollars for better readability.

Mobile market share in Japan in 2021

Based on a price of 4,500 JPY per share (or around 34 USD per share), the group’s market capitalization is $73 billion, more than twice that of Orange, and its enterprise value — its market capitalization plus its long-term financial obligations — amounts to $84 billion. In terms of financial performance, we observe over the last cycle 2012-2022 that turnover has progressed little, but that margins have experienced regular expansion. This development is linked to healthy dynamics in the domestic market and the continued devaluation of the yen in international markets.

The return on equity fluctuates around 15%, a performance that is all the more satisfactory in that it is obtained with limited recourse to the leverage effect, since debt represents around a third of equity, whereas Orange employs as many debts than equity for a lower profitability. Despite the hyper-capital-intensive nature of the business, the generation of liquidity and the level of profitability make it possible to effectively hedge investments in infrastructure. Each year, approximately half of free operating cash flow can be used for acquisitions or returns of capital to shareholders.

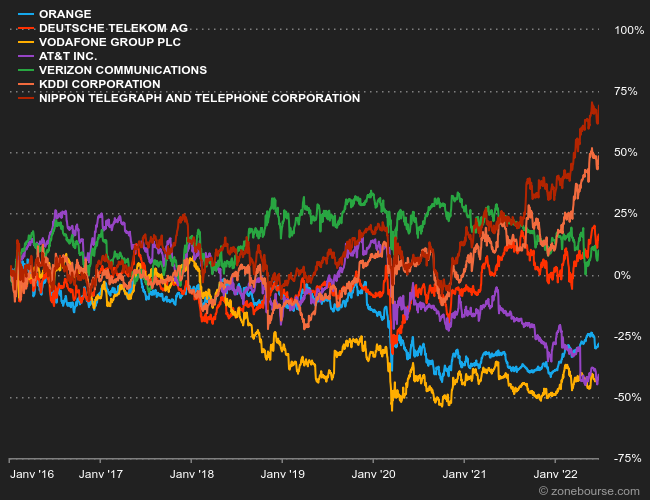

Since 2016, only KDDI and NTT stand out

$28 billion in 10 years for shareholders

Over the past decade, KDDI’s net income has doubled, the dividend has tripled and, a significant feature, the number of shares in circulation has decreased thanks to $10 billion in share buybacks in ten years. In total, some $28 billion has been returned to shareholders between 2012 and 2022. The operator is not particularly focused on external growth, since only $4 billion has been invested over ten years. This will be blamed on the lack of opportunities in a largely oligopolistic sector and on the conservatism of the industry. The valuation is aristocratic since it would take a quarter of a century to reach the current capitalization with the remuneration offered to shareholders over the last ten years. Not enough to jump to the ceiling therefore, unless there were significant growth prospects but this is not the case, on the contrary.

Despite everything, we are quite far from the problem of European operators, prisoners of a much too competitive market with more than 40 operators for 300 million users, where for a number of neighboring customers, the American market is shared between three operators . This ultra-competitive context on the old continent implies that operators achieve the lowest margins, and therefore cannot make their colossal investments profitable, nor generate sufficient profits to ensure both their development and high returns on capital to shareholders. . The Americans, like the Japanese, do not have this problem: with healthier dynamics in their domestic markets, they are able to self-finance their investments while ensuring comfortable remuneration for their shareholders.

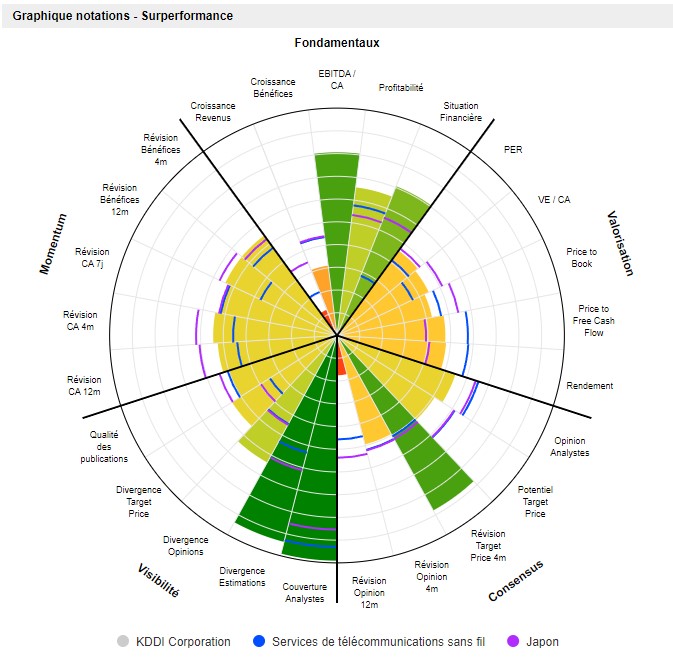

In terms of valuation, as we said above, the group is trading at a priori unattractive multiples of 14 times the profits expected next year, for a dividend yield of 3%. Apart from the defensive virtues of the case, based on the Japanese oligopoly and a good economic optimization, the attractiveness of the title is not obvious.