Some logos are recognizable among all. Nike monopolizes the runners-up in the brand awareness rankings. This popularity goes hand in hand with continuous growth for decades, fueled by a pricing power worthy of luxury brands. This successful business endures over time thanks to the power of the brand which gives it a competitive advantage without equal, except perhaps Coca-Cola and Apple.

A legendary brand

Like the competitive advantage of the famous soda and the apple phone, that of Nike is fueled by its powerful pricing power which generates colossal profits. A bit like perpetual motion, these profits are massively invested in advertising budgets which reinforce pricing power by constantly occupying the “mind share” of consumers around the world.

The almost perpetual motion of the Nike cash machine

Among the most important publicity vehicles are sports people, and those sponsored by Nike have provided the sport with the most legendary emotions. The best players in the history of the NBA Michael Jordan, LeBron James and Kobe Bryant, the greatest golfer of all time, Tiger Woods, the most popular footballer in history Cristiano Ronaldo or the tennis player with the greatest number of grand slams, Rafael Nadal. All of these legendary names helped and were helped by Nike to write history and boost the prestige of the brand.

By associating with the greatest athletes, Nike has anchored itself in the collective spirit as a brand synonymous with exceptional

His runner-up and historic German rival, Adidas, is obviously doing well and has solid assets. But Adidas will probably never have the reputation of the comma, with advertising budgets half as large. But make no mistake, Adidas remains an exceptional company with an international aura.

Sustained growth, but at a high price

Nike’s popularity can be seen in its financials. Over the last decade, Nike has succeeded in more than doubling its turnover, going from $20 billion in 2011 to $45 billion in 2021, representing an average annual growth of 8.45% per year for 10 years. Meanwhile, Adidas’ growth is at a much slower pace of 4.9% per year, pushing its turnover up from $13 billion to $21 billion. Illustrating the benefits of scale and better optimized cost structures, Nike’s operating margin (15.6%) is almost twice that of Adidas (9.35%), despite a lower gross margin. German advantage (45% for Nike, 50% for Adidas).

Evolution of Nike’s results

This financial health of Nike is also found at the bottom of the income statement, with a free-cash-flow multiplied by six over the same period. The group derives its strong growth from the American and Chinese markets, the largest in the world. However, one-fifth of sales come from the Chinese market, which may present a risk in the event of an escalation of geopolitical tensions with the United States. Adidas is not fortunate enough to benefit from such a dynamic European market, but its European cachet allows it to attract a more elite class of American consumers.

That said, both groups have excellent financial results. Nike uses more leverage (debt contracted to finance investments), which allows it to post a return on equity two to three times higher than that of Adidas, which manages its store like a European, it is that is, in a less aggressive way, as a “good family man”. Nike returns almost all of its profits to its shareholders in dividends and share buybacks. These redemptions are used in particular to cushion the impact of the abundant remuneration in stock options.

miracles

Nike, after a 40% drop since its all-time highs of last November, is currently capitalized at $162 billion, or around 30 times its free cash flow (fcf) of $5.2 billion. This represents an fcf (free-cash-flow yield) yield of around 3.2%. This valuation is hard to legitimize in the current context of rising rates, unless growth holds the same pace over the next decade as over the previous one. This is what is included in the price. However, ambitious is the investor who bets on a continuation of this trend. The Chinese market already seems well penetrated, and the brand seems to have pushed its pricing power to its climax, especially on the eve of a potential recession in the United States.

But hey, we are never safe from a miracle. Apple, for example, has already traded below 10 times its earnings twice in the past decade. Yet the brand was experiencing exponential growth while massively buying back its shares. A boon for investors. The miracles arrive on the markets, it is besides all their interest. Crowd movements cause sometimes ridiculous levels of valuation to be reached during massive sales phases, which then represent unexpected entry points.

Back to our comma. Nike would have been a perfect line in Warren Buffett’s portfolio, since it ticks almost all the prerequisites to be part of the legendary investor’s portfolio. Only the gargantuan compensation in stock options and its valuation, which was always too high, can explain its absence from Buffett’s selection.

Change in Nike and Adidas stock prices since January 1, 2020

What about Adidas?

Its rival Adidas also donates 4/5ths of its profits to its shareholders. The equipment manufacturer’s historically low valuations, however, prompted the brand to accelerate its action programs. The more pronounced fall (-50% since the all-time high of August 2021) of the German against Nike is undoubtedly due to its exposure to Russia and Eastern Europe, where Adidas is very popular. .

The growth of Adidas’ free-cash-flow follows the same trajectory as that of Nike, namely an average gain of 18% per year for 10 years. Adidas saw its free-cash-flow climb from $566 million in 2012 to $2.5 billion in 2021, and from $1.3 billion to almost $6 billion over the same period for the American.

Adidas’ capitalization barely exceeds $30 billion, ie a multiple of approximately x15 compared to profits (PER). This valuation seems attractive for an exceptional company whose activity is so long-lasting. If the PER reaches x10, Adidas would be a “no-brainer” investment, especially if share buybacks continue to accelerate.

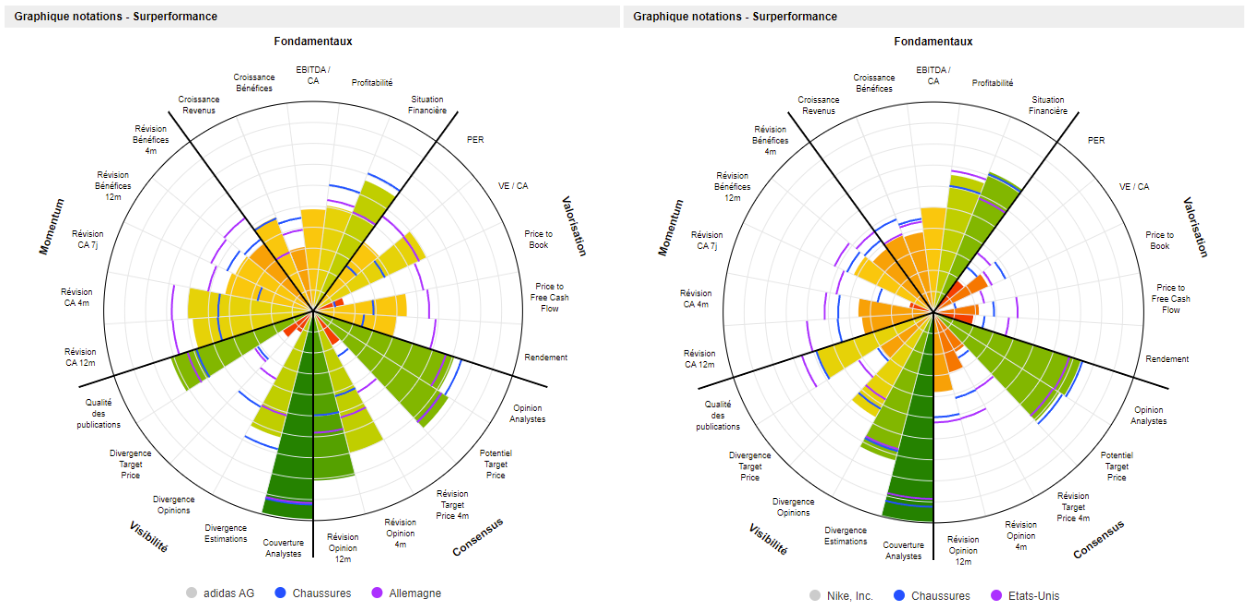

Marketzone ratings of Adidas (left) and Nike (right)

Eventually, it may be Adidas that will offer Warren Buffett the opportunity to make his first significant investment in sportswear and re-enter the European investment landscape, where Berkshire has been rather absent in recent years. Nike therefore remains quite expensive, but investors give it a reputational premium, betting on continued growth. Adidas, meanwhile, has entered opportunity territory but still presents a complete and solid picture, which ultimately does not have much to envy to its American rival. To be continued…