A system for guaranteeing the money deposited by individuals in bank accounts has been set up by the State. Since 2010, it has provided protection of a maximum of €100,000 per depositor and per institution, regardless of the number of accounts held. Should this ceiling be revised upwards? Yes, say 49% of French people according to a survey conducted by YouGov for MoneyVox.

If your bank fails, do you risk losing your money? After the sudden fall of Silicon Valley Bank on March 10, the debacle of Credit Suisse, the concerns about the state of Deutsche Bank and the stock market attack on BNP Paribas and Socit Generale shares in particular, you probably wondered about the soundness of the banking system and the consequences on your savings.

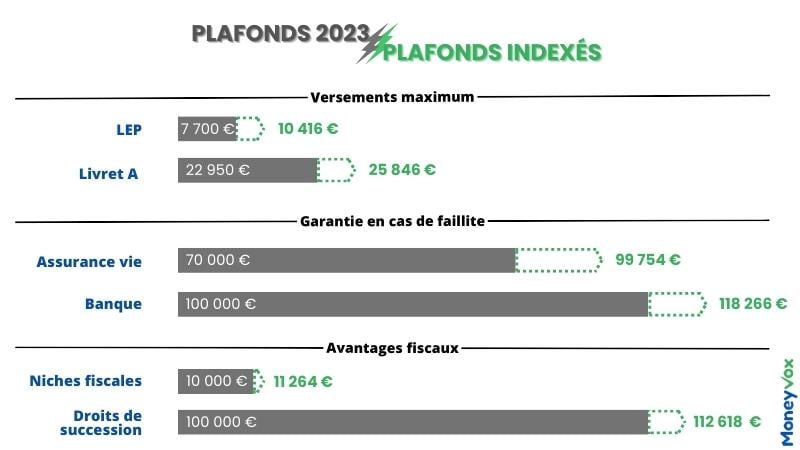

It is the Deposit and Resolution Guarantee Fund (FGDR), a public service body, whose mission is to protect customers in the event of their bank defaulting. In concrete terms, the FGDR offers a guarantee of up to €100,000 maximum per customer and per establishment, regardless of the number of accounts they have.

All about the deposit guarantee

An increase of 30,000 euros in the ceiling in 2010

Sums deposited in current accounts, bank books, home savings (CEL and PEL), youth savings accounts, term accounts and cash accounts for PEAs, PERs and employee savings plans are covered.

The guarantee ceiling was harmonized at 100,000 euros at euro zone level after the 2008 crisis because it was very different from one country to another. The customer of a French bank was protected up to 70,000 euros whereas in the Netherlands this guarantee was only 2,000 euros for example, recalls Christophe Nijdam, former banking analyst and author of Finance for dummies in 50 key concepts.

One saver in two favors an increase in the ceiling

For more than 10 years therefore, this deposit guarantee ceiling of 100,000 euros has not been reassessed. However, with the rise in prices, the amount of the guarantee suffered a sharp drop in terms of purchasing power. According the INSEE simulator which calculates monetary erosion due to inflation, the purchasing power of 100,000 euros in 2010 corresponds to 118,266.29 euros at the end of 2022.

In this context, should the guarantee ceiling be reviewed? According to a survey conducted by YouGov Institute for MoneyVox (1), 49% of respondents believe it should increase. Conversely, 22% believe that it should not move and 23% have no opinion.

For the economist Philippe Crevel, this ceiling deserves to be indexed so that it can monitor changes in income and therefore better protect the increase in household savings over the years. According to him, the question will arise: either we increase these ceilings in steps, or by an indexation rule.

It seems to me that the amount of the deposit guarantee in Europe should be increased to reassure savers and avoid a possible bank run. Look in the USA, the warranty is 250000 dollars (228,000 euros editor’s note) per customer and per bank and that did not prevent the bankruptcy of the SVB bank, adds Christophe Nijdam. Moreover, several American parliamentarians plead for a substantial increase in the guarantee of deposits to prevent future bank runs.

According to Aurlien Soustre, representative of the CGT-banques et assurances at the Consultative Committee of the Financial Sector (CCSF), the current guarantee in Europe is sufficient insofar as it is understood to be per customer and per institution: A joint account, held by two holders, therefore benefits froma guarantee of 200,000 euroswhile the same depositor with accounts in several banks has, each time, coverage of 100,000 euros per establishment.

A special guarantee of 500,000 euros

Note, however, thata special ceiling of 500,000 euros was added in 2015 for exceptional and temporary deposits. It applies in particular to deposits related to the sale of residential property belonging to the depositor.

Nevertheless the deposit guarantee ceiling is above all there to reassure savers and prevent him from withdrawing their money to put it under the mattress. France has six banks qualified as systemic (BNP Paribas, Crdit Agricole, Socit Gnrale, Crdit Mutuel, BPCE and La Banque Postale). These are banks whose failure would lead to the cascading collapse of other financial institutions.

And according to Jzabel Couppey-Soubeyran, lecturer at the University of Paris 1 Pantheon-Sorbonne recently interviewed by MoneyVox, the state will not let them down: These groups, which are not always virtuous, are those who are best protected by public power…These banks will be saved, and the savers will be saved with it!

Bankruptcy: these guarantees that protect your savings from a crash

A special guarantee for the Livret A

The sums saved on the Livret A, LDDS or LEP savings accounts are directly guaranteed by the State. This protection is therefore added to the deposit guarantee of 100,000 euros.

CASE. Savings: How Inflation Is Eating Your Benefits

(1) The survey was carried out on 1,005 people representative of the French national population aged 18 and over. The survey was carried out online, on the YouGov France proprietary panel from March 29 to 30, 2023.