Contents

A new maximum interest rate for consumer loans has been in effect since January 1st. What this means for borrowers.

What has changed in consumer loans since January 1st? Since the beginning of the year, the maximum permitted interest rate for consumer loans has been one percent higher than before and is now 12 percent. So if you want to borrow money in the short term, you may have to dig even deeper into your pockets this year. The increase was due to the in a federal regulation Calculation formula that has been established since 2016. The formula essentially says: If the general level of interest rates on the money market increases, the maximum interest rate for consumer loans also increases.

What are consumer loans anyway? Consumer loans are bank loans that borrowers can freely use to purchase consumer goods or services. These are not loans for professional purposes and, unlike mortgages for real estate, nor are they loans for investments.

Legend:

And money beckons forever.

Keystone/ALESSANDRO CRINARI

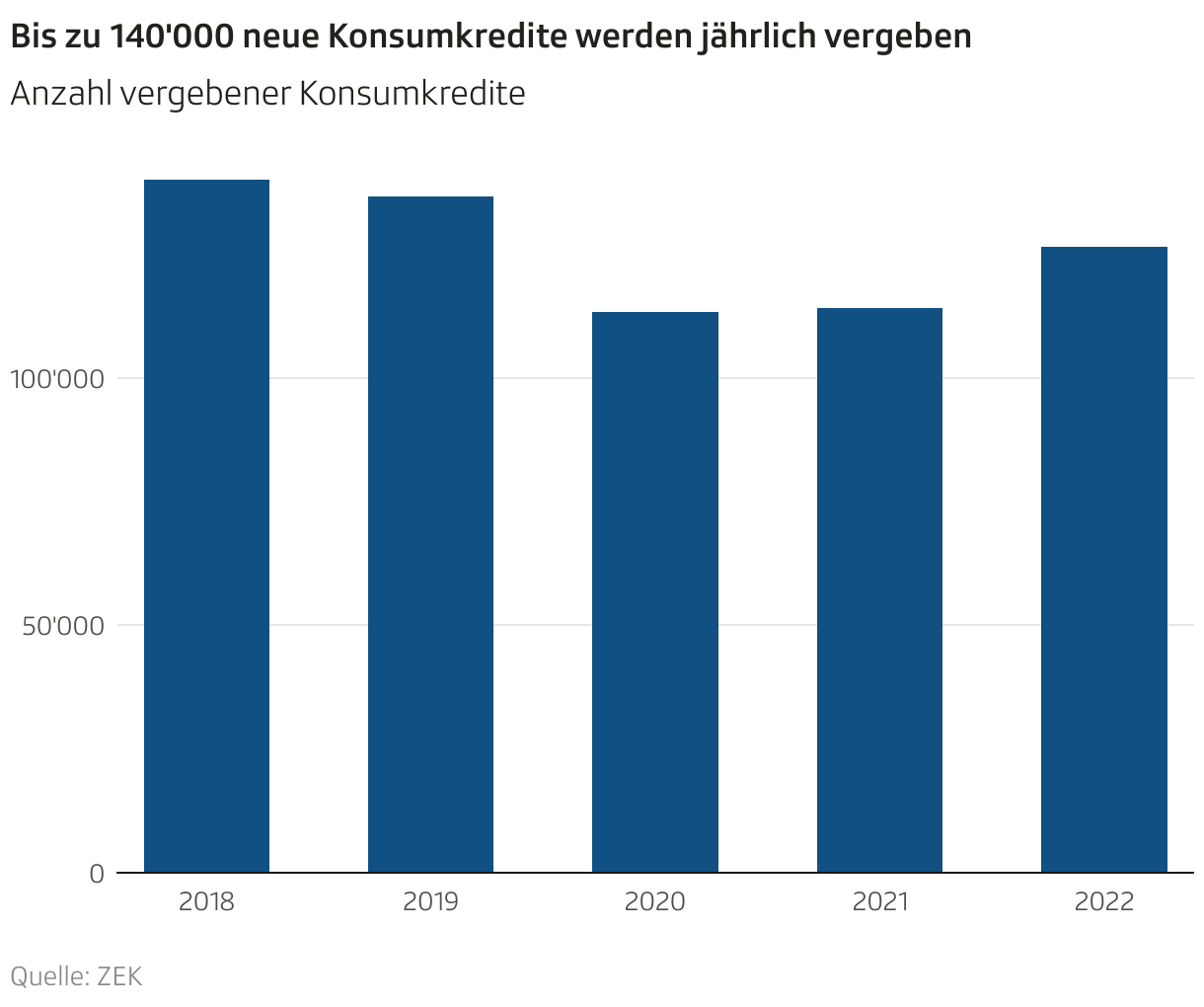

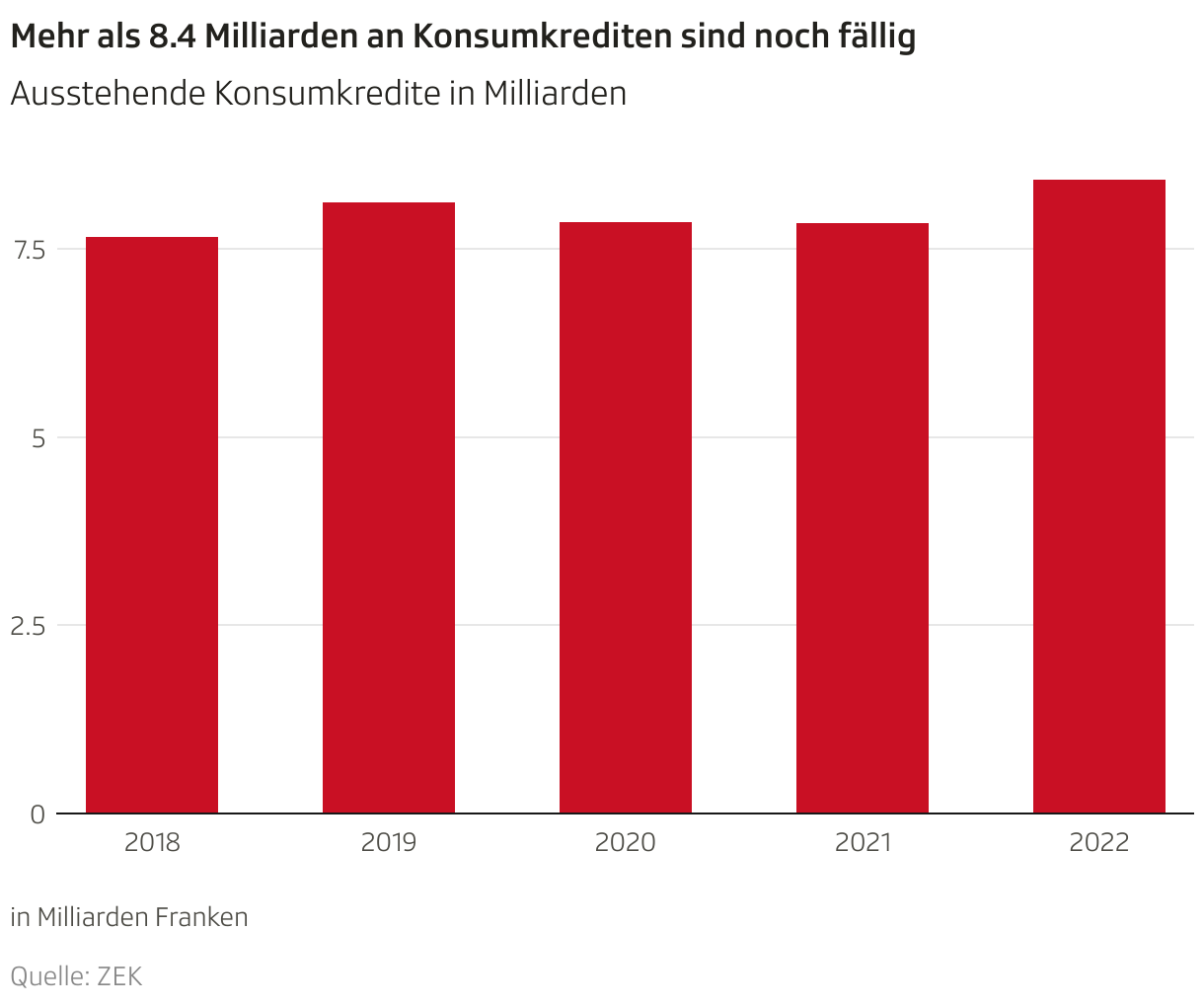

Switzerland, a country of debtors? Consumer loans are very widespread in Switzerland. According to the Association for the Management of a Central Office for Credit Information ZEK, exactly 126,347 new consumer loans were granted in 2022 (excluding leasing contracts). In total, the total of these loans amounts to more than 4.5 billion francs. At an average interest rate of 8 percent, the industry would earn around 360 million francs in interest in one year.

In total, at the end of 2022, there were exactly 357,564 consumer loans with a total loan amount of a good 8.4 billion francs. Figures from the Federal Statistical Office also show: In 2020, around 39.4 percent of the population lived in a household that had taken out some form of loan.

Who can actually get a consumer loan? Anyone who wants to take out a loan must prove their creditworthiness. This means that these people must prove that they can repay the loan and interest with their wages without falling below the subsistence level. That’s how it is Federal law on consumer credit law and the corresponding regulation regulated. They must therefore show that they can afford the rent, taxes, social security contributions, a basic amount for their living needs and any interest and repayment amounts owed for existing loans in addition to the monthly installments of the new loan.

Is the increase problematic for borrowers? For Pascal Pfister, managing director of Debt Advice Switzerland, the increase in the maximum interest rate comes at an inopportune time: “Anyone who needs a loan now has to pay more for it. This is an additional burden on top of the generally high level of inflation.” Because with the maximum interest rate, the average interest rates would also rise. He calls on politicians to reconsider the level of maximum interest rates: “It is questionable whether these are justified, given the amount of lenders’ profits and the low risk of default.”

The banks support increasing the maximum interest rate: For Daniel Alder, Managing Director of Consumer Financing Switzerland, the umbrella association of consumer lenders, increasing the maximum interest rate is unavoidable. Because: “Money market interest rates have risen. Our members have to refinance themselves on the market and borrow their money.” He also reminds us that the maximum interest rate was 15 percent until 2016. He also assumes that the market will play: “The average interest rates should be between 7 and 9 percent.”