Employee savings plans are a collective savings scheme offered by certain companies. The employer can pay each employee a bonus representing part of their profits, i.e. participation, and another bonus linked to the performance of the company (results, turnover, compliance with the social responsibility criteria of the company…), it is profit-sharing. Participation is compulsory in companies with more than 50 employees but optional for others. Profit-sharing is never compulsory.

Once the amounts have been determined by the company, the employee can choose to receive them directly or to place them in an employee savings plan. However, there are two prerequisites for opening an employee savings account:

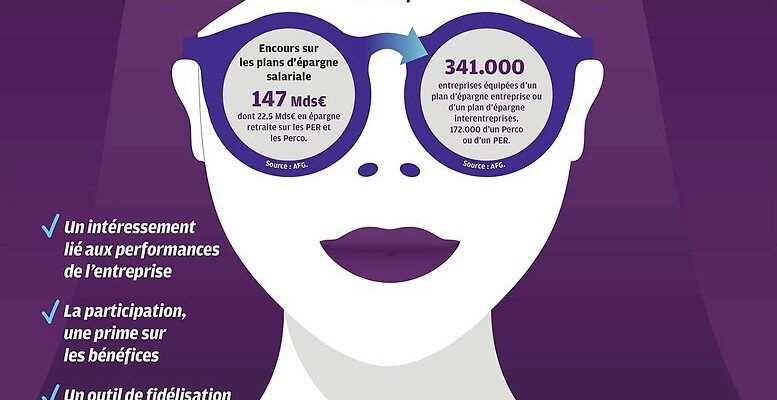

– the existence of a system such as company savings plan (PEE) and / or former collective retirement savings plan (Perco), or collective retirement savings plan (collective PER), set up in the company;

– when the company provides for it, it is sometimes also necessary to benefit from the seniority required at the time of payment to be eligible for the plan. This seniority cannot exceed three months.

The opening of an employee savings account takes effect from the first payment transaction on your savings plan, whatever the origin (payment or transfer from pre-existing systems). To make a payment, you can:

– or pay into the collective framework of your company, by responding to your annual notice of participation option and / or incentive that you will receive during the consultation period. It is generally possible to complete the process online or by post;

– or make an individual payment at any time. This voluntary payment comes from the personal contribution of the employee that the latter chooses to invest, on an ad hoc or scheduled basis. The company can also give an additional boost by supplementing your payments with a sum of money: it is the matching.

Premiums paid before June 1

Voluntary payments into an employee savings plan (PEE and / or collective Perco-PER) are capped depending on the support chosen. The profit-sharing and profit-sharing bonuses must be allocated by the employer at the latest before June 1, if the financial year is calculated over a calendar year. Finally, the sums you invest in employee savings plans are unavailable for a certain period of time, in exchange for tax advantages (read below), but it is possible to obtain the release in certain exceptional situations.

Our advice

Many employees do not know what to do with their employee savings plans. Find out if you have access to a PEE, to a Perco-PER, by whom they are managed, what the fees are and what they earn. Arbitrate between the different investment funds offered.