Today we are going to talk about rates, and to avoid repeating myself and incidentally boring you, I suggest that the curious read another dedicated article on the subject of short rates, long rates and the transmission of monetary policy to the real economy if it is not yet clear to you. Rest assured, even the greatest economists still have doubts.

Here I will simply repeat part of it, which precisely concerns the difference between a fixed rate and a variable rate.

“Fixed rates and variable rates

In all circumstances, there are two possibilities of debt financing. If the economic agent chooses a fixed rate, he borrows an amount for a period and an interest rate determined in advance. By choosing a variable rate, he can observe an evolution of the interest rate until the maturity of the loan. Choosing a variable rate rather than a fixed rate or vice versa amounts to anticipating a change in the economic context (activity, inflation, monetary policy, etc.).

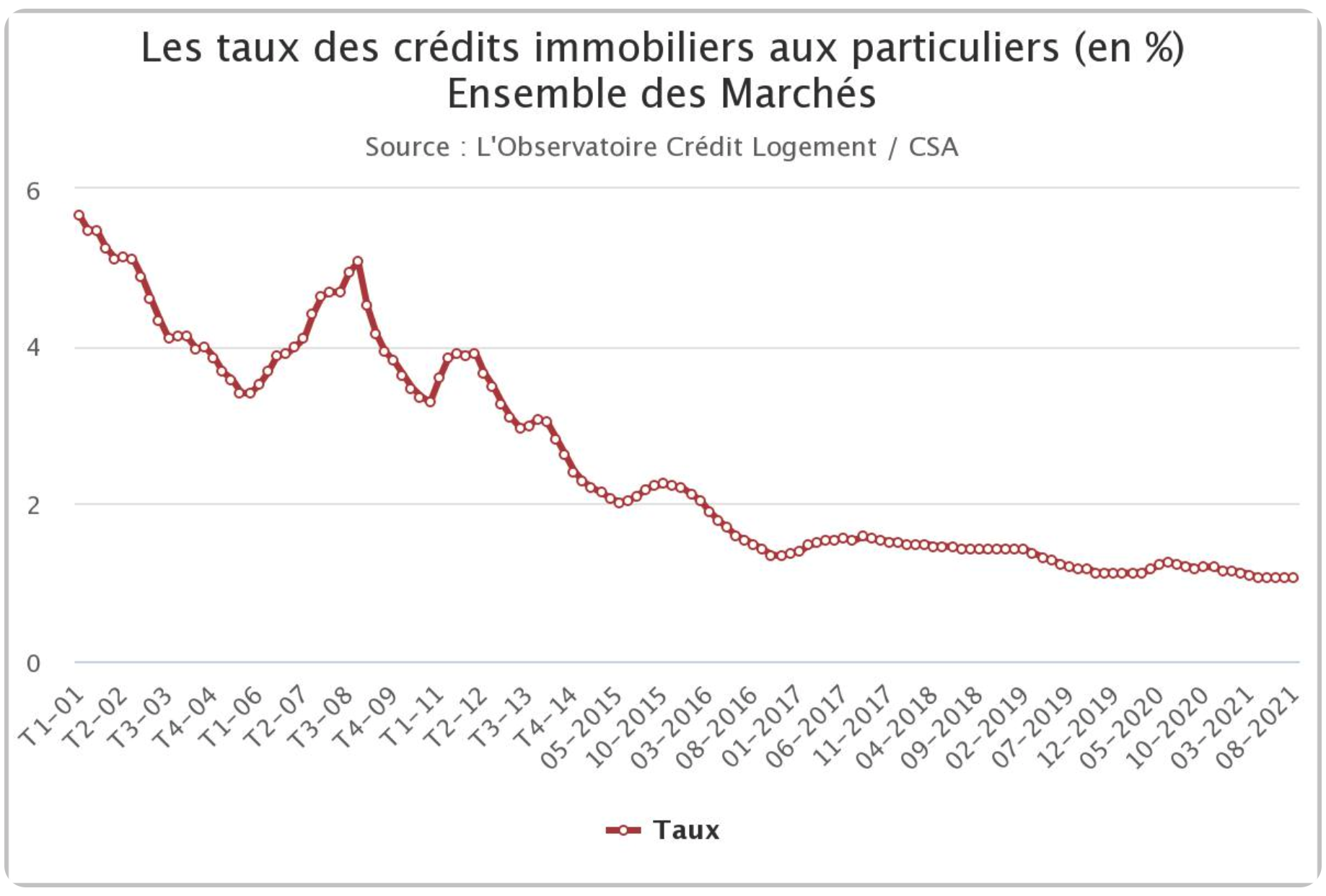

We then understand that when we choose the option of the variable rate we cannot be certain (in other words: we have no idea) of the cost of the loan to which we are subscribing. Moreover, the longer its duration, the more this observation is confirmed (despite the downward trend of recent years, we can observe a good number of rate cycles in the space of 20 years)

Source: Statista

Source: CSA

We then wonder which households are crazy enough to finance themselves at variable rates!

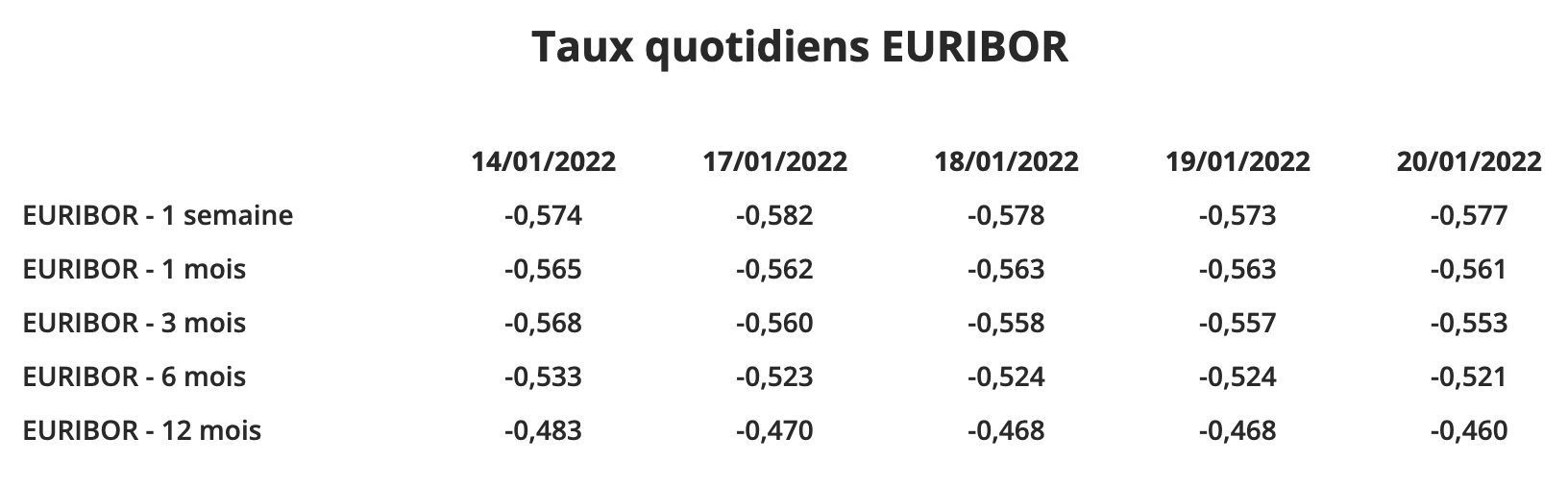

In fact, there are a few advantages. Generally, the indicator on which commercial banks rely to determine the cost of borrowing at variable rates is the Euribor rate (see the article cited above if your reaction was of the type: Kesako?). Rate to which they add their margin, often between 1 and 2%. The fact is that this amount is in most cases lower than the fixed rate that would be offered to you for financing with equivalent characteristics. However, be careful, we are only talking about the first deadlines! Remember that this is a variable rate.

Source: Bank of France

A variable rate can therefore be attractive for a short-term loan or for the financing of a very liquid asset that has been purchased with the aim of reselling it in the near future because it is possible to repay it. in advance without paying penalties.

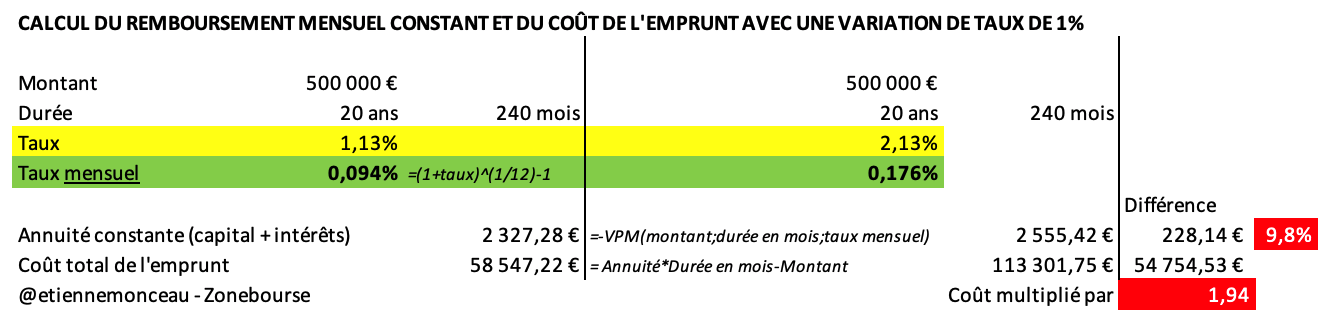

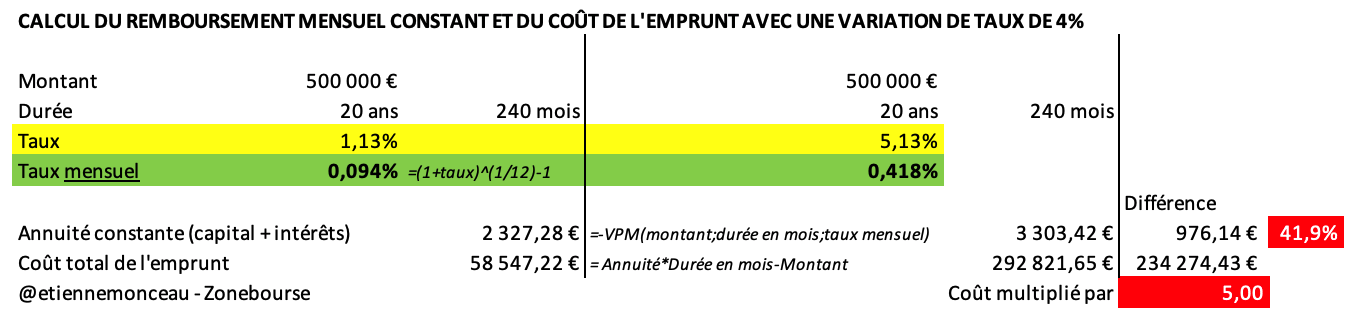

To understand the effect of a rate hike on the monthly payments that the household must pay to its bank, I threw myself into my Excel file to simulate a few amortization plans (I’m nice, I’ve given you the formulas). To simplify things, I’m only interested in 100% financing of a property worth €500,000 over 20 years and I have fun varying the annual fixed rate. In the first case (variation of the rate from 1.13% to 2.13%), we note that the total cost of the loan is multiplied by 1.94! Monthly payments increase by 9.8% from €2,327 to €2,556. In the second case (variation of the rate from 1.13% to 5.13%), the total cost of the loan is multiplied by 5! Monthly payments increase by 41.9% from €2,327 to €3,303.

Simulations of monthly payments and the total cost of a loan with different rates. Zonebourse.

Obviously, to be more precise, it would be necessary to take out the detail of an amortization plan by integrating a progressive rate variation, but it is far from being essential to get the message across.

If it was not yet for you until now, it is now obvious: the impact of a rate increase is colossal on the household budget. This is also one of the triggers of the subprime crisis.

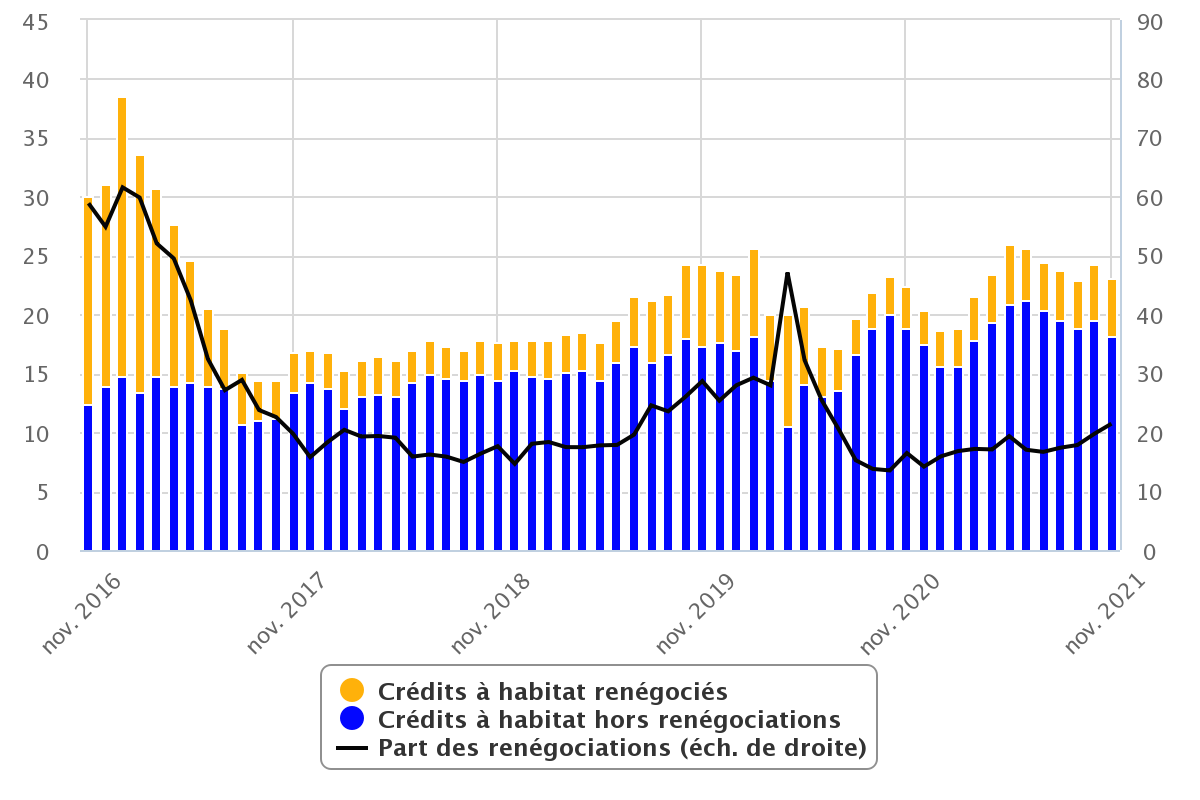

In France, even if it is quite possible to borrow at a variable rate, few people still use it, especially when the rates are very low and it is possible to renegotiate your credit, even when we took a fixed rate (how beautiful the competition).

Share of renegotiations in home loans in France. Source: Bank of France

However, in other countries, choosing this type of financing is more common. It is on this point (the share of variable rate mortgages) that it is very difficult to find data (spoiler: I ended up finding it anyway).

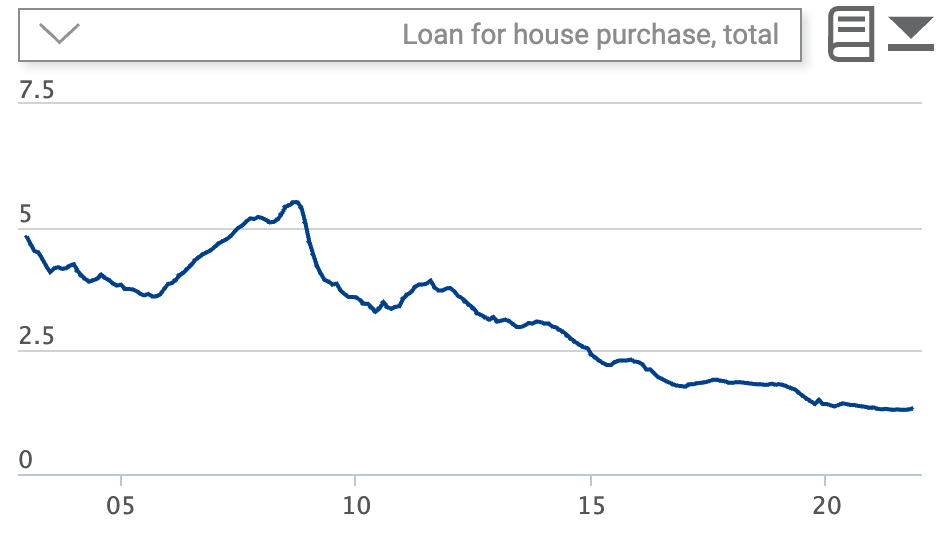

In 2002, according to Eurostat, more than 70% of mortgages were at variable rates in England, Germany, Portugal, Spain and Finland. But things have changed and the average real estate rates in Europe have fallen from 5% to 1.3%. Interest in the variable has therefore diminished.

Evolution of the average rate of real estate loans in Europe. Source: EuroAreaStatistics

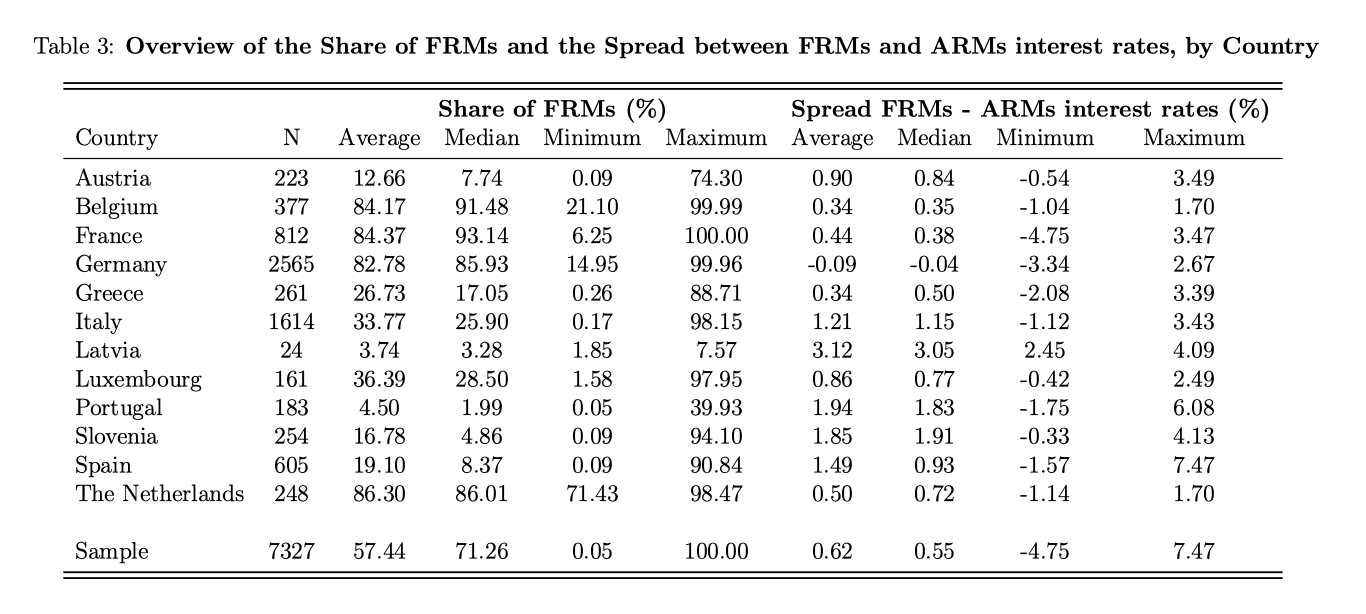

Today, the euro zone countries that use fixed rates (FRM = Fixed Rate Mortgages) the most are Belgium, France, Germany and the Netherlands, while the countries that use variable rates (ARM = Adjustable Rate Mortgages) are Austria, Greece, Portugal and Spain. This heterogeneity also has consequences on the transmission of the ECB’s monetary policy in each of these countries and on their financial stability.

Share of financing (all types of loans combined) at fixed rates and average difference between fixed and variable rates in %. Albertazzi et al. European Central Bank

Outside the eurozone, even more exotic modes of financing can be found. In Australia, for example, financing at a fixed rate over 2 or 3 years which then turns into a variable rate until maturity seems to be widely adopted…

Through these few paragraphs, we have therefore returned to the notions of fixed rate and variable rate to initiate a beginning of reflection on the effect of a rise in real estate rates on the household budget as well as the economic risk linked to rates. variables. To be able to conclude anything on the subject, much more important work would be possible, but that is not the objective of this “awareness” article. It is also important to remember that an increase in the key ECB rates (short rates) does not have a direct influence on the real estate rates of commercial banks, the transmission of monetary policy to the real economy is far from complete. be obvious. However, we know very well that this is what awaits us and that it is a necessary measure to avoid the creation of a real estate bubble that is too flagrant for everyone to miss.