A few years ago, a family friend tried to evangelize my grandfather on an infallible stock market technique: betting on the great talented captains of industry. I still remember the way in which he praised the merits of Serge Tchuruk, whom he knew well for having frequented him on the benches of l’X. Grateful for the tip, the grandfather had filled his portfolio with Alcatel stocks at the turn of the millennium. Well obviously, badly took him.

What is the relationship with Danone? I’m coming. Serge Tchuruk left his position as boss of Alcatel in 2008 after a bitter failure. That same year, Emmanuel Faber became number two at Danone, a group of which he will take sole reins in 2014. A strong personality, the successor of Franck Riboud. A little guy from Grenoble, in love with the mountains and with clear ideas on the strategy to be followed. A leader with whom we want to embark.

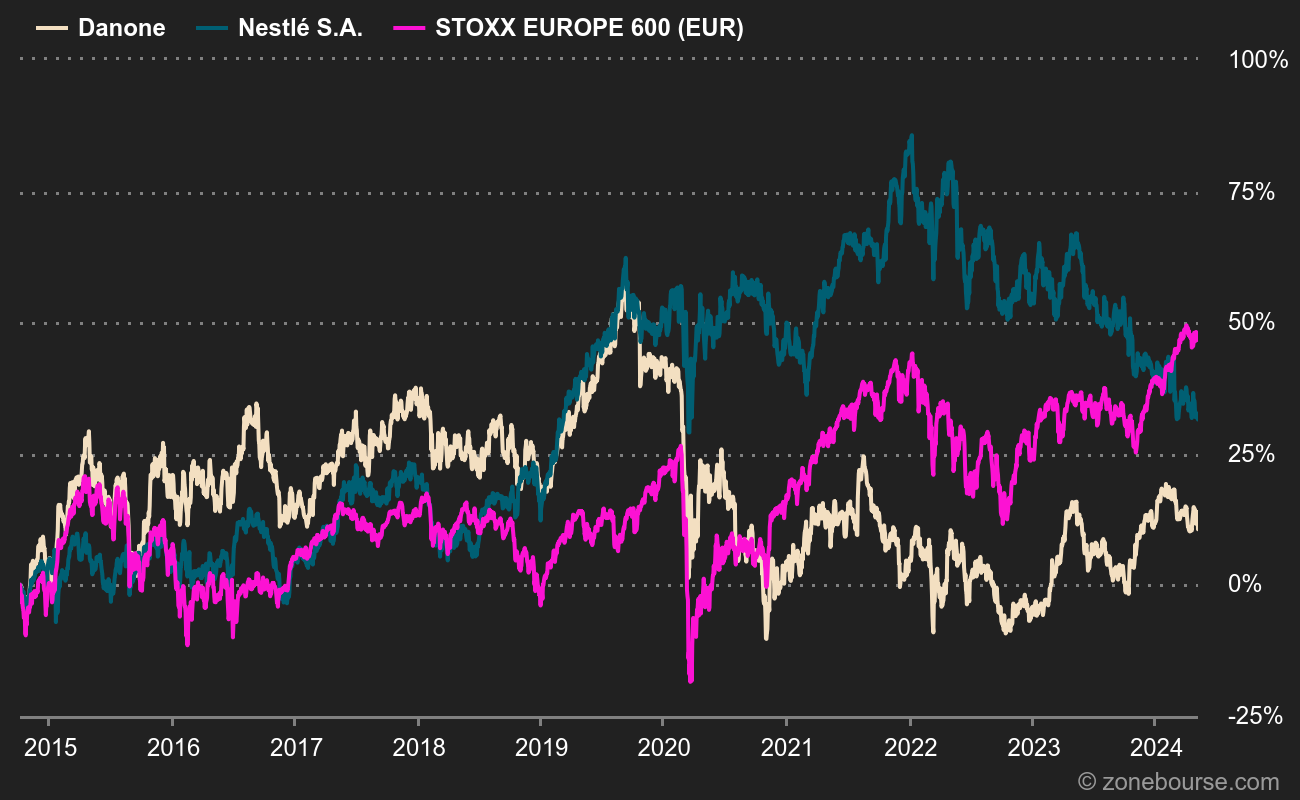

Yes, but here it is, Faber was resigned a few months ago, for lack of a sufficiently convincing balance sheet for its shareholders. We are far from the Alcatel mismanagement that said, but it has floundered a little in the Activia anyway. Between 2008 and 2021, Danone shares increased by 35% including dividend payments, or 2.2% per year. It’s better than the Livret A, but it gets stuck when we compare the performance with the STOXX Europe 600 NR index (dividends reinvested), which gained twice as much (4.7%). Worse, since the arrival of Faber alone at the helm (the 1er October 2014), the stock grew by 3.08% per year including dividends, against 7.2% for the STOXX Europe 600 NR. Excluding dividends, Danone shares have been declining since 2008 and symbolically increasing since October 2014, as shown in the two charts below.

The journey of Danone, Nestlé and the STOXX Europe 600 since 1er January 2008

The journey of Danone, Nestlé and the STOXX Europe 600 since October 10, 2014

What is also very visible because I added another action out of pure nastiness is that the balance sheet is even more unfavorable compared to Nestlé (whose action has gained 11.7% per year on average since 2014 including dividends). Emmanuel Faber must have heard hundreds of times “yes but during this time, Nestlé has done much better“. In fact, the stock market performance of Switzerland is (much) more favorable. The two leading agribusiness companies in Europe are still compared even if their profiles have significantly deviated in recent years. Nestlé has developed Nespresso and nutrition animal and has arbitrated its traditional trades, while remaining positioned in the water. Danone has remained on its fresh dairy products and its mineral waters, by focusing on specialized nutrition (medical and infantile). Of the two groups, this is the Switzerland who made the best choices in the eyes of the market.

Commodity of products

Overall, analysts criticize Danone for being positioned in difficult markets, especially dairy products where competition is raging and where “commoditization” threatens (understand trivialization, which undermines the ability to maintain good margins). Even on the Danette! Danone’s average organic growth was around 1.9% over the past five years, compared to 3.1% for Nestlé. This may be a detail for you, but for analysts it means a lot. In addition, the design offices find that the group does not have any particularly attractive assets, which could play the role of a locomotive, unlike Veveysan with its pods and kibbles.

To make matters worse, Emmanuel Faber had decided to make Danone a company with a mission. That is to say, to give it a social and environmental purpose, and consequently create constraints and binding objectives. The shareholders had approved, after all it was a great idea. But investors quickly tire of great ideas if they don’t translate quickly into stock market performance. The ESG is well in the annual report and displayed in the metro. If it starts costing money, that’s something else. Moreover, and this is a real problem, we do not know how to value and even less improve on the stock market practices that will bear fruit in the long term, especially on the basis of a multi-factor approach that would combine the environment, the social and other subjects which are impossible to quantify simply. But that’s another subject.

Danone has been dragging its reputation as the bottom of the class for several years. There were a few flashes of lightning that suggested the band was starting their resurrection, but hopes have always been dashed so far. This is reflected in a relatively low PER for the sector: 16.7 times the expected results in 2022, then 14.3 times two of 2023. The star Nestlé is respectively 27.6 and 25.6 times, that is to say . Unilever, Mondelez, Reckitt and the rest of the clique are also better regarded. A look at the fundamentals shows that growth is weak and that the financial situation is not particularly an asset. Revisions to turnover and profit are correct, nothing more. In short, not enough to make an orgy of Actimel nor to get drunk in Evian water.

“Should not invite him” identifies rather qualitative companies that are going through a complicated patch on the stock market. You never know, they could get over it! The latest articles in the section: