What makes the Peloton brand more desirable than others in the eyes of the public is this blend of health and technology. As for the investor, he had something to be seduced by the subscription side, potential source of recurring income and the techno-social dressing. To top it off, Peloton went public at the end of 2019, that is to say just before the start of the coronavirus crisis. Stamped “pure Covid value”, since part of humanity was condemned to play indoor sports, the company benefited from unreasonable enthusiasm, both commercially and on the stock market.

A Peloton bike (Source Company)

From its introductory price of 29 USD, the title rose to 171.09 USD on January 14, 2021. Enough to multiply its stake by six or almost in less than a year and a half. Not bad for a company that has never earned the beginning of a dollar and shouldn’t do so until at best the year 2025. That said, the activity is real: turnover has increased from 915 M€ in 2019 to 4.02 Md€ in 2021, of which 21.7% now comes from subscriptions.

For a shareholder who subscribed during the IPO or until the spring of 2020, it’s the jackpot. For the latecomers, it’s the collective fall: the share fell to 31.33 USD, which makes Peloton the most calamitous American stock with a capitalization of more than $5 billion over a year, with a -80 % that makes a mess. The stock is currently trading around USD 31.30.

Don’t throw any more

The history of Peloton for a year is paved with bad news. First, covid-values were no longer popular in 2021, after having crushed everything in their path the previous year. Then, it was necessary to warn about margins because of the increase in freight rates. Then a child died when a treadmill was mishandled. In the aftermath, the US Product Safety Commission issued a warning about the mat after reporting 39 more or less serious incidents involving it. After procrastinating, Peloton ended up recalling all the carpets sold, at a cost of $165 million. Then the results for the year ended at the end of June were marked by a much heavier loss than expected. As for the 2022 projections, they largely disappointed analysts when they were announced. They were also lowered in November. Then Peloton sued Lululemon, who counterattacked. Before a controversy in relation to actor Chris Noth, fallen ex-hero of Sex and the City. In short, the crisis of growth has turned into a nervous breakdown for the company and its shareholders.

Unattractive fundamentals

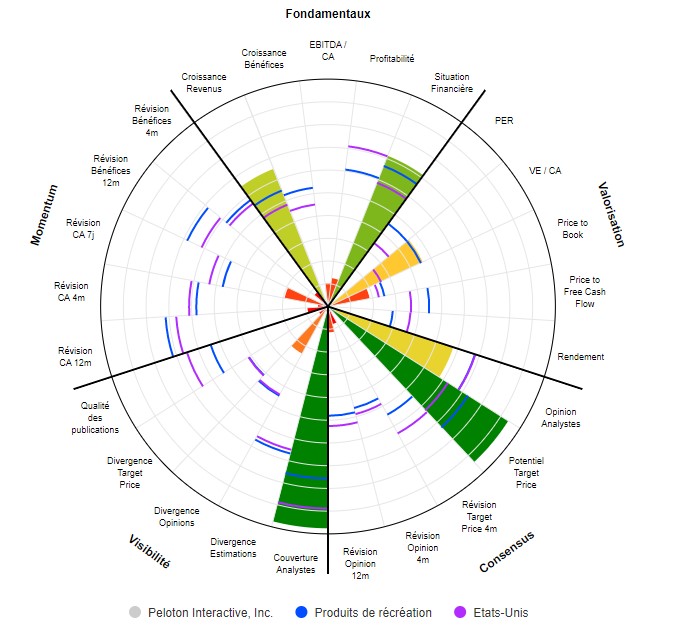

Going back to more basic considerations, what do the fundamentals of the business look like? To nothing. Well, not much. So of course, the balance sheet is quite solid and revenue growth is interesting, but the margins are not keeping pace for the moment and the profits, as I said above, will not be there before 2025 if we consider relies on the analysts who follow the file. The result revisions are bad, as the warnings have come and gone. The quality of publications naturally suffers. Finally, the valuations assigned by analysts range from simple to triple, or even a little more. A disparity that affects the readability of the file. Even the small rumor of predation by Apple which is going well did not manage to wake up the course durably.

“Fallait pas l’invite” identifies rather qualitative companies that are going through a complicated period on the stock market. You never know, they could recover! Latest articles in the section: