I went a little far to introduce this period during which a lot of companies went bankrupt. But internet startups weren’t the only ones struggling. I remember that in 2002/2003, two companies that are well known today almost disappeared: the industrial company Alstom and the reinsurer Scor. In fact, if you look at a 22-year chart, both stocks have lost over 90% of their value. Under the leadership of leaders as talented as they were divisive, who moreover had complicated ends of mandates, the two companies had managed to raise the bar.

Regarding Scor, it was Denis Kessler who pulled off the feat of putting the French reinsurer back on track to bring it up to the level of its rivals. His Alstom counterpart Patrick Kron had also put his group back on track, literally with the sale to General Electric of the group’s energy assets, an operation that has caused a lot of ink to flow since. But let’s forget Alstom to focus on Scor.

From the moment the reinsurer’s recovery plan began to operate, that is to say in the summer of 2004, the stock experienced a prosperous period since it quadrupled until reaching its peaks in 2018, around 44 EUR. A remarkable turnaround, which brought the company back into the global elite.

The main global reinsurers, by written premiums

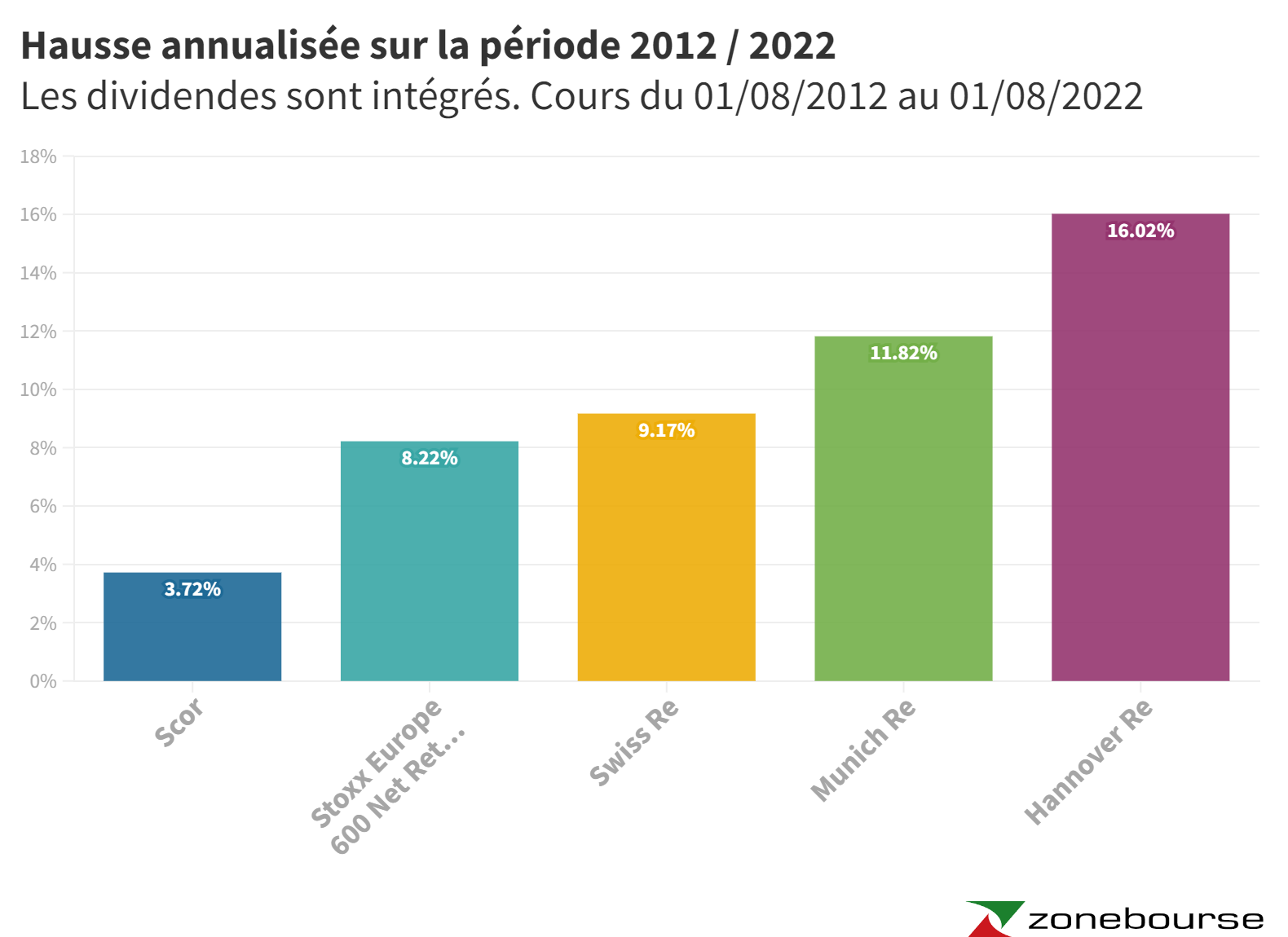

But over the more recent period, it is rather grimace soup. So much so that the action lost 37% in 2022, but also 53% over 3 years. Over 10 years, the balance is -11%. I should point out, however, that Scor pays a rather generous coupon, which significantly improves stock market performance. Thus, by integrating the coupons, the balance sheet remains positive over 10 years, although far removed from the competition or even from the Stoxx Europe 600 NR.

Over 10 years, Scor’s career has suffered from comparison with its competitors and even with the global market

How to explain the recent decline?

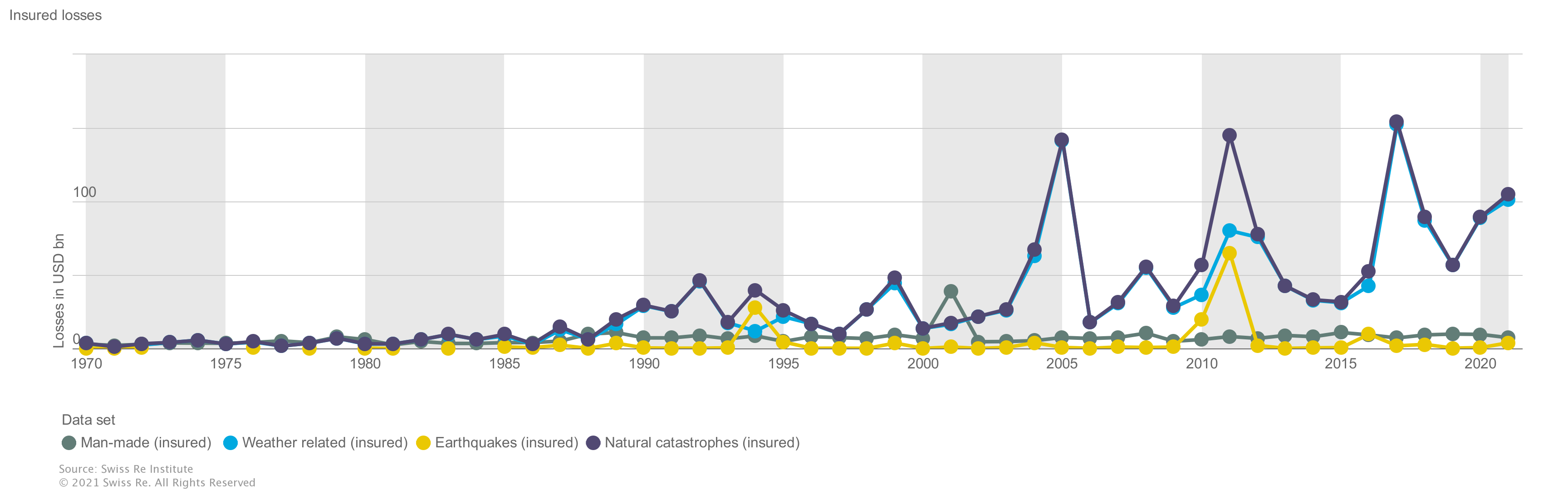

The stock fell sharply last week after the announcement of surprisingly weak half-year results. The accounts bear the scars of the drought in Brazil and the war in Ukraine. “It is a very difficult quarter for Scor, which comes on top of an already failed first quarter and which translates into a very disappointing and worrying first half.“, recognizes Grégoire Hermann, who is following the case at AlphaValue. Especially since the weakness now comes from the P&C branch (damage), while it is the L&H division (life and health) which has been struggling until then. “Although we want to believe that Scor correctly assesses the risk it bears, the reality has been different so far, and has been for several years.“, worries the analyst.

Evolution of insured losses since 1970, by type of claim (Source Swiss Re)

The other element that frustrates investors is credit strength. The rating industry may have taken the lead in the wing after its appalling compromise in the financial crisis of 2008, it remains nonetheless crucial for certain sectors, including that of reinsurance. Scor’s ratings have been under scrutiny at S&P and Fitch since this year. Granted, S&P confirmed the “AA-” rating on Friday (lost what those codes mean? A quick explanation here), but the agency doubts the company will meet its profit expectations this year. However, it seems to give him the benefit of the doubt, and a delay until the half-yearly results of next year to demonstrate that the corrective measures announced will bear fruit.

The research firm Jefferies points out that insurers are naturally attentive to the rating when choosing their counterparty. And top-rated reinsurers have superior pricing power. The credit rating recovery spiral between 2004 and 2015 should not be reversed. For the record, S&P rated Scor’s debt “AA-” in 2000, then “A+” in January 2002. The situation deteriorated so quickly that the rating went to “A” at the beginning of October 2002, then to “A -” at the end of October 2002 and “BBB+” in July 2003. In November, S&P downgraded the reinsurer by two additional notches to reduce it to “BBB-“, the lowest rating in the investment category. The situation would have been devastating if the credit rating had gone to junk, but the infernal cycle ended then and the group began to regain levels of financial solidity. From “BBB+” in December 2003 to “AA-” in September 2015.

We will therefore monitor the comments of the agencies that follow the Scor (S&P, Fitch, AM Best and Moody’s), as they will constitute an important marker of the stock’s performance. In the meantime, despite the large dividend, which represents a yield of around 10/11% on current prices, the file is not in the odor of holiness on the stock market. Because investors know full well that if more resources have to be devoted to strengthening financial solidity, it is the remuneration of shareholders that will suffer the consequences.

“Fallait pas l’invite” identifies companies that are going through a complicated period on the stock market. You never know, they could recover! Latest articles in the section: