But AT ONE TIME, it was true. True cash machines, with high barriers to entry and flourishing prospects for the digital industry, satellite operators were sought-after fund stocks. In particular the two French companies, Eutelsat and SES SA At this stage, our Luxembourgish readers are entitled to be offended because SES is Luxembourgish, not French, even if the company is listed in Paris. I emphasize this because I was wrong about the nationality of the company almost 15 years ago when I was working for another media, which had earned me a bit of a salty official letter. In particular on the systematic appropriation of French-speaking societies by these French pigs, while I myself am only a Savoyard pig (the term is not pejorative here, since we venerate the pig).

The SES fleet (Source company)

SES so. A scent of space conquest, with ASTRA satellites in orbit for more than 40 years. The group offers large-scale transmission services that make it possible, for example, to distribute video content and data or to provide government organizations with secure networks for their telecommunications. Turnover is split between the video branch (59% of revenues) and the network branch (41%). The three countries contributing the most to income are the United States (31%), Germany (19.5%) and the United Kingdom (12%).

On its website, SES claims coverage of more than 1 billion viewers, provision of services to 7 of the 10 largest telecom players and a portfolio of 58 government agencies. There are 71 satellites of the group currently in orbit, which does not look very impressive compared to the armada of a newcomer like SpaceX, which already has 1,655 satellites in space, according to the tally of the SCU. But mini-satellites in low orbit whose role differs from those of SES. But the figure gives an idea of the ability of competitors to disrupt the market, as we will see later.

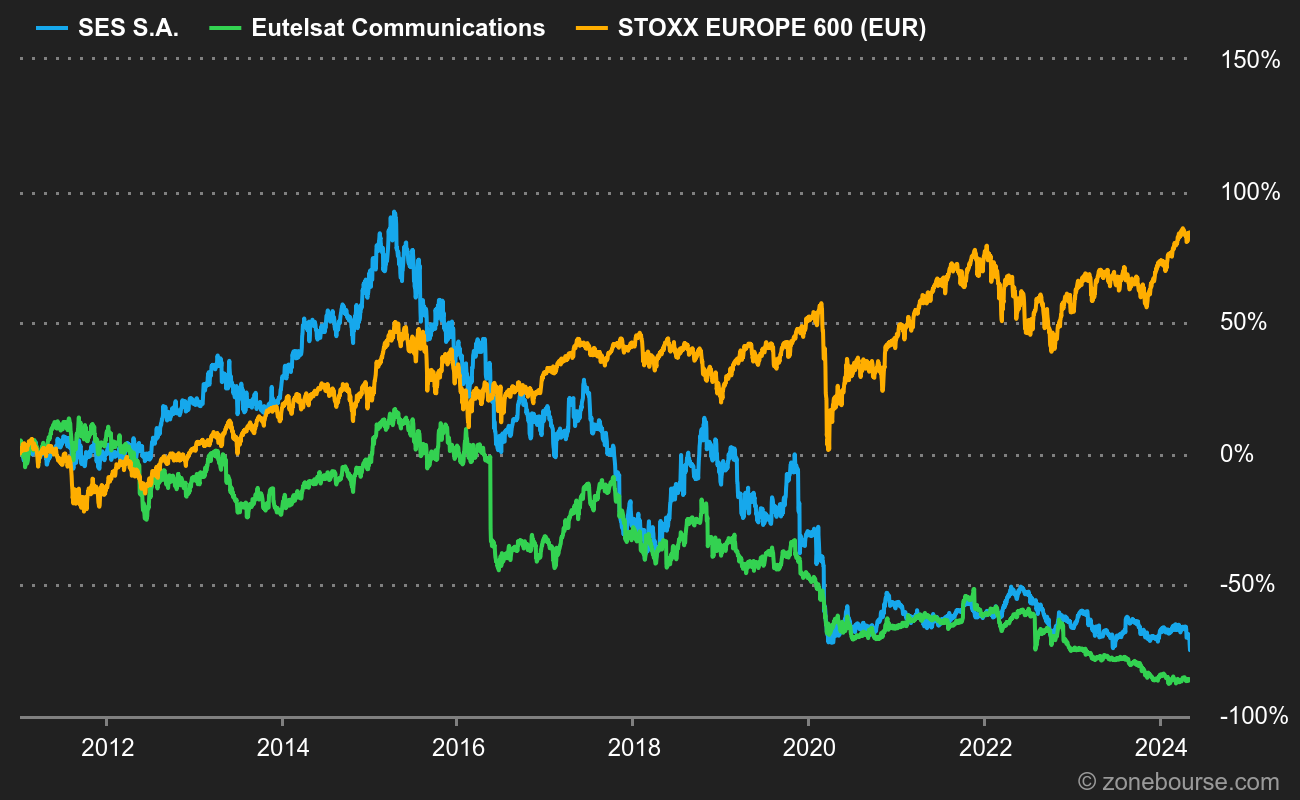

The golden age of satellite operators ended less than ten years ago. Before that, they had taken advantage of a situation of oligopoly, complicated access to space and severe regulation to impose high prices and ensure a good income. An income which was also the counterpart of the high capital intensity of the activity and the risks induced by space launches. The economic model conceals another diptych: long contracts that allow high indebtedness. Or rather who authorized, since the industry entered a new phase a few years ago which destabilized the leaders of the sector, and which explains why the action fell from 35 EUR on April 14, 2017 to less than 7 EUR currently . Which of course earned him to end up in our “need not invite him” section, despite a not insignificant rebound from the lowest point signed in March 2020 at 4.87 EUR. Over 10 years, the stock has lost an average of -8.42% per year. A liability reduced to -3.5% per year including dividends, but a liability nonetheless (over the same period, the STOXX Europe 600 gained 6.8% per year on average, and 10.37% including dividends).

Low orbit

The paradigm shift in the sector came about as a result of technical progress in data transmission. Terrestrial networks have become more powerful and more extensive, reducing customer dependence on incumbents. New launchers have appeared, new operators too. Progress has made possible the miniaturization of satellites and the use of new orbits. Some historical players have gone bankrupt, others have suffered, like SES.

But the group did not sit idly by, even if the reaction took a long time to emerge. It has gone back on the offensive, in particular by deploying a new constellation of O3b satellites, and will benefit from a substantial windfall for having released Band C in the United States. Investors would like to know how to use this windfall, which may be the case at the end of February when the annual results are published.

The future income statement, precisely, does not necessarily give a fair view of the profit structure, since it includes the payments related to Band C. It should be noted that the turnover is rather stagnant because of the erosion video revenue and that the Ebitda margin should more or less be maintained. Not enough to dream of while debt remains structurally high (2.3 to 2.5 times EBITDA for the next two years). There remains the coupon, which the managers want to maintain at a generous level in an attempt to restore the image of SES: at least EUR 0.40, which represents a yield of nearly 5.7% on current prices.

“Fallait pas l’invite” identifies companies that are going through a complicated period on the stock market. You never know, they could recover! Latest articles in the section: