Snowflake is a cloud data management specialist. Its data analytics solutions have met with invaluable commercial success with customers who can aggregate, transfer, pool and order huge amounts of data on a multitude of different platforms without resorting to complicated APIs to set up or protocols. inevitably vulnerable exchange. The centralized data can thus be distributed to a multitude of actors who orbit around the center… a “snowflake” organization, which naturally inspired the company’s surname. The flexibility of the offer also allows third parties to join this ecosystem to develop and sell their own solutions on a large scale. There is therefore a platform effect which guarantees both the ubiquity of the solution and erects attractive barriers to entry. We also find Snowflake in the triumvirate of the global cloud, Amazon, Microsoft, Google.

A widely publicized IPO

The fairies leaned over the cradle of the company which will celebrate its tenth anniversary this year. In 2012, the head of the venture capital fund Mike Speiser went to get two French from Oracle, Benoît Dageville and Thierry Cruasnes, to create the company. There was also a lot of croaking on this subject around the IPO. And a few sharper comments pointing out that once again, it’s in Silicon Valley that French creators thrive. Among the fairies was Berkshire Hathaway, which invested from the IPO. Rather unusual as Berkshire traditionally never participates in IPOs. An investment certainly undertaken under the responsibility of one of Warren Buffet’s two lieutenants (Todd Combs or Ted Weschler) rather than Buffett himself. Perhaps they were seduced by the insane growth rates displayed by the company, a prerogative of several IPOs in the technology sector of this period.

It should not be forgotten that Snowflake was valued at $3.5 billion in 2018, then $12.4 billion at the start of 2020 and finally $33.3 billion based on the IPO price of USD 120. Suffice to say that the venture capital funds present in the capital carried out an excellent operation, certainly better than the shareholders who entered the file since, if we exclude the subscribers of the IPO or those who have since left in an appropriate timing. In this type of operation, it is always good to think about the motivations of sellers and buyers.

From 400 to 126 USD in six months

The sequel is much more chaotic, with two interludes beyond 400 USD a share. Since the last peak of last November, the action has continued to tumble until it hit a low point of 126 USD a few days ago, barely above the IPO price. The market cap’s three-fold halving in six months has led some bold analysts to compare Snowflake in 2022 to post-financial-crisis Google, when the tech giant with a monopoly on web search was trading at all-time lows. But with a major difference: ex-cash and ventures, Google quoted at 10 or 12 times its profits at the time, while Snowflake never brought in a penny in cash and traded at 20 times its income.

Since the IPO, the stock has fared worse than the S&P500 or a techno-aristocrat like Microsoft

The speculative dimension therefore remains very strong and any hasty comparison seems fanciful. You have to be right. Rather than Google, the most immediate comparison would be more with Amazon: IPO in 1997 at $18 per share, a price that jumped to $105 in two years during the dotcom bubble, then fell sharply to $6. It took an entire decade for Amazon’s stock price to rebound to all time highs. It is sometimes useful to remember that behind the success stories, there is not always a long calm river.

29 times 2029 profits

The management, however, communicates very ambitious projections: 10 billion dollars in turnover by 2029, i.e. an income multiplied by five in seven years, with a cash profit margin (free cash-flow) of 15%. Even relying on these management projections (necessarily optimistic), the return on investment expected by then is completely insufficient to consider such risk-taking. Especially if we take into account the inevitable dilution caused by the plethora of stock option payments, which represented $600 million last year, or half of the turnover expected this year. This tendency to overcompensate managers and employees is now a well-established practice in the technology sector.

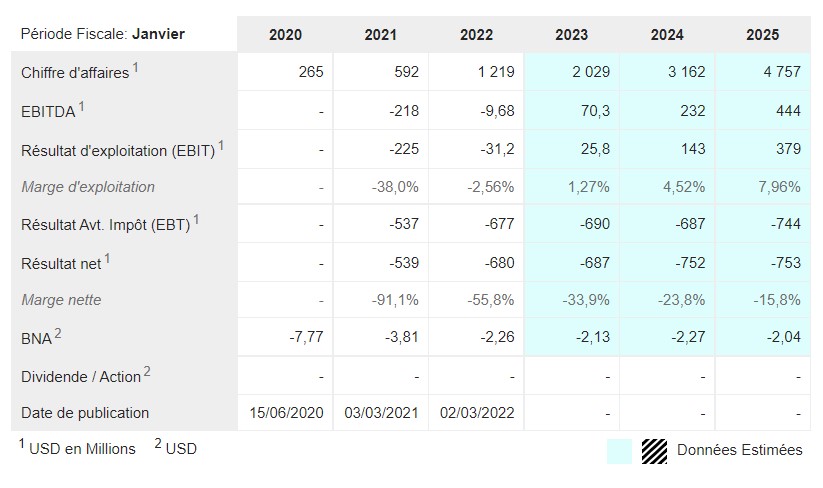

Estimates of expected results over the next few years (Zonebourse / S&P Capital IQ, 28 analysts on average)

Snowflake’s objective is to reach operational breakeven next year, before rolling out the plan to these famous 2029 objectives. But let’s assume that management’s projections are correct: cash profit should reach 1.5 billion $ in seven years, or a multiple of 29 times the results if we base ourselves on the current capitalization (in this diagram, note that we do not include the dilution resulting from stock options). On this basis, the valuation appears reasonable for a company experiencing very strong growth, if rates remain low. But since we are talking about the profit made in 2029, the file suddenly looks less sexy. It will be noted, it is already that, that the imposing reserves of the company should protect it from fundraising once the cash-burn is no longer negative.

In short, Snowflake retains an indisputable speculative character even after correction. Insiders also seem to think the same since CEO Frank Slootman sold $600 million worth of shares right at the peak of valuation, as did his financial director Michael Scarpelli, who sold him $241 million worth of shares. Actions speak louder than statements and for the moment, Snowflake will have especially enriched its first investors and its management.