If your income and the feasibility of your project remain sine qua non conditions for granting your credit, other information may or may not allow you to obtain your financing.

What does the bank really look at before granting you a real estate loan? If certain information requested does not change, more and more banking establishments are interested in your project in detail, in particular to the work envisaged in the event of purchasing a property with a poor DPE.

Income

Times are tough for borrowers. Because if real estate rates have gone from 1% to 4% in less than two years, salaries have not increased in the same proportions. Excluding, since January 2022, the debt rate, i.e. the share of the credit in relation to the borrower’s income is set at 35%. And inevitably, this rule has a strong impact on household financing.

In June, with a rate of 3.60%, a borrower earning 2,000 euros net per month could hope to obtain 136,000 euros. Two years earlier, in May 2021, the average rate was 1.35%. At the time, with the same criteria, the borrower could claim a little more than 174,000 euros. The banks themselves do not block files based on income, confirms Mal Bernier, spokesperson for Meilleurtaux. It is the debt ratio that blocks borrowers. So, credit production falls month after month. It showed a drop of 45% over one year in July, 12 billion euros.

Real estate loan: how much can you still borrow based on your salary?

The contribution

In June, according to data from Century 21, the personal contribution had increased by more than 60% between the first half of 2022 and the first half of 2023. It represented almost 35% of the purchase price, 89,000 euros for a property worth 257,497 euros. If the project is feasible with a 10% contribution, the bank will be able to follow, assures Mal Bernier. If the intake increases in recent months, this is because some borrowers are obliged to provide more to have a viable project.

Real estate loan: with the rise in rates, the personal contribution required is close to 90,000 euros

Residual savings

Residual savings are not strictly speaking a condition for obtaining a property loan. Savings are important in awarding a rate, not a credit. The more the borrower brings in contribution and residual savings, the lower the bank will grant a rate, assures Mal Bernier. Ideally, a borrower who arrives with 20% down and residual savings after the project will have the best rate.

According to the communications director of Meilleurtaux, the banks’ activity in recent months has also focused on this type of file. Having savings after the project would therefore be the sesame to benefit from a more attractive credit rate. A good will of the banks which is easily explained: the borrower will need banking products to invest this savings, which will save money for the establishment.

Real estate credit: residual savings, a new condition for obtaining a loan?

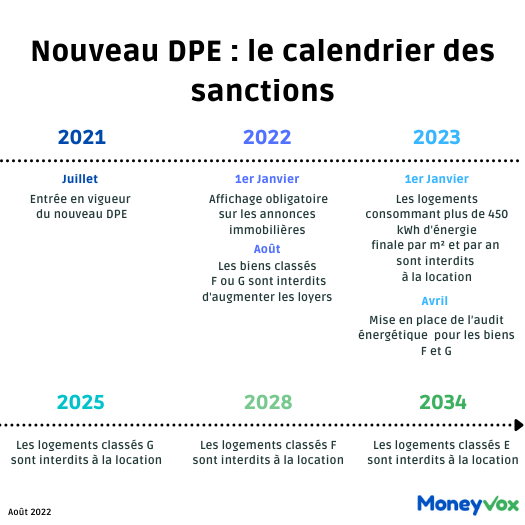

The DPE

This is undoubtedly the new thing, even if the DPE has been an important point for several months, notes Mal Bernier. Indeed, the Climate and Resilience law, promulgated on August 24, 2021, provides the ban on the rental from January 1, 2025 of class G housing and in 2028 of those class F by the new energy performance diagnosis (DPE).

If you are buying for a rental investment, this is a major subject because the bank will want to be sure that the property will be rented for the entire duration of the loan repayment, explains Mal Bernier. The bank will not finance a property classified G in the DPE without a price which is 20% below the market level or if the borrower does not come forward with a project which takes into account an envelope for renovation work.

If the bank will not necessarily block the project for the purchase of a main residence, a bad DPE will still be included in the calculation, a works envelope having to be planned. It’s an additional element which is part of the financing plan and what we are looking at, confirms Mal Bernier. You almost have to have made work estimates before going to the bank if you buy a thermal strainer.

Can the bank refuse me a loan because of a bad DPE?

And also…

Some things don’t change. When verifying your file, certain information may raise eyebrows at the bank. This is the case, for example, if you play a lot online (sports betting, poker, lotto, etc.) or if you tend to live beyond your means.

Real estate credit: these expenses that ruin your chances of getting a loan