HR

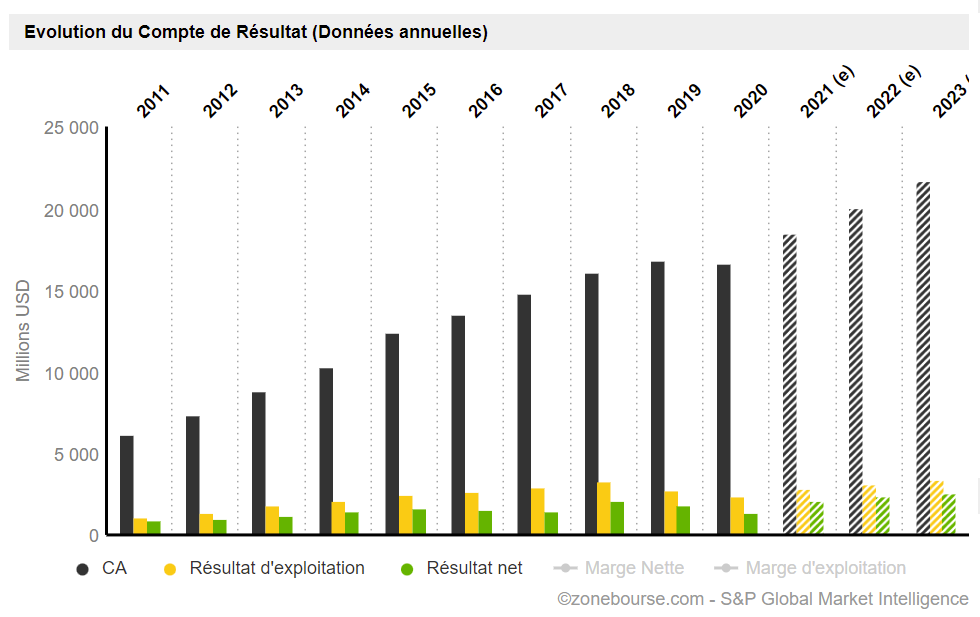

As well as being a position in Warren Buffett’s listed equity portfolio, RH can boast of being a 20-baggeuse stock since its IPO in 2012. In reality RH (formerly Restoration Hardware) has had a long history since its inception in 1979. It was first listed on the stock exchange in 1998 before exiting the public market in 2008. RH is an American high-end furniture company. The company has 94 furniture galleries and 36 factory outlets in the United States and Canada. The company obviously took advantage of the confinements of the health crisis but it would be reductive to grant it only this success. It has also been successful in its move upmarket to luxury to stand out from an Ikea as well as its digitalization, which represents an increasing channel of its activity. This luxurious positioning allows it to better withstand market fluctuations, because it is aimed at wealthy buyers less exposed to economic vagaries. The company achieves margins of around 10% for its net margin and 20% for its operating margin (they should increase in 2022). HR generates regular and growing free cash flow. The ROE and ROA are in great shape. The company is gradually reducing its debts and Capex represents 6% of its turnover. The stock has potential for 2022 to continue this good momentum.

Evolution of the HR income statement since 2012:

Source: Zonebourse

Cognizant Technology Solutions

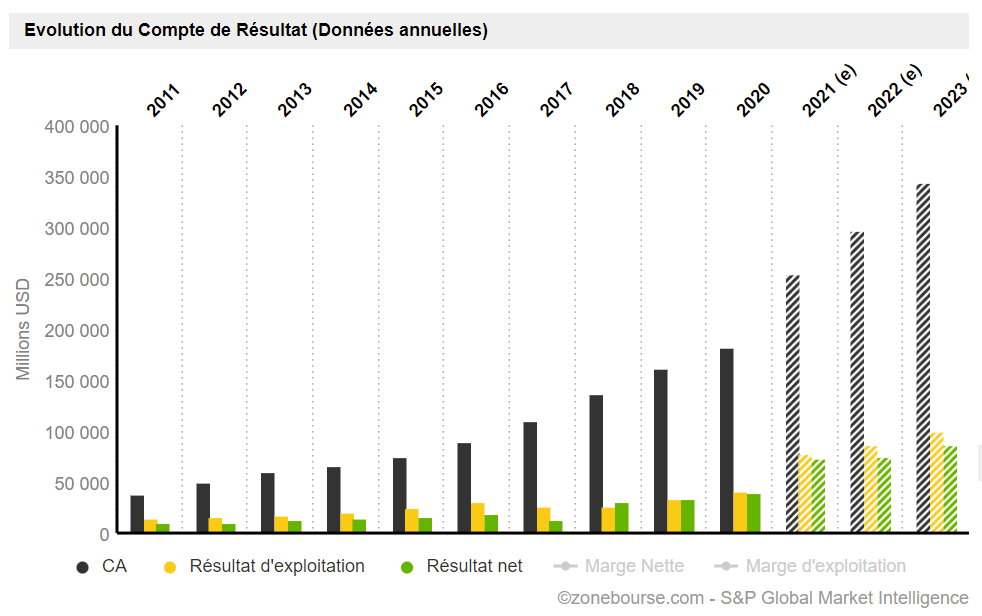

Cognizant Technologies Solutions is one of the leading IT service providers in North America and a leading specialist in IT outsourcing to India. It is one of the few technology and consulting companies to organize itself vertically around two priority sectors: financial services and health. The company is posting strong returns on capital, a policy initiated with the transition of the activist group Elliott to capital between 2016 and 2018. The return on equity should rise to 18.6% in 2021. Margins achieved in recent years quarters amount to 15% for operating margin and 11% for net margin. The company is in remarkable financial health with more cash than debt and positive and slightly growing free cash flow. In recent years, the company has been accelerating acquisitions to boost the group’s external growth, with some success. This is evidenced by the anthology of transactions over the past few months, including the $ 1.4 billion buyout of TQS Integration, a highly regarded consulting firm in the health industry since its clients are nine of the ten largest pharmaceutical majors. . The analysts who follow the group welcome this strategic reorientation for the moment. Revenue growth is expected to continue to increase by 8-11% per year for the next three years. Combined with a generous shareholder compensation policy through share buybacks and the payment of dividends, Cognizant seems to be buoyed by favorable winds for 2022.

Evolution of Cognizant Technologies Solutions income statement since 2012:

Source: Zonebourse

Alphabet

Alphabet, the parent company of Google, is the world’s leading advertising company. The company offers products and services that we all use on a daily basis (Chrome, Google Maps, Search, Google Play, Android, Youtube, Google Cloud, Google Ads, etc.). It is also in a monopoly situation since Google Search crushes the competition with more than 90% of the market share of developed Western countries. The company is at the crossroads of several major technological trends (artificial intelligence, digitization, internet of things, etc.). With a steady growth of 20% per year in turnover, the outlook remains good for the coming years and Alphabet could still deliver the best of itself in the coming years. The publication of results continues to surprise on the rise, the brand image of Google is rising in the rankings, and Youtube is gradually coming to compete with Spotify for music and Netflix for films. Alphabet’s bet presents some perceived risks, of course, particularly concerning antitrust and a possible dismantling. But in my opinion, this risk does not present a real risk for the shareholder who will see, in the event of Alphabet being split into several companies, see his positions revalued upwards (pure-players are better valued nowadays). A low-risk bet for 2022, resurgence of the epidemic or not.

Evolution of Alphabet’s income statement since 2012:

Source: Zonebourse

The author of this article is a shareholder of Alphabet.