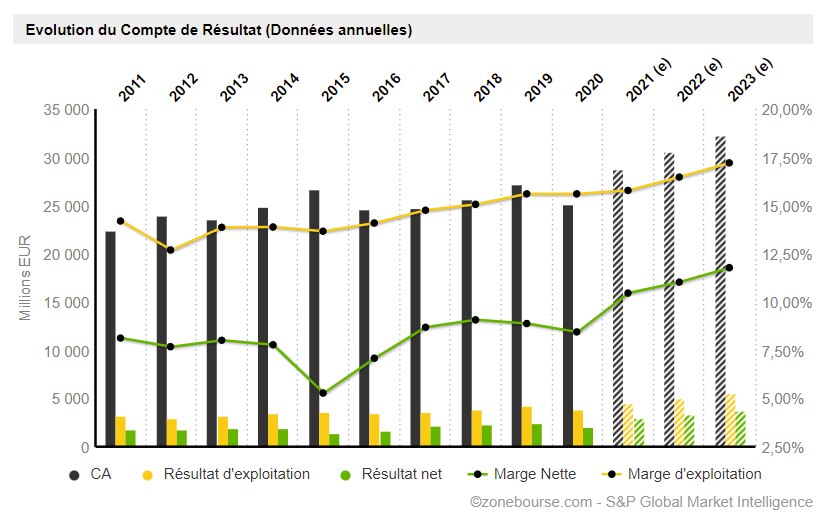

Infineon Technologies AG

Infineon Technologies, a former spin-off of Siemens AG, is a German semiconductor manufacturer and leader in the smart card market. The company offers a wide range of sensors, microcontrollers, integrated circuits, switches and other electronic components for the automotive industry (41% of its turnover), telecommunications infrastructure and consumer electronics (31 %), renewable energies (17%) and connected security systems (11%). The company has a good geographic diversity of its activity. Its direct competitors are Samsung, STMicroelectronics and NXP Semiconductor. Over time, the company has proven its ability to adapt, as a technology supplier, then a systems integrator and finally a solution provider. As proof, the average annual growth of its turnover since its creation in 1999 (what is called the historical CAGR) amounts to 10.6% against 5.8% for the semiconductor market. There are many growth levers for the group, particularly in the renewal of the vehicle fleet, with strong demand for electric vehicles and silicon carbide as the main growth engines. For example, electric vehicles carry an average of $ 950 of semiconductor equipment against $ 490 for a thermal vehicle and their market share is increasing sharply. Infineon has internally developed an MCU named AURIX Tricore, the best-in-class chip for real-time applications that will be essential to enable autonomous driving. After its small misadventures of recent months (closing factories in Malaysia, storms in Austin), 2022 should be a better harvest for the company, which has doubled its stocks to better respond to demand flows. In a favorable pricing environment, Infineon managed to deliver decent margins, in the order of 10.6% (net margins) in 2021, and is expected to increase to 13% next year. The company’s financial leverage is well under control (0.63 planned for 2022). Free cash flow is growing strongly (150 million euros in 2019, 718 in 2020, 1,568 in 2021) and the ROE should rise to 15.6% in 2022. A good value of semiconductors for next year.

Evolution of the income statement Infineon Technologies AG since 2012 :

Source: Zonebourse

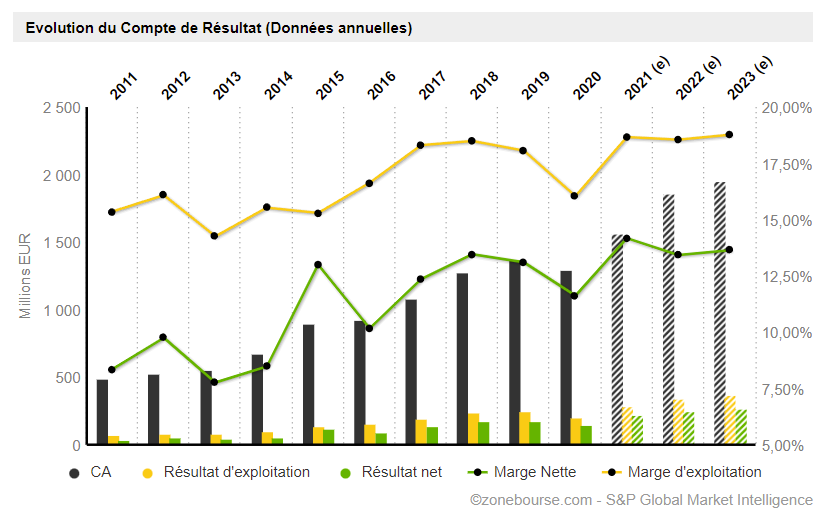

Schneider Electric SE

Present in more than 115 countries, Schneider Electric is the undisputed leader in electrical management – medium voltage, low voltage and secure energy, and automation systems. The ecosystem that Schneider has built allows it to collaborate on its open platform with a large community of partners, integrators and developers to offer its customers both control and operational efficiency in real time. The society supports its customers in the design of their production lines to improve their efficiency and environmental impact. For some time now, it has also been offering digital solutions for the design and control of automation systems in industry and the building sector. The group is also required to work on cooling systems for data centers. This French company (the only one in this 2022 European selection) has an exemplary stock market and operational history. The share achieved a market performance of 40% in 2021 and 337% over 10 years rolling. Free cash flow has experienced average annual growth of 16% over the past five years. Net profitability (expected at 11% in 2022) and operational (expected at 16.5% next year) live up to its reputation. The good visibility of the evolution of future activity as well as its remarkable diversification (both geographically and by activity) make it a choice stock for a portfolio fund. The icing on the cake, its ESG rating makes it eligible for SRI funds.

Evolution of Schneider Electric’s income statement since 2011:

Source: Zonebourse

Interpump Group SpA

Founded in 1977, Interpump is the world’s largest producer of piston pumps. The activity of the Italian group is divided into two poles, that of hydraulic pumps on the one hand (used to lift dumpers, concrete mixers, cranes), which represents 68% of turnover, the rest of sales being from the manufacture of high pressure pumps (used in high pressure washers, car washing systems, water desalination). Interpump has enjoyed a smooth stock market and operational performance, as evidenced by the stock’s progression, up 50% in 2021. Margins are good (expected in 2022 at 18.6% for the operating margin and 13.4% for the net margin). The debts are well controlled with a financial leverage of 1.24 times. Return on equity is expected to be around 17.4% next year. The value is carried by tailwinds. Italy benefits from the European “Next Generation EU” program of 750 billion euros and is already banking on improving its infrastructure. Interpump, as a construction actor, will benefit from this a fortiori.

Evolution of Interpump’s income statement since 2011:

Source: Zonebourse

These companies present “reasonable” valuations in view of the market context. They are admittedly slightly more expensive than the market average but these stocks are much more qualitative than the average for their respective sector. For example, Infineon Technologies pays itself four times its turnover and 30 times its future profits, Schneider Electric pays itself three times its 2022 turnover and 26 times its future profits and Interpump pays itself 3.5 times its 2022 turnover and 26 times its future profits.