24 months later, the Western population is deconfined and the COVID much less virulent. And the American delivery man is already put up for sale by its Dutch owner. Rumors point to offers approaching 1 billion dollars, seven times less than the purchase price. This fiasco is in the image of the sector, an eternal promise for a never profitable business.

One of the greatest challenges in the logistics industry is the management of “last mile delivery” (LMD), a concept that represents the delivery stage between the last logistics center and the end customer. This LMD accounts for 53% of the total cost of delivery of a product and induces significant constraints for carriers.

This LMD, with restaurants as the last logistics center, constitutes the bulk of the business of meal delivery services, which have still not succeeded in making this process profitable despite reduced labor costs (independent delivery people, uberization, etc.) , and low capital expenditure (cars/bicycles paid for by the delivery person).

The recent collapse in the valuations of meal delivery players prompts us to take stock of the four main players, who each have a different profile.

1.Uber

To Through its UberEats platform, Uber is the leader in meal delivery in the United States, where it generates between 50% and 60% of its turnover.

Its meal delivery segment has grown by leaps and bounds in recent years, growing from $600 million to $8 billion in just four years, surpassing Uber’s initial mobility business (transportation of people). However, this activity has never been profitable and burns between 400 M$ and 500 M$ per year.

Fortunately for Uber, its mobility activity generates an EBITDA of around $1.5 billion to $2 billion. The company can thus easily finance the growth of Uber Eats, which has obvious synergies with Uber, as the two services use the same platform.

Lately, its cash-hungry meal delivery business has drastically reduced its appetite for greenbacks, and UberEats looks set to break even. This significant progress deserves to be welcomed, and was only possible thanks to the diversification of activities.

On the stock market, Uber is currently valued at around $50 billion after a fall of almost 70% in its value since its all-time high in February 2012. The company is valued (EV) at 1.6x its turnover, a compression significant compared to its pre-covid valuation (4X to 5X).

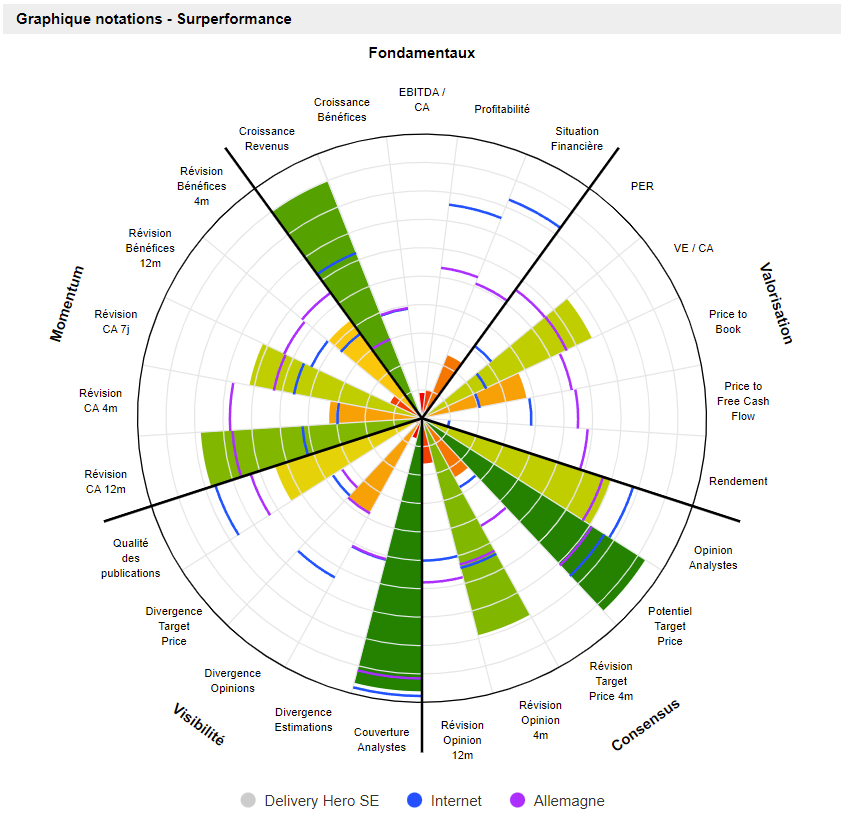

2.Delivery Hero

The German group, based in Berlin, has the particularity of achieving most of its turnover in Asia (45% in 2021). Its overall turnover has shown a crazy growth of 80% per year since 2017, climbing from €544 million to almost €6 billion.

Yet this growth is accompanied by an incredible ability to lose money, which is not going away, with a negative free cash flow of more than a billion dollars for the 2021 financial year.

The group therefore relies heavily on the ability of its investors to inject cash, both to finance operations and the expansion of the company (€1.3 billion acquisition in 2021). Prosus, its main shareholder with 27% of the shares, brings a certain assurance to Delivery Hero due to its size and solidity, necessary assurance for a company that is totally dependent on the capital markets. Delivery Hero is also the subject of recurring purchases from insiders.

The company is valued at just under €8 billion and the stock is sailing at almost 80% of its highs. The enterprise value stands at just over 1x sales for 2022, but the company has a very pronounced speculative character, with sessions with at least 5% variation almost daily.

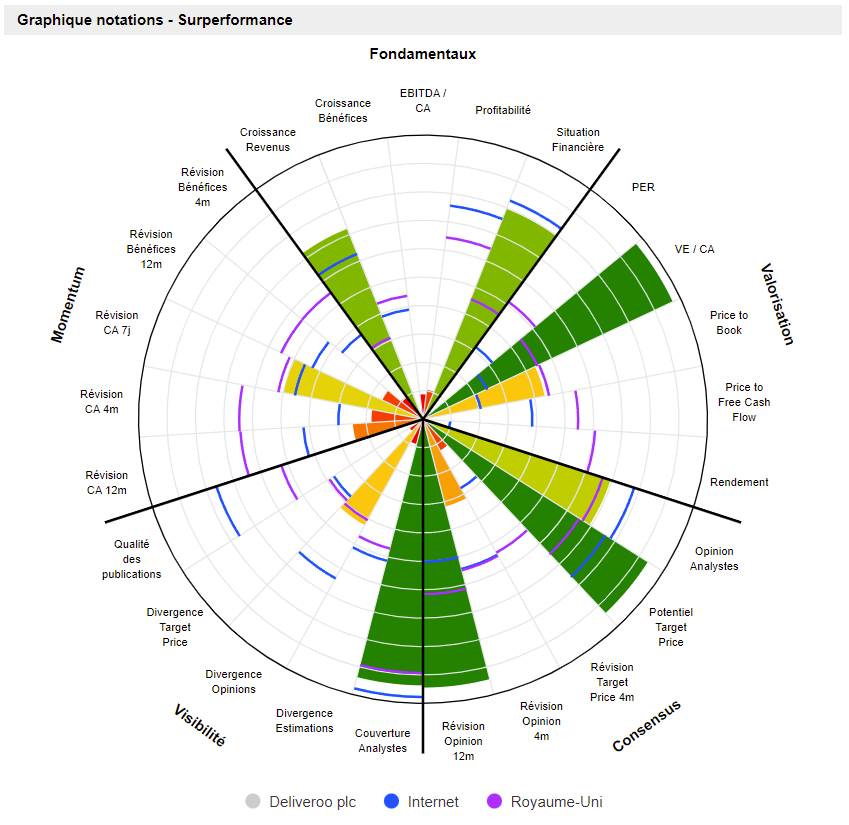

3.Deliveroo

The British delivery company Deliveroo, well known to the French public, has also experienced very sustained growth with sales rising from £300m to £1.8bn in just four years (average annual growth of 55%). Its particularity compared to competitors is its less megalomaniac trait characterized by a more controlled development, without acquisitions but with a focus on organic growth. Deliveroo generates more than half of its turnover in Great Britain.

As a player in the delivery of meals, Deliveroo is not immune to the loss of cash which amounts to around £200 million per year, but which follows the initial business model and seems to be under control, unlike its German competitor. If the company continues at this pace, the cash reserves of £800m will allow it to last another three or four years.

Deliveroo presents a picture that is certainly healthier than its peers mentioned above, but there is no reason to expect profitability, apart from a rise in the prices of its platform which risks putting off a slew of customers.

The enterprise value is currently established at 0.3X the turnover, the most attractive valuation of the four companies mentioned in this article. The action has lost nearly 80% of its value since its peak and regularly performs sessions with pronounced variations.

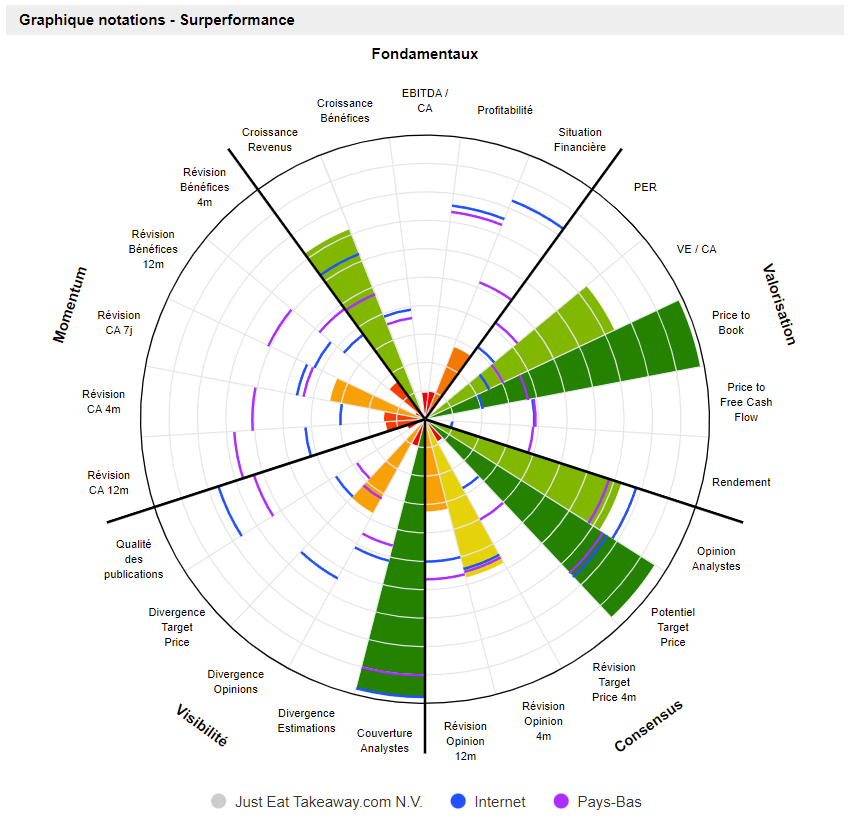

4. Just Eat Takeaway

The Dutch, resulting from the $8 billion merger in 2020 between the British Just Eat and the Dutch Takeaway.com, shows the most insolent growth of this selection, with an average annual growth of 134% for four years, bringing the turnover from €150 million to €4.5 billion.

As for his friends, the company is not profitable and burns nearly 600 M€ in 2021, a figure which is not improving with the growth in sales. The company no longer has cash to ensure its operation and is forced to sell off its assets to ensure its survival, including Grubhub, which could sell for seven times less than its acquisition price of $7.3 billion in 2020.

This file illustrates the destruction of value suffered by the sector and in particular Just Eat, which finds itself in an impasse and could only count on an acquisition or a merger to ensure a future. Nevertheless, we do not see Delivery Hero adding a new cash-consuming abyss, a merger with Deliveroo would not fit into the English strategy, and a merger with the American Uber would be very surprising.

Just Eat Takeaway displays an enterprise value equivalent to 0.9 times the turnover, illustrating the still present hopes of a takeover in the minds of investors. Unfortunately, the company seems to be going straight into the wall, and a buyback is bound to take place at a level far from the previous highs.

Conclusion :

The trajectories of the main meal delivery players are a reflection of their immature sector, which is struggling to find the keys to opening the doors to profitability. Every society has an advantage on which it can hope to capitalize. Whether it is Uber with its diversification which allows the financing of its delivery activity, Delivery Hero with its huge Asian market and its reference shareholder, or even Deliveroo and its sound management. Only Just Eat appears to be the bad student and its prospects are particularly nebulous.

Meal delivery remains a highly speculative segment, with no real long-term vision and with a strong legislative risk because of the status of independent deliverers, who may be requalified as employees, as is already the case for Uber in Switzerland.

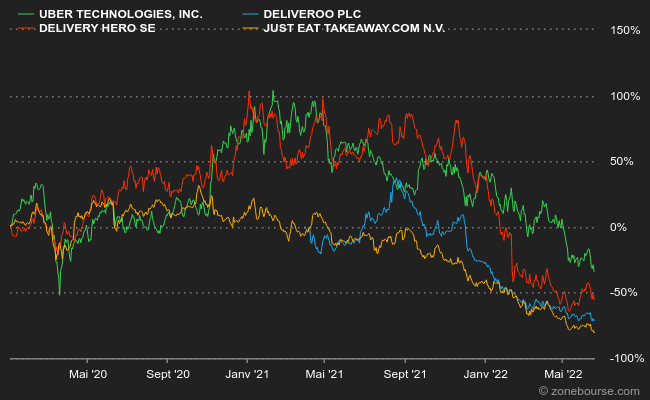

Stock market history of meal delivery players since January 1, 2020.