Payment via mobile platform is certainly practical, but involves some risks. The European Consumer Center warns against fraud and gives some advice on how to avoid it.

It is now a habit for millions of users who have partly given up on their bank card: the smartphone or the connected watch have become means of payment in their own right. It must be said that the proliferation of platforms (Google Wallet, Apple Pay, Samsung Pay, Garmin Pay, etc.), their support by almost all banking organizations and above all the ease of use explain this success.

However, like any means of payment, the latter is not without risk and this is what the European Consumer Center (CEC) of France recalls via a press release.

Mobile payment is not immune to fraud

The first element put forward by the CEC press release concerns the fact that contactless payment via a smartphone or a connected watch is not subject to a cap, unlike the classic bank card. In general, authentication via PIN code, fingerprint or facial recognition is sufficient to open an account for any purchase, even a large one. Some banks still require additional authentication via the application in the event of payment in excess of 200 euros.

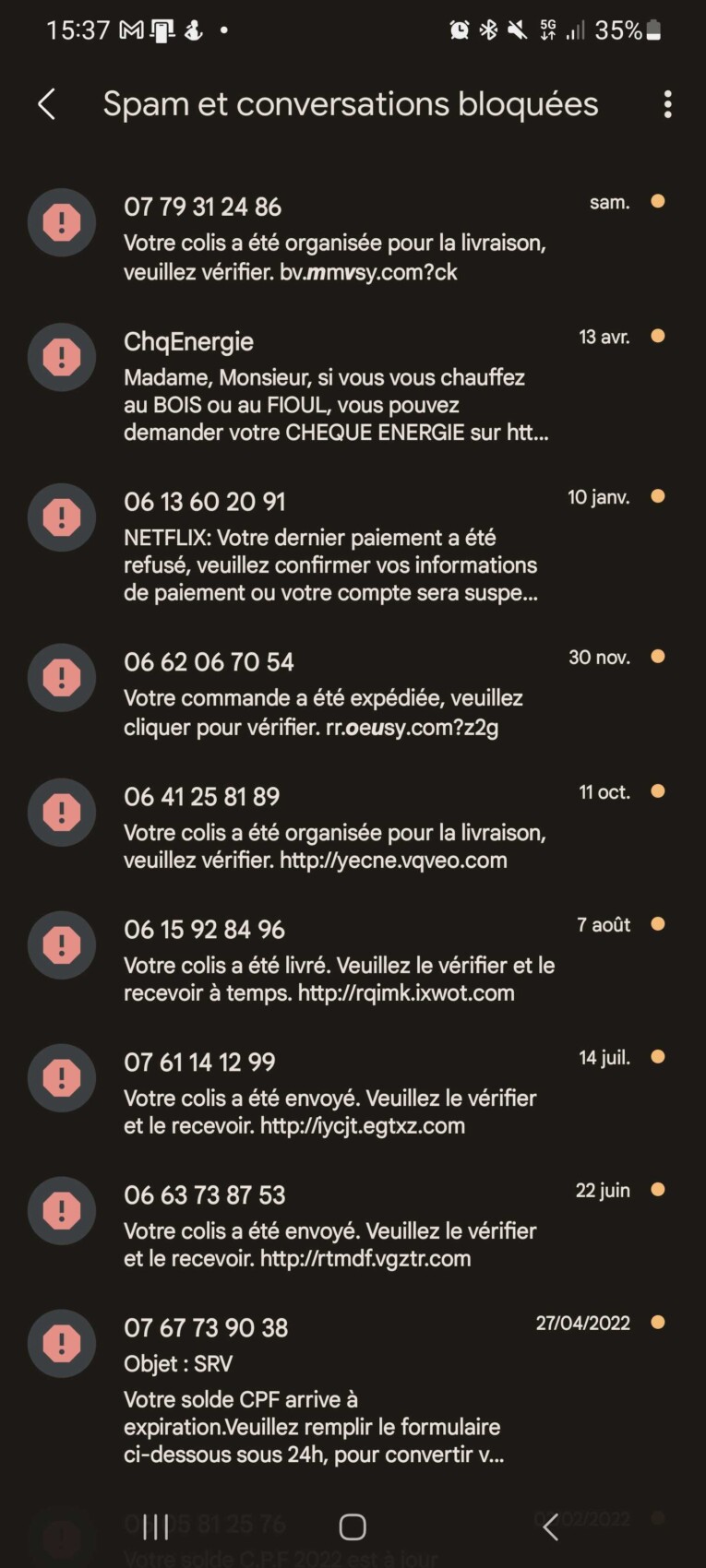

This does not in any way prevent fraud. The CEC states that it has received numerous complaints from victims of “ spoofing » (identity theft) and «smishing(SMS phishing).

In most cases, fraud occurs when the victim agrees to give their credit card numbers following a message received by email or SMS referring to a form site inviting them to share their Apple or Google identifiers to resolve a billing problem, delivery or loss of bank identifier. If the victim has previously accepted the coupling of his bank card to a mobile payment service, fraudsters can pay large sums with their smartphone.

What to do in case of fraud?

The first thing to do in the event of fraud (or even suspicion of fraud) is to block your card directly with your bank. Banking applications generally allow this operation to be carried out very simply, whether temporarily or permanently. However, the organization points out that in the event of fraud, this operation is not always 100% secure and that you will have to contact the payment service in question (Apple Pay, Google Pay, etc.) to delete your bank card. associated.

Whatever the amount stolen, you can request a refund from your bank in the form ofchargeback.You will also be able to dispute fraudulent debits and request reimbursement in writing from your bank within a maximum period of 13 months (or 70 days for a fraudulent payment outside the European Economic Area).

CEC Manager Bianca Schulz recommends:

Keep as much evidence as possible to prove your good faith and contest your negligence. This is an argument often put forward by payment providers to refuse to reimburse fraudulent transactions denounced by a customer.

Here is the substance of the advice provided by the CEC to strengthen the security of its mobile payments:

- Lock the payment application with a password or separate identification method from that of your phone.

- Always check battery life your phone and especially your connected watch if you use it as the only means of payment.

- Note the your bank card numbers and your bank’s customer service number away from your phone.

Do you use Google News (News in France)? You can follow your favorite media. Follow Frandroid on Google News (and Numerama).