Saturday, August 7th, 2021

Better days? When?

Commerzbank leaves many questions unanswered

From Stefan Schaaf

Commerzbank’s numbers are deep red. In order to be back on par with large European financial institutions, it will take a lot of effort, says CEO Knof, who has been in office since the beginning of the year. He tries to take it sporty. But adversity is not only looming in Poland.

Manfred Knof has to feel a little like a coach who has taken over a stumbling traditional club in the second Bundesliga. It should quickly go up again, to where you naturally locate yourself. Just as the fans of HSV, Schalke 04 or Werder Bremen always look upwards and, if in doubt, “to Europe”, Commerzbank wants to be able to play on the same level as major European banks.

But the way there is long and arduous, so that Commerzbank CEO Knof, who has been in office since the beginning of the year, communicates like a new trainer: clearing up the burdens of the past, rebuilding the “club”, being patient and still drawing a bright future. “We are sticking to our earnings forecast,” he emphasized on Wednesday during a conference call for journalists. For the year as a whole, they should be “slightly above those of the 2020 financial year”, when Commerzbank posted income of around 8.2 billion euros.

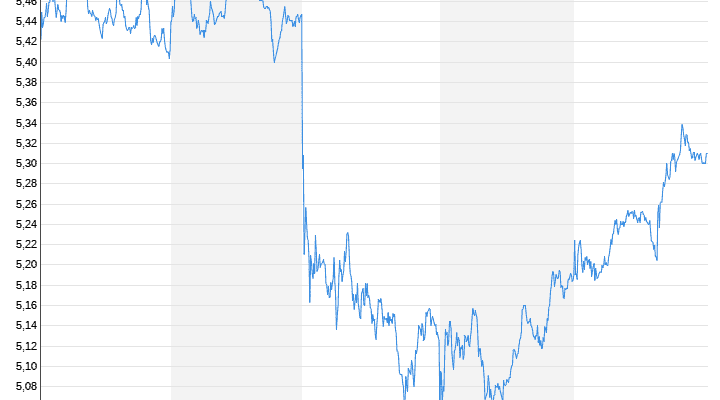

The figures now published by Commerzbank for the second quarter show, on the one hand, that the institute is still busy with clean-up work. But there are also disappointments beyond that. No wonder, then, that the already badly running share temporarily slipped around five percent on Wednesday and fell more or less to the level at the beginning of the year at around 5.20 euros. With the hoped-for resurgence from the MDax to the first division, i.e. the Dax, it will not work.

First to the figures: Commerzbank is communicating an operating result of 570 million euros for the first half of the year, of which 32 million euros (previous year: 205 million euros) were generated in the second quarter. That sounds good at first, but the reality of the second quarter looks bleak. There is a net loss of 527 million euros, while the institute earned 183 million euros in the same quarter of the previous year – and thus even at the economic height of the Corona crisis. The quarterly loss is due to many one-time and restructuring effects, more on that below. However, the loss is also higher than the analyst consensus expected – and they knew about the ongoing restructuring.

The market had only assumed a minus of 504 million euros. From a market perspective, the real disappointment in the quarterly figures is that earnings remained below expectations and costs above expectations, both effects that have nothing to do with restructuring or one-off effects.

However, one must also allow the Commerzbank management under Knof that they have to tackle the messy clean-up work at the credit institute that overestimated its possibilities for a long time and tried again and again to play on an equal footing with Deutsche Bank. The second quarter did better with the larger competitor. The bottom line was that the Frankfurt-based company generated a profit of 692 million euros from April to June, after a loss of 77 million euros a year ago. It was Deutsche Bank’s fourth quarterly profit in a row.

Commerzbank is also promising better times again. “In 2022 we should clearly see the fruits of the transformation process,” promised CFO Bettina Orlopp. She did not want to commit to a profit forecast for the current year. “It wobbles around the zero line, she said. Orlopp makes sure that things are going quite well operationally from the fact that the company’s net interest income is stable and the second main source of income, namely the commission income, is pointing upwards.

In Poland there is a threat of hardship for Commerzbank

The reluctance is likely to be related to the date of September 2nd. Then the Supreme Court in Poland will decide how to deal with Swiss franc loans from the noughties. As in other Eastern European countries, banks there had issued mortgages in Swiss francs with low interest rates. The speculation did not work because the franc appreciated significantly in the course of the financial crisis and borrowers had to repay significantly more in local currency. What is actually a market economy disturbs the national populist government in Poland. If the court forces the banks to compensate, the Commerzbank subsidiary there, mBank, will also be charged.

The parent company from Frankfurt posted a charge of 55 million euros in the second quarter, 300 million euros had previously been set aside. Apparently there are other risks. In the presentation on the quarterly figures it says: “The outlook is based on the assumption that there will be no substantial changes in relation to the loan portfolio of mBank in Swiss francs.”

The judgment of the Federal Court of Justice on account fees in Germany hit the office with 66 million euros more. Here, Commerzbank, like other banks, is currently in the process of legalizing the increased account fees, i.e. obtaining the consent of its customers.

And then there are the burdens from the cum-ex scandal after the Federal Ministry of Finance recently announced a stricter tax review of the issue. However, Commerzbank did not quantify the exact charges; they are hidden in a general item.

The largest single chunk of special charges in the second quarter, however, was a depreciation of 200 million euros on the project, outsource securities processing to HSBC. As early as July 22nd, the bank cited “technical implementation risks and changed market conditions” as the reason for this. Numerous questions about who is responsible for the expensive failure of the project, which started in 2017, remained unanswered during the conference call.

The big strategic questions at Commerzbank are still unanswered: How are the two major shareholders, the Bund and Cerberus, behaving, of which – unlike a year ago – there is currently no public hearing. And the core question: Will Commerzbank manage to remain independent after its current transformation or will it – possibly in a political deal – become part of a major cross-border European bank.

.