Institutional hedges. The AI narrative seems to be slowing down, liquidity is tightening, Russia was worrying all last weekend and regional banks are not at the end of their troubles. Today, let’s take advantage of the general calm of the markets to recap the various events.

The Fed changes its tune

About ten days ago, the famous FOMC took place, an event during which the FED talks about monetary policy. She chose not to raise rates, as you probably know.

Prior to this FOMC, we had discussed the probabilities of the July rise. At the time of the article’s release (June 8), market participants estimated the likelihood of a July rate hike at 50.7%.

Now, the odds have changed, and market participants estimate a 77% chance that the Fed will raise rates in July.

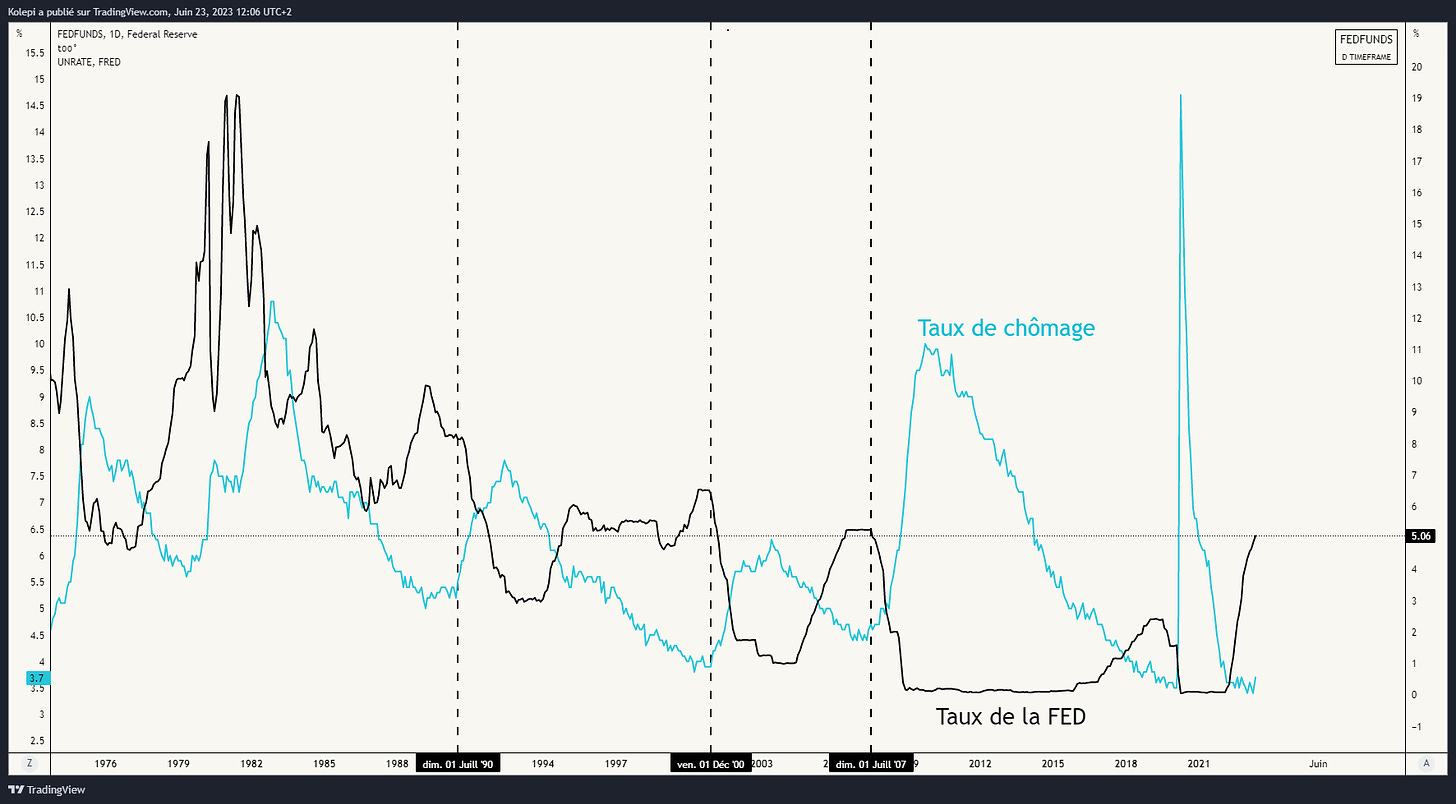

We can see the historical graph below.

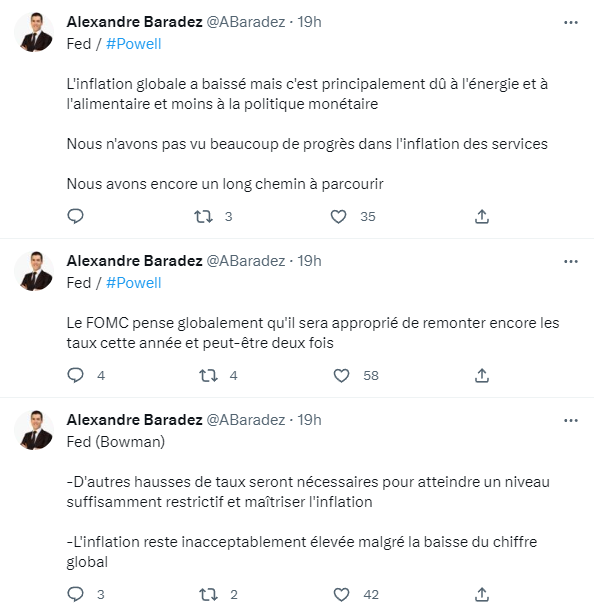

The FED has been particularly “hawkish” during its last meetings. Thanks to Alexandre Baradez (whom I invite you to follow on twitter), we have an overview of the latest speeches from the FED.

The FED wants to continue its fight against inflation, but will she actually do it? We saw in a previous article that it will probably have to make concessions, for two reasons:

- If the currency loses value, the debt is lighter : If you have a fixed debt with a nominal amount to be repaid, inflation reduces the real value of this debt over time. As a result, the actual debt repayment burden is reduced.

- Returning to the two percent target would be too costly economically : If the FED really wants to bring inflation back to 2%, the cost to the economy will be too high, as wewe saw at the beginning of the year.

The cost of lowering inflation to the two percent target would be an unemployment rate of 6.4%. If that were to happen, it would happen ahead of the US presidential elections. Bad press for Joe Biden, who intends to run again.

I think the Fed will keep rates high until:

- Unemployment rises drastically : Historically, the Fed has pivoted when unemployment becomes too high.

Or

- A “Credit event” is coming : Credit events are much more difficult to predict. Regional banks are extremely exposed to commercial real estate, which is currently in a difficult position. But there can be many other causes of a credit event.

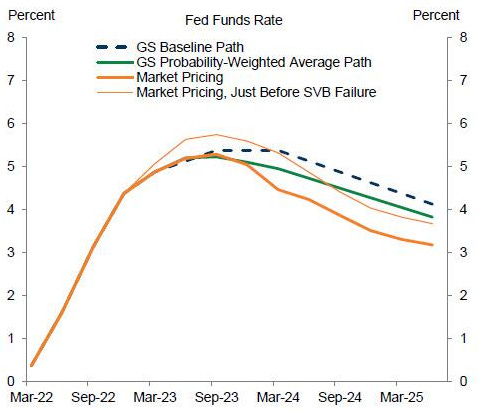

The problem here is that market participants have been pricing in a faster rate cut than Goldman Sachs expects. When the market understands that the FED is not going to lower its rates immediately, it will probably weigh on the price of risky assets.

Institutionals cover themselves

There are several reasons why market participants are currently looking to hedge:

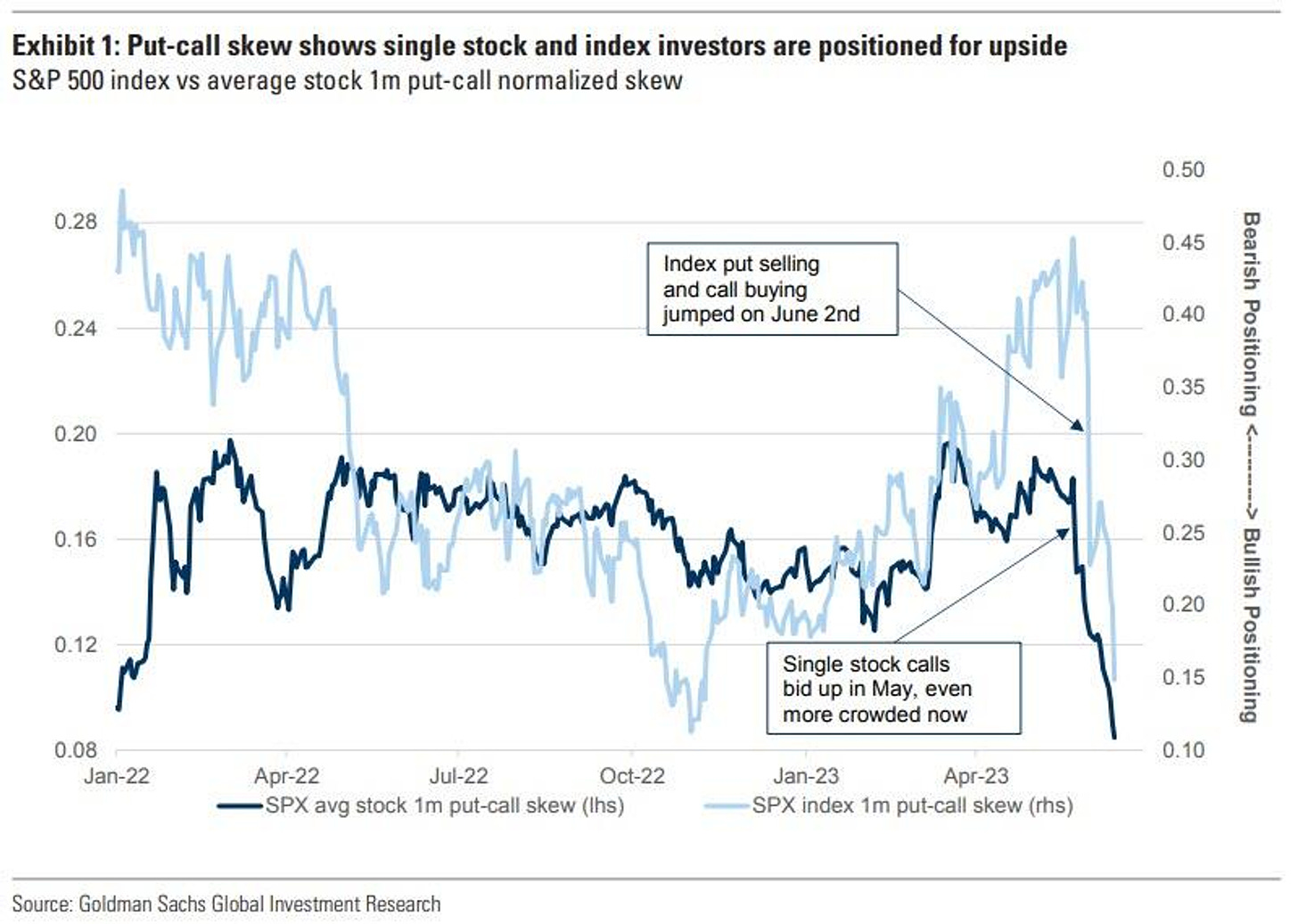

The asymmetry between put options and call options

Sale options (put) allow you to protect yourself against a fall in prices, call options (call) allow you to profit from a rise in prices. When the skew is skewed in favor of the call options, it indicates that investors are primarily interested in potential gains on the upside and are less worried about a downside.

Spin

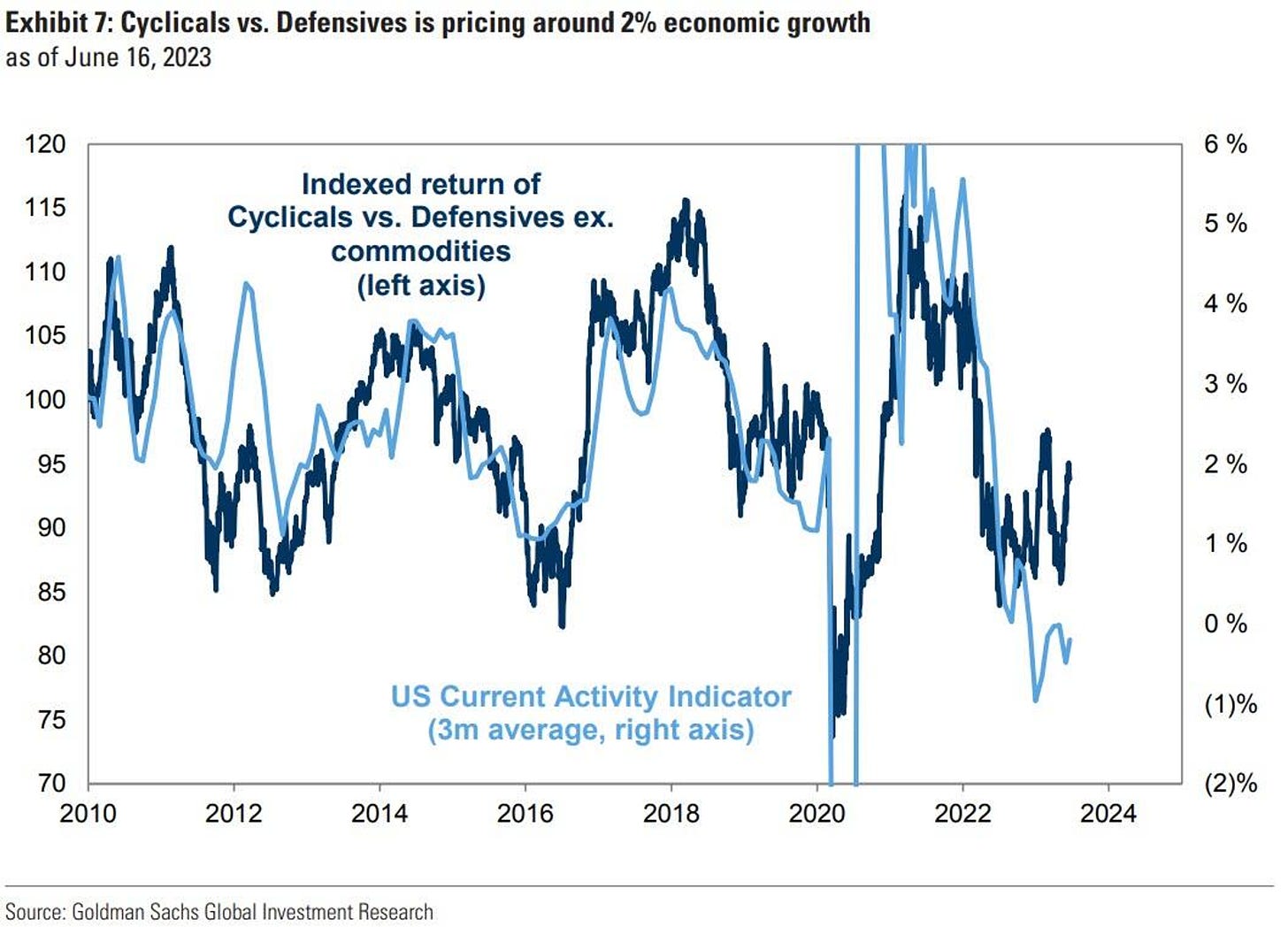

The graph “Index Return of Cyclicals vs. Defensive eg. Commodities” compares the returns of an index representing cyclical stocks versus defensive stocks, excluding stocks related to commodities.

Cyclical stocks are generally those whose performance is closely linked to economic health and growth, such as industrials, technology, automotive, etc.

Defensive stocks, on the other hand, are seen as more stable and less sensitive to economic cycles, such as the utilities, consumer staples, healthcare sectors…

The US Current Activity Indicator measures the current level of economic activity in the United States. This indicator is based on various economic data: industrial production, retail sales, employment, consumer spending, etc.

The chart “Indexed Return of Cyclicals vs. Defensive eg. commodities” has been climbing since the beginning of 2023, meaning that players are exposed to cyclical stocks.

These graphs have always been very correlated: when the economy is doing well (current activity indicator), they are exposed to cyclical stocks, which are the ones that will perform best, when the economy is in difficulty, they fall back on stocks defensive.

Why such a decorrelation?

In my opinion, it is a mixture of several things. On the one hand, exacerbated pessimism at the end of 2022, beginning of 2023, causing many players to position themselves short (short selling).

Second, an AI narrative and a force of actions that are linked to this impressive narrative.

Third, FOMO which is exacerbated by closing short positions.

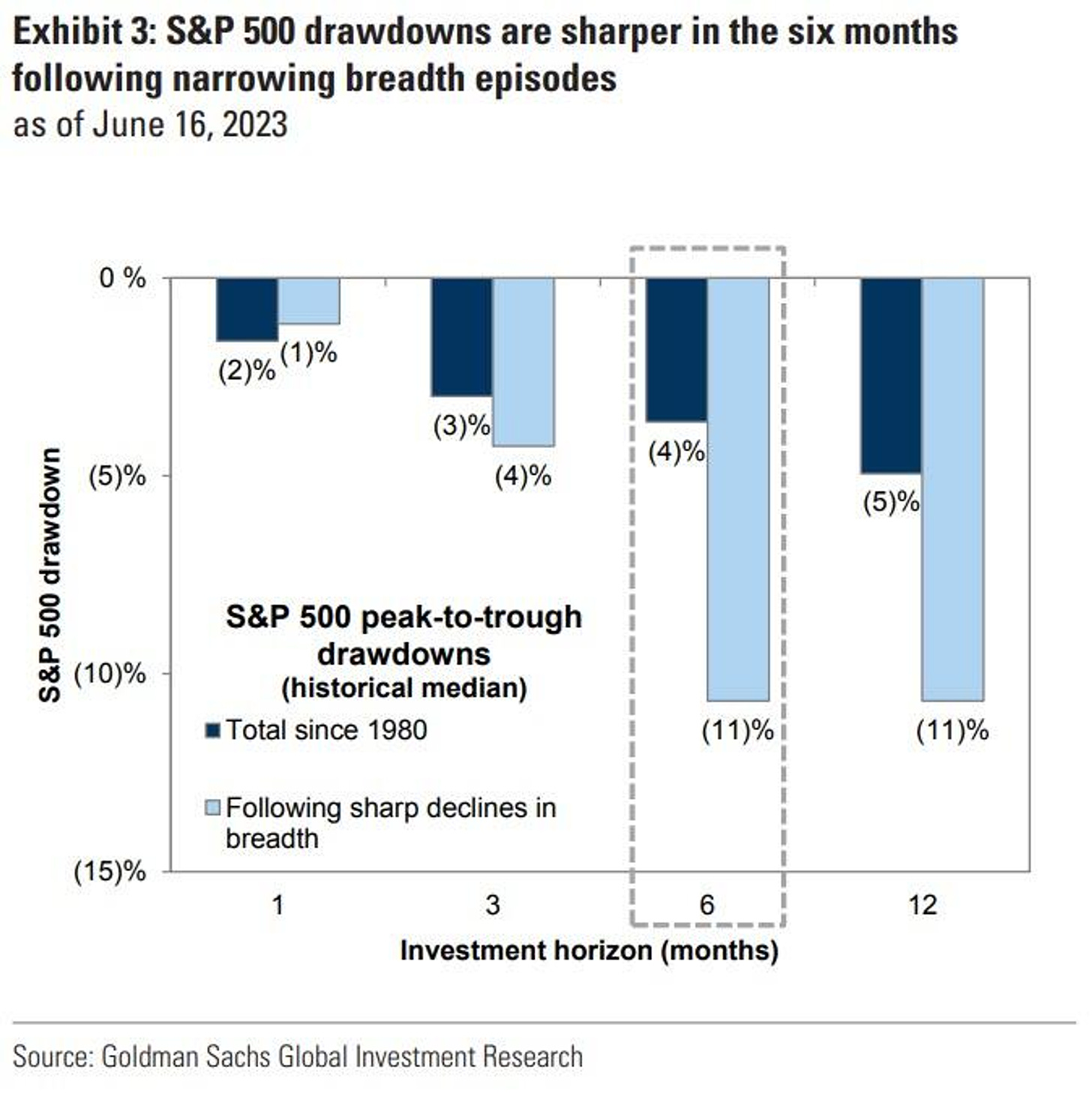

Below we see the median performance of the SPX from peak to trough, total AND after a drop in amplitude.

On average, the drops in the SPX that followed a drop in the amplitude were more violent, especially in a horizon of 6 to 12 months. Which seems logical: the risk is concentrated on a handful of stocks, in this case stocks related to AI.

Liquidity is king

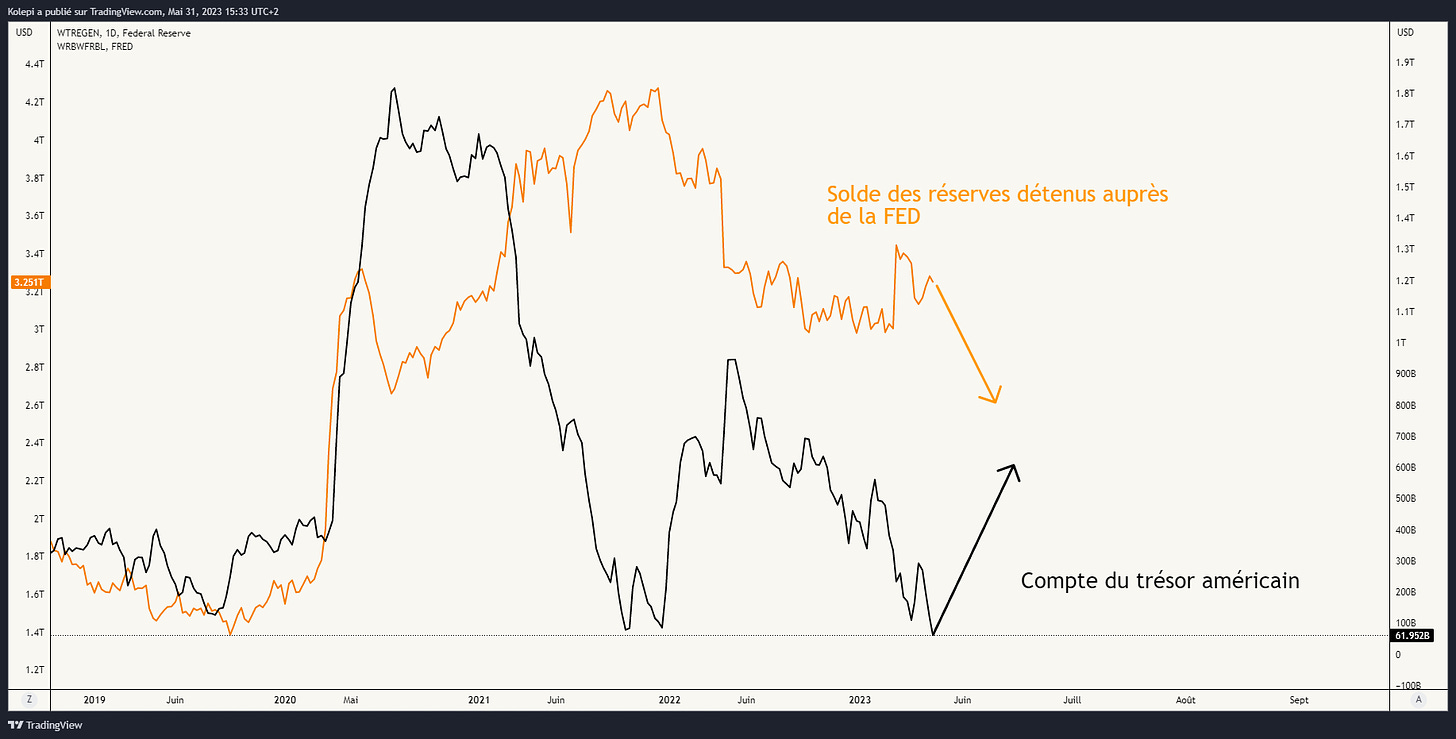

“Raising the debt ceiling prevents the US from going bankrupt, but it also implies that the US will have to issue new bonds to reconstitute a bedrock of “safety” in the US Treasury account. To buy these bonds, the commercial banks will withdraw liquidity placed with the reserves of the FED, and if the yield increases all the same, it will exacerbate the interest of the American citizens towards the monetary funds, further weakening the banks.

How will the debt ceiling agreement lead to the next banking crisis?

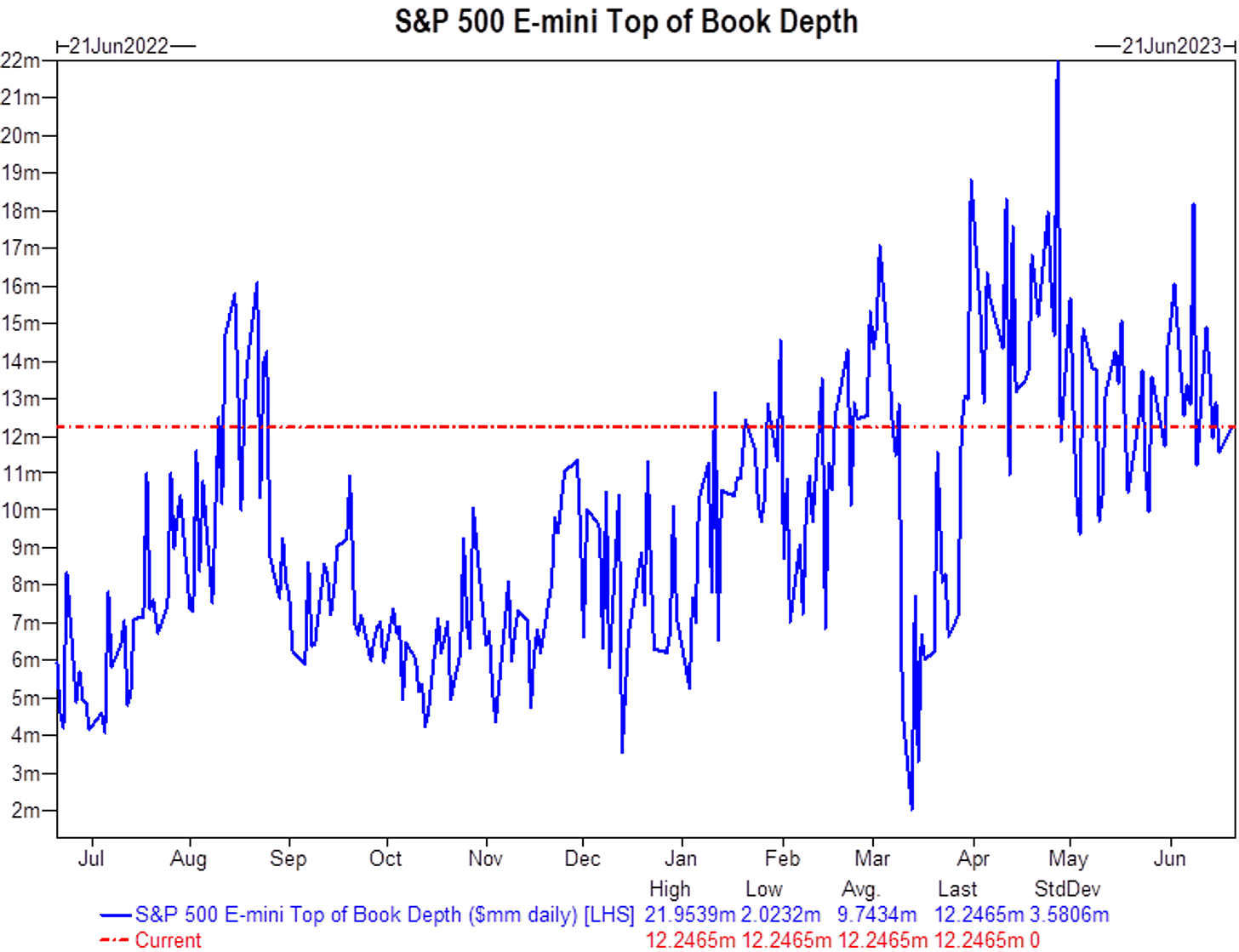

After the BTFP (Bank Funding Term Program), having been created by the FED in response to the failure of several banks, the depth of the market has clearly increased, we see it on the following chart representing the depth of the SPX orderbook.

It has started to contract in recent weeks, as US central bank bond issues are used to replenish the US Treasury account.

If you enjoyed this article, feel free to share, like, and subscribe to The Macronomist.

A very different feeling

Several surveys indicate that investors are much more optimistic recently. Let’s go back in order:

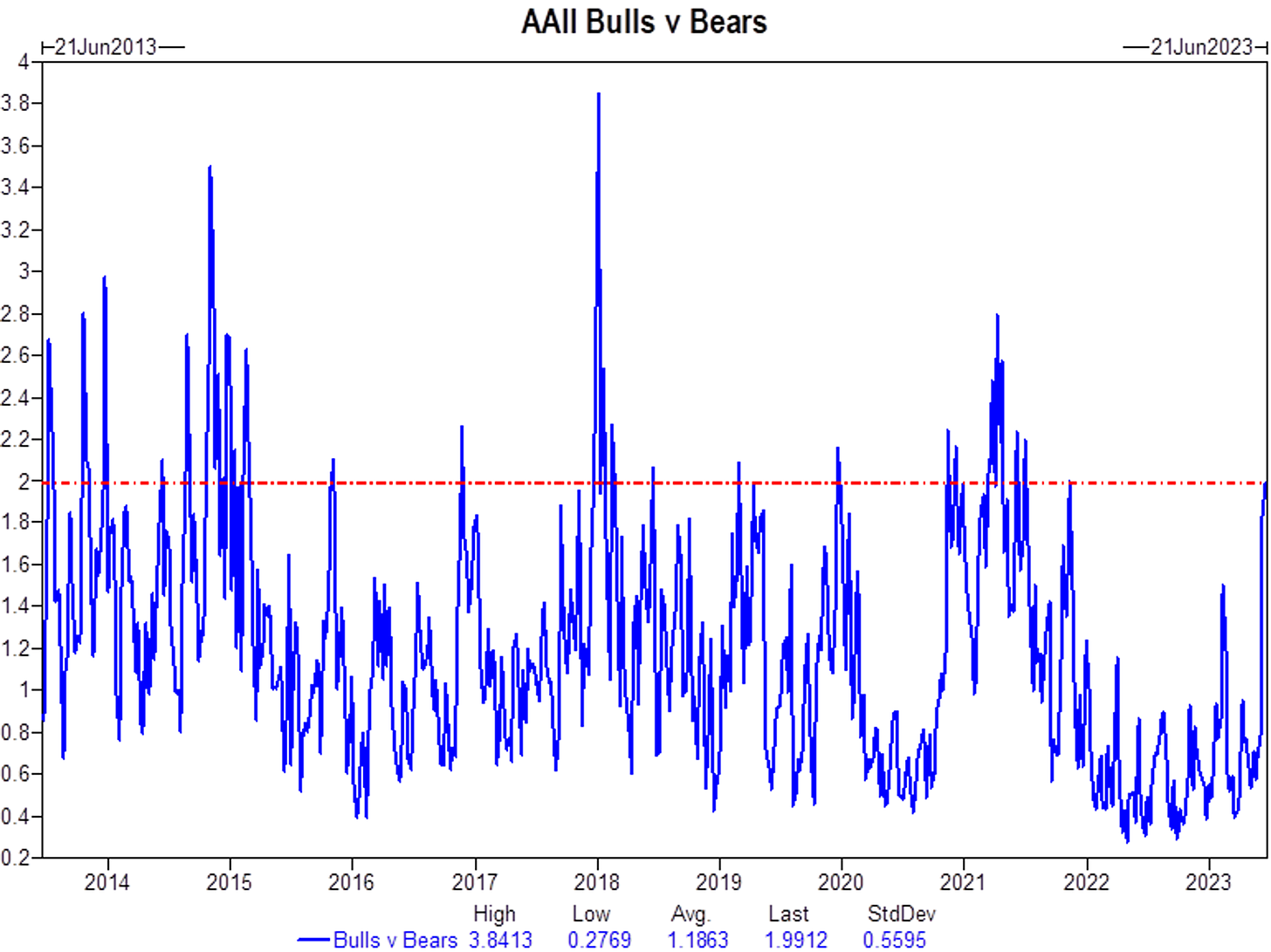

The American Association of Individual Investors survey is based on responses from a sample of individual investors to a weekly survey. Respondents are asked to give their opinion on the markets, either bullish, bearish or neutral.

US retail investors haven’t been so optimistic since the end of 2021.

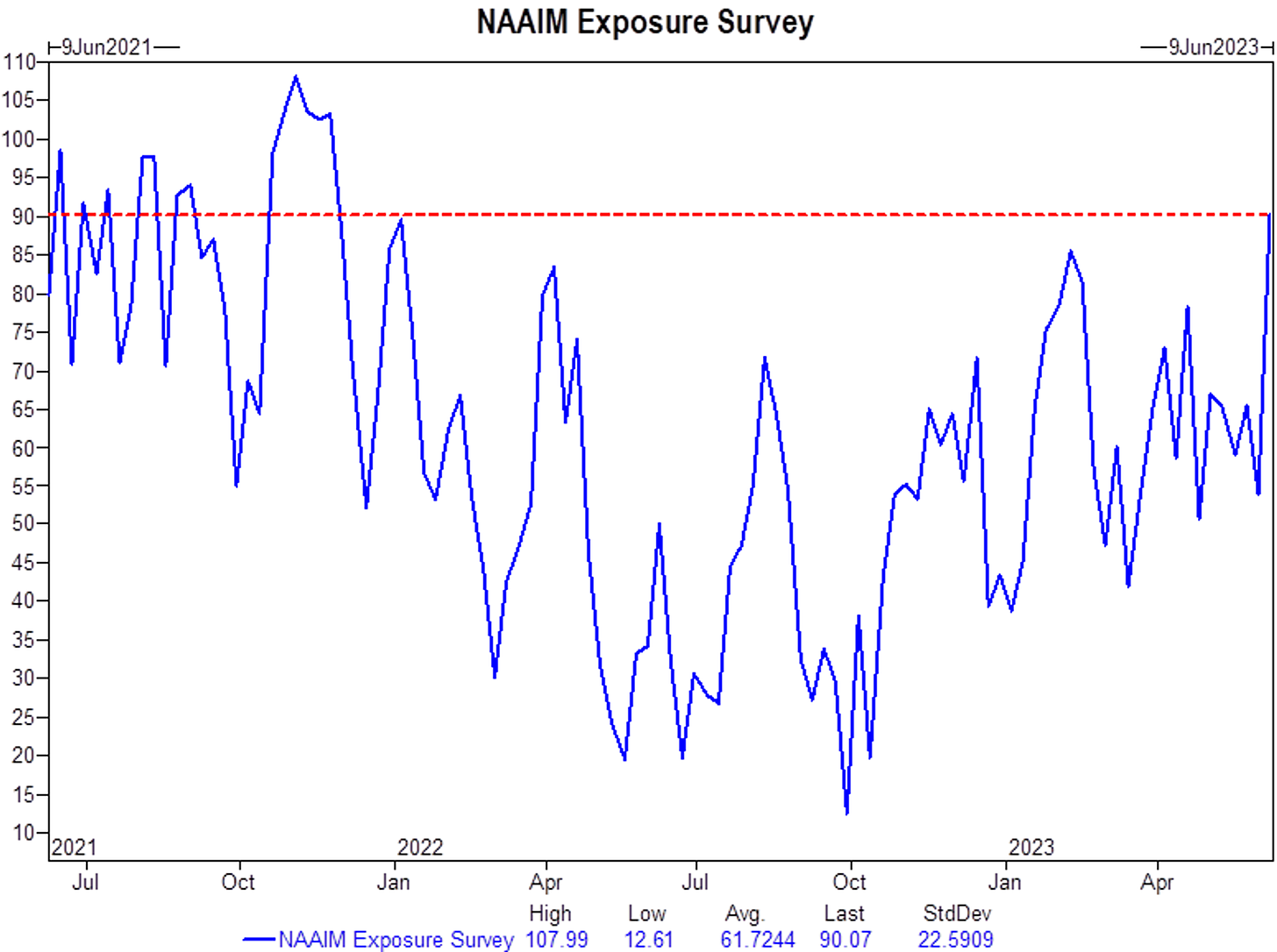

Second survey, that of the National Association of Active Investment Managers. These are no longer individual investors, but asset managers.

This survey asks members of the association to provide information on their positions and feelings.

The latter have not been so optimistic since the end of 2021. This very pronounced acceleration over the past few weeks leads me to believe that this is a FOMO (Fear of Missing Out, the fear of missing a occasion).

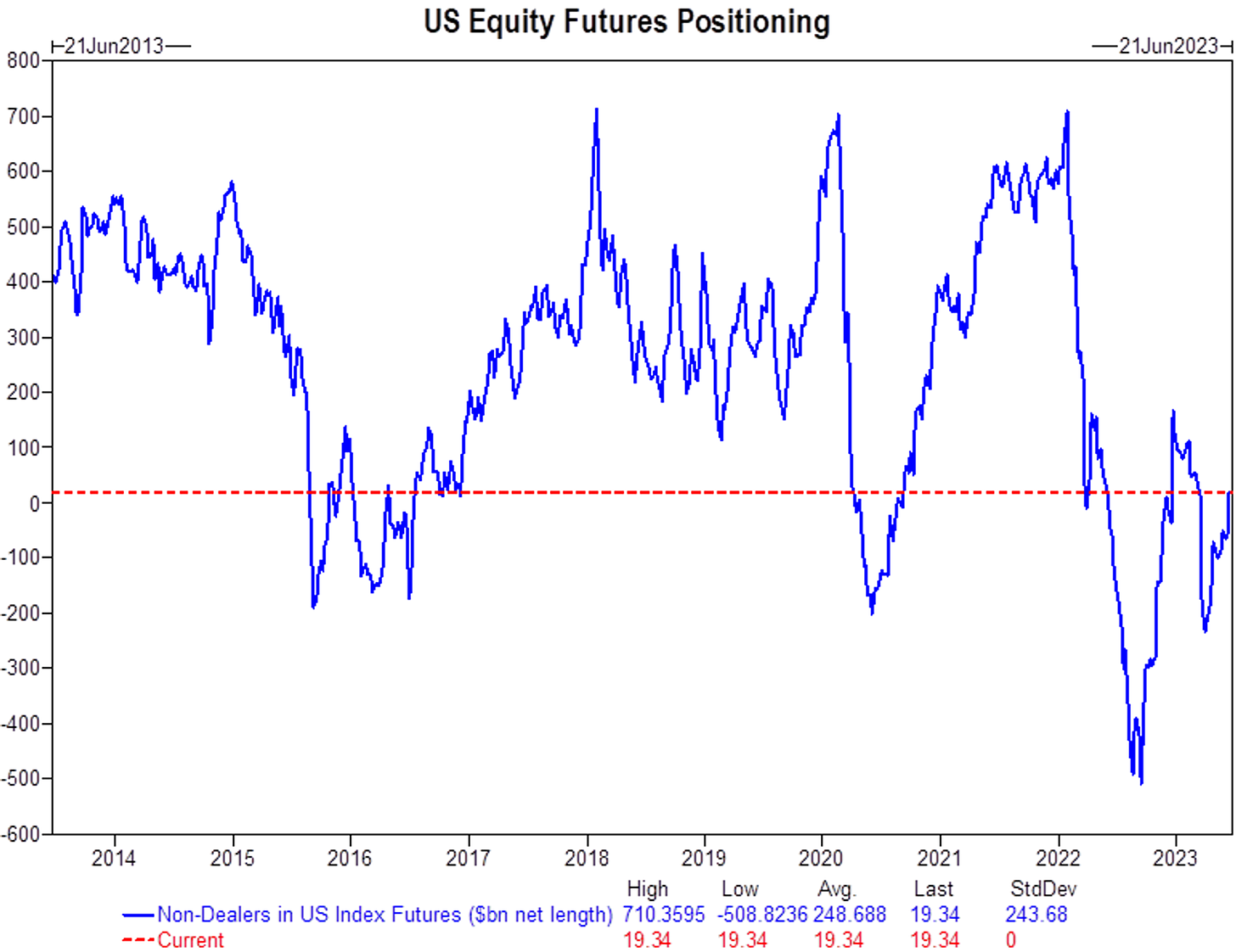

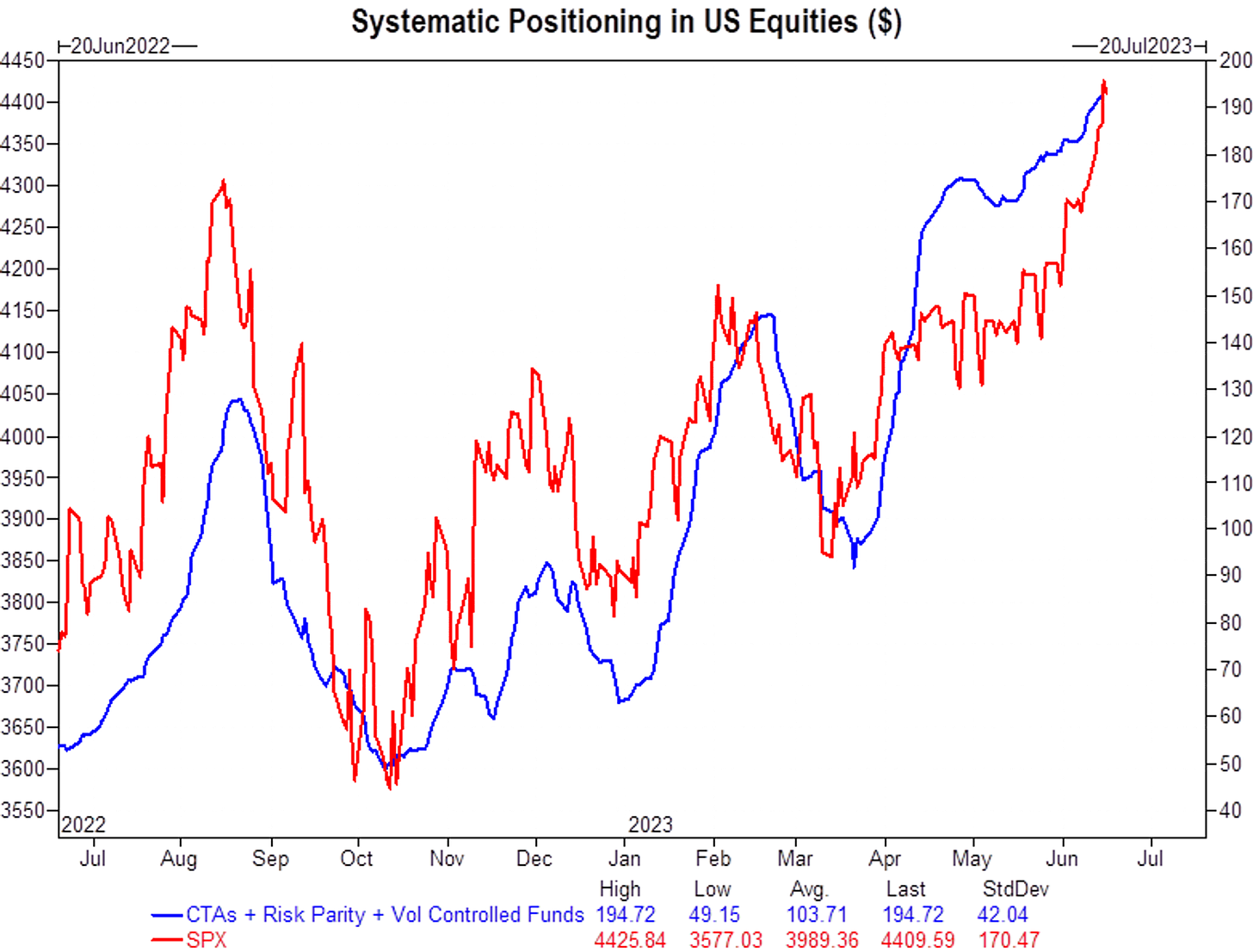

And this is reflected in the positioning of investors. Below is the graph representing the net exposure of non-bank investors to US index futures contracts, expressed in billions of dollars.

Non-bank investors can include fund managers, institutional investors, pension funds, hedge funds and other participants in financial markets that are not banks.

For the first time in 2023, market exposure is net long.

As well as systematic investors, those using algorithms. They haven’t been as exposed to US indices since August 2022.

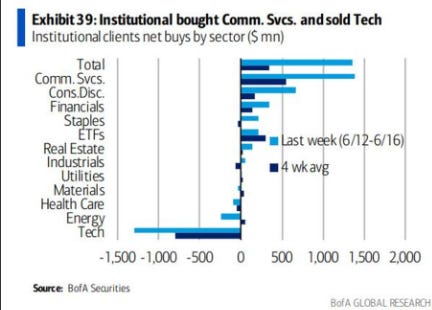

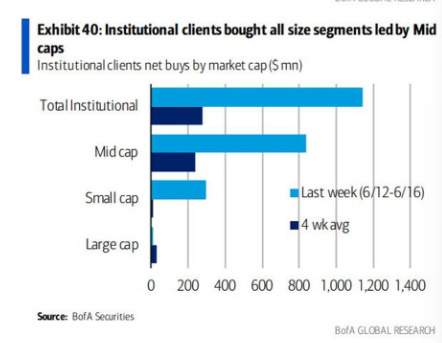

Who does what ?

Bank of America’s institutional clients are selling tech, buying communications and selling tech. “Institutional clients” include: pension funds, insurance companies, foundations, universities and sovereign wealth funds, etc.

And they are also starting to avoid buying large cap stocks at these price levels.

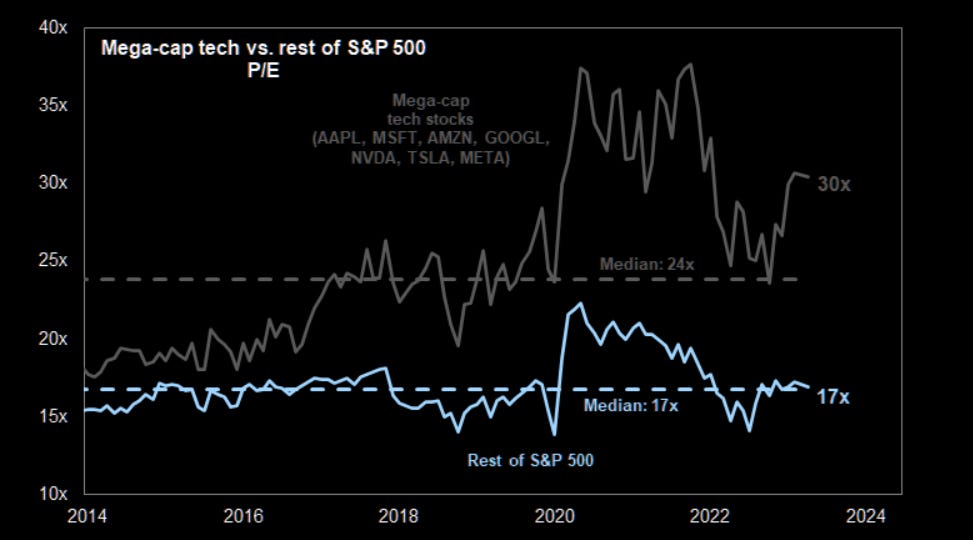

The problem here is, as we’ve seen many times, it’s the heavily capitalized tech stocks that have largely driven the indices in 2023.

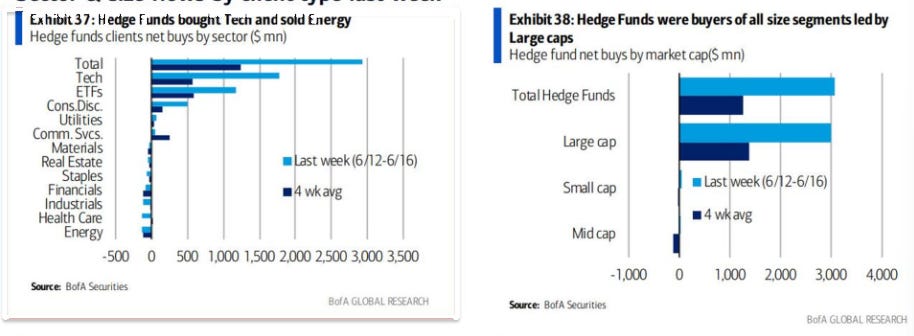

Hedge funds continue to buy technology stocks, and sell energy and the health sector. They therefore continue to have a positioning on cyclical stocks.

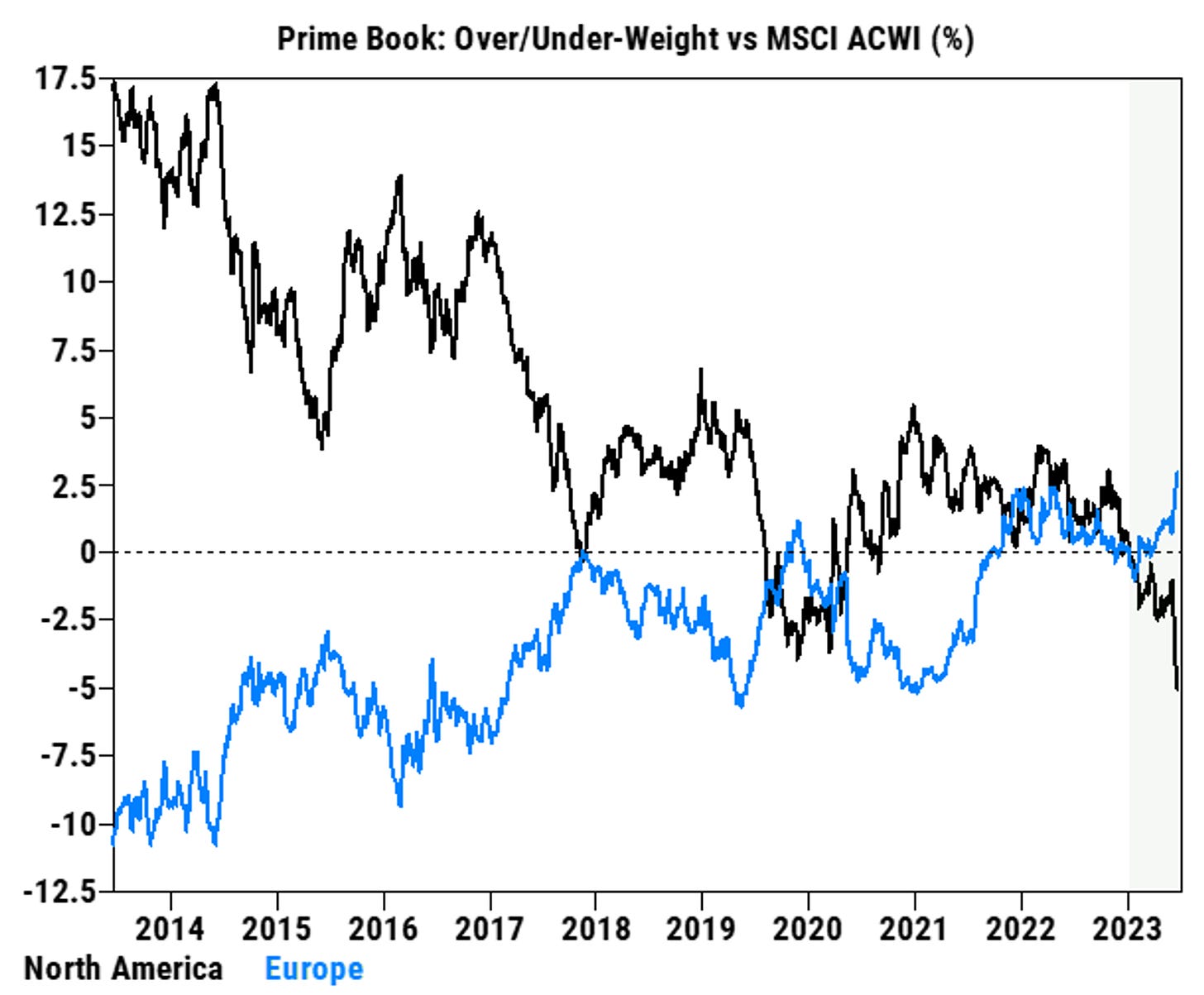

Goldman decided to underweight the USA to favor Europe.

Here we see two lines, blue for Europe and black for North America. Goldman was underweight the USA and overweight Europe compared to the MSCI ACWI index.

The MSCI ACWI (All Country World Index) is an index used to represent the performance of the global stock market.

If you enjoyed this article, feel free to share, like, and subscribe to The Macronomist.