In this context of rising key rates, a credit analysis of the companies you follow is welcome. I suggest that you review together 3 metrics that seem essential to me to understand if a group has its debt under control. The analysis of these multiples is perfectly coupled with that of financial leverage and return on equity (ROE). Conversely, it is inconceivable to make a decision based solely on financial profitability without ensuring that the weight of the debt in the balance sheet, the weight of financial interests in the income statement and the interest rate corporate appearance are acceptable.

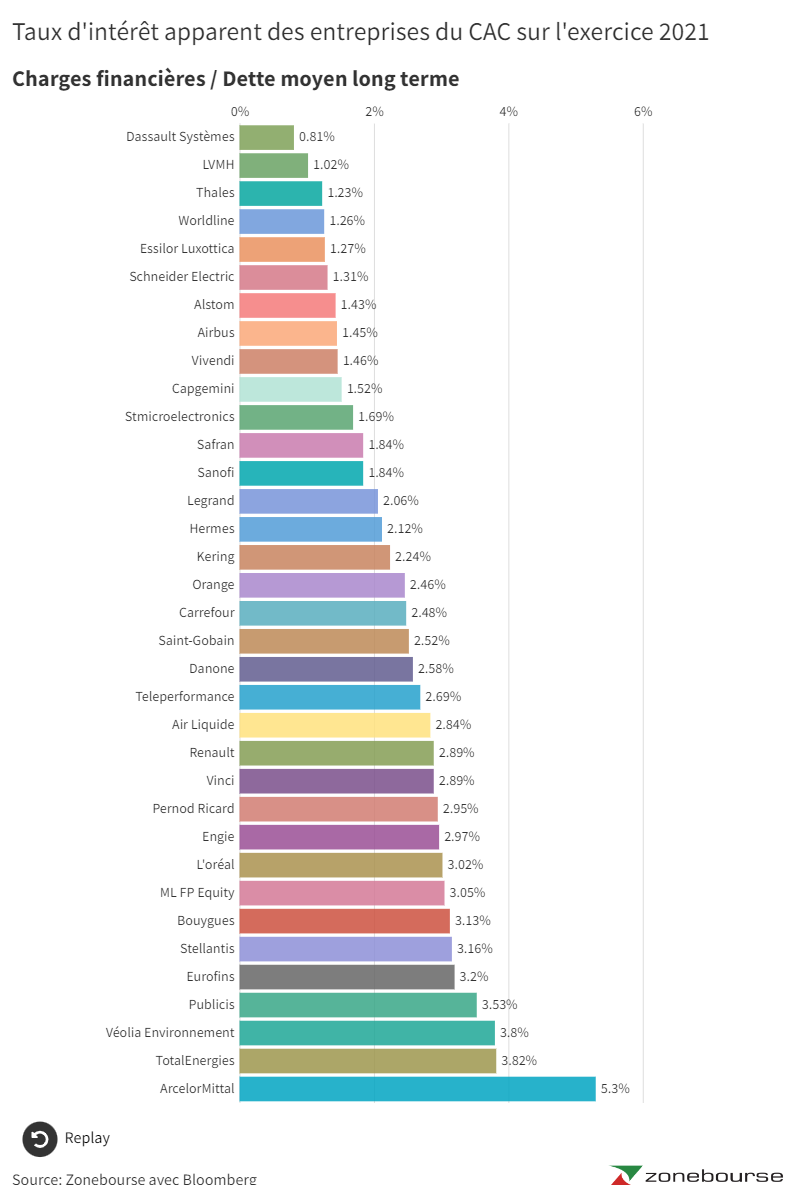

The apparent interest rate.

If you are used to consulting the financial information published by a company, you know that you can find the details of the lines of credit it has opened and the bonds it has issued with the maturity and the cost linked to each between them. However, these infographics are not always the easiest to interpret. To get an idea of the cost of a company’s apparent debt more quickly, I invite you to compare the item of financial charges in the income statement, to the stock of medium/long-term debt that you will find very easily in the liabilities of the balance sheet.

Note that the cost of net financial debt that you find in the CDR includes the interest income that the company received during the financial year. Naturally, when we want to compare what the company has paid in relation to the stock of money it has borrowed (bonds and bank loans), we eliminate these financial products (which are income) to keep only the relevant interest expense items. In the example below for the case of EssilorLuxottica, we eliminate the €30 million in interest income to keep only the expenditure items (€141 million).

Essilor Luxottica income statement and note 7 on financial charges. Source: DEU 2021 company

Having made these clarifications, let’s compare the 2021 apparent interest rate of all CAC 40 companies (excluding the financial sector). Remember that being able to borrow at low cost is a considerable advantage for creating financial leverage and increasing the return on equity tenfold.

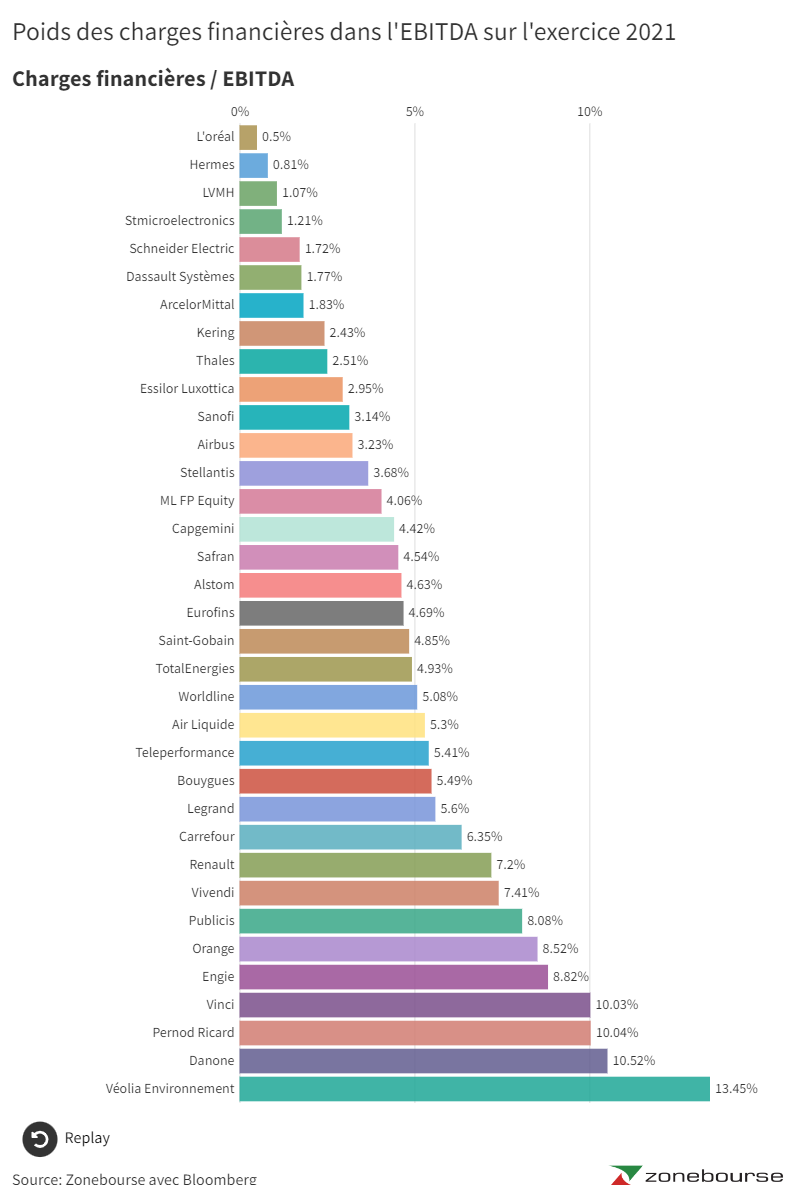

The weight of financial charges in the result of the company.

Creating financial leverage means using shareholders’ equity as collateral to borrow money at an interest rate below the company’s economic profitability. If the cost of the debt is too high and/or the company is unable to allocate this new capital to the development of its activity, there is destruction of value for the shareholder. It is for this reason that it is extremely important for an analyst to check the apparent interest rate linked to the debt.

However, paying its debt at an affordable price does not guarantee that the company will be able to meet its deadlines with great ease. It is for this reason that I invite you to pay attention to the weight of financial charges in the company’s EBITDA. Remember to analyze this report over time to detect companies with cyclical revenues that may find themselves in difficult situations during less successful years.

With these different metrics, we are not really in a position to judge the exposure of companies’ existing lines of credit to a rise in interest rates. To do this, we would need to know the proportion of loans at variable rates vis-à-vis the fixed part (note that most companies got rid of the variable part when it was strategic). However, if these companies approach banks or the bond market again for financing, it will inevitably be at a higher price and it is always good to know which companies are paying more for their debt than others and which ones financial charges represent one of the main items in the income statement.

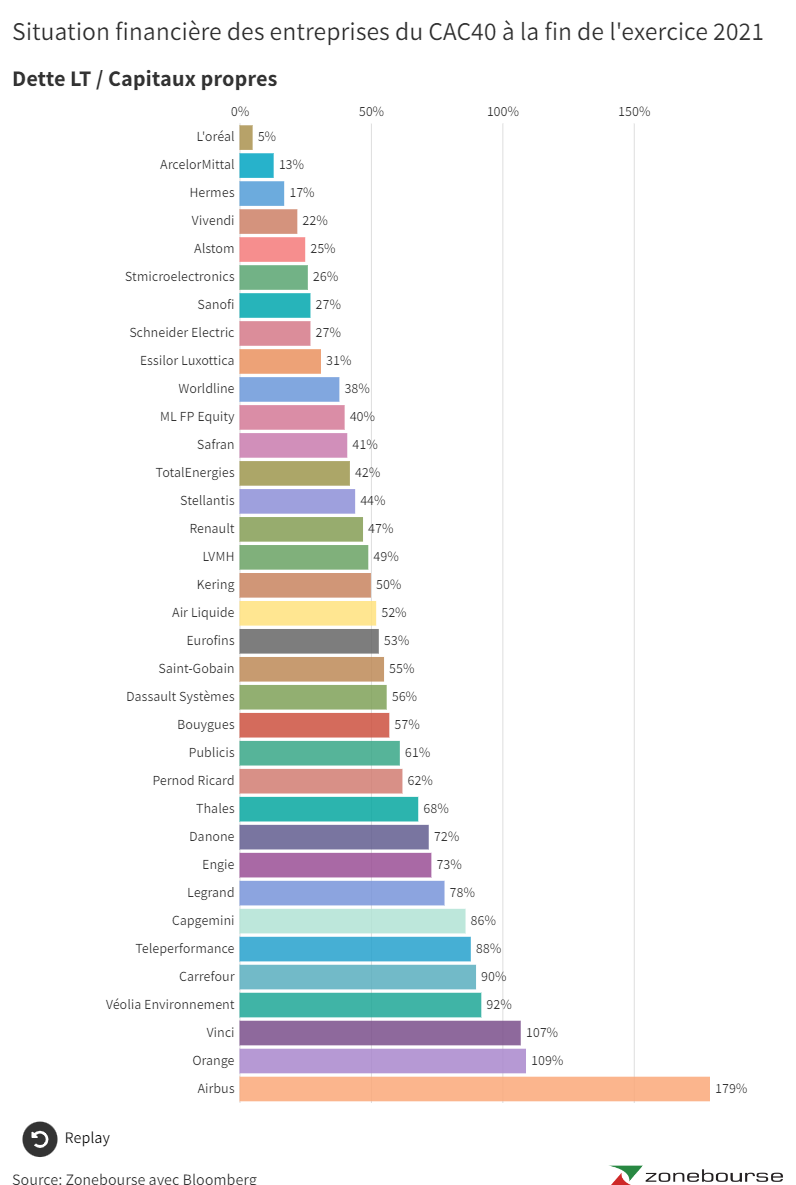

The weight of debt on the company’s balance sheet.

We now know which are the CAC40 companies for which the financial expense item is very significant. For example, 10.5% of Danone’s EBITDA is allocated to the reimbursement of financial interest linked to its debt. Danone’s apparent interest rate is 2.58%, which is relatively correct for a CAC40 company in this period of very low interest rates. We therefore understand that if in the future, for the same level of indebtedness, this rate were to double, then 20% of Danone’s EBITDA will have to be devoted to the reimbursement of financial interest. But we suspect that the company will not fully roll over its debt. Above all, it took advantage of low interest rates to increase its debt ratios and improve its financial profitability. What we hope is that from now on (and this over a medium-term horizon) the group will not find itself in the need to open new lines of credit, we rather expect that that the weight of the debt in the balance sheet is gradually reduced, at the rate of capital repayments.

To follow the evolution of the financial situation of a company, we must therefore also have an idea of the weight of the debt in the balance sheet of this one. We suspect that companies like Danone, which often have recourse to substantial debt, will try to reduce it over the years to come. Here is another chart showing the relationship between corporate debt and equity.

One would naturally think that the most indebted companies are those that pay their most expensive debt, but this is not always the case as you can understand by comparing the different tables.

I also invite you to be vigilant regarding the interpretation of this last graph: I have decided to reason here in terms of gross LT debt, without taking into account corporate cash. The same graph could be produced by taking into account the net debt / equity ratio, the message would then be very different.

If we believe these different tables (which, I remind you, only take into account the figures for 2021), we can draw the following conclusions:

Finally, be aware that with the rise in interest rates, the management of the working capital requirement (which is essentially financed with short-term resources) will once again become something increasingly important.

In recent months/years, in the very particular context that we are experiencing (negative real interest rates and high inflation), WCR has been a source of value creation for sectors where stocks are significant through the profits of inflation. As the authors of the Vernimmen point out, good management of working capital then consists precisely in not managing it. But this could change again in the years to come and it will then be necessary to be more vigilant vis-à-vis industries which present high WCR (steel, chemicals, consumer goods, luxury goods, building materials, mines, pharmaceuticals, etc.)