Saturday 20th February 2021

Interest concerns and economic hope

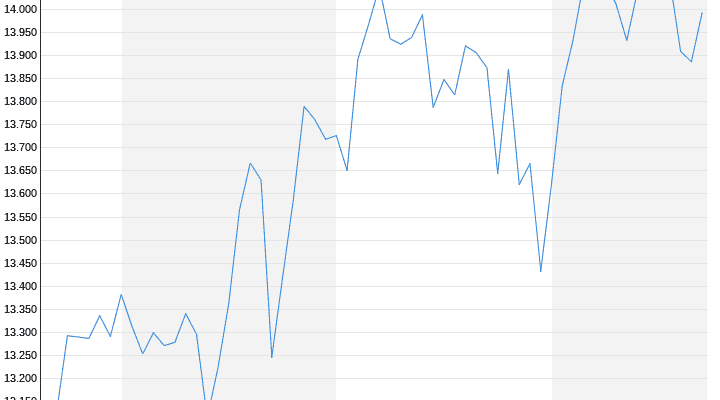

Dax finds it difficult to break free

The record bull market stalled. Equity investors are concerned about rising bond yields. The spread of the coronavirus mutations is also unsettling. On the other hand, however, there are hopes of an upturn in the economy and rising corporate profits.

The hanging game in the Dax could continue in the new week. Because: Corona lockdowns continue to look better than the economic outlook. There is still great uncertainty, especially with regard to mutations in the virus. According to experts, a braking effect for equities could also develop further increases in interest rates on the bond markets. At the same time, there is justified hope of increasing corporate profits due to the large economic stimulus package in the USA. It is difficult for the Dax to break free from this bracket.

The Dax has been hovering around 14,000 points for two weeks. The index reached a record high at around 14,169 points. He then sounded the low of the latest consolidation with a good 13,800 points. A clear trend is nil. On Friday it was enough for the Dax to end the week in a friendly way. In the end, the leading German index closed 0.77 percent higher at 13,993.23 points. On a weekly basis, there was a moderate minus of 0.4 percent.

Equity investors recently worried about the rise in bond yields, especially in the USA. Yields on ten-year US bonds rose to their highest level in a year. This could make bonds to stocks more attractive as an investment again. Market participants shouldn't be too unsettled by these concerns. Because there is a big difference to earlier phases of increasing returns: This increase in returns is desirable! With reflation, the chance increases that the states will grow out of their seemingly excessive debt ratios. That is certainly the reason why the US Federal Reserve explicitly wants to allow the inflation rate to rise above the 2 percent mark.

Dax is lagging behind

And there is another difference: Blackrock thinks about the returns that this time they even rose more slowly than usual in economic turns. In fact, returns are rising more slowly than prices. This makes the real interest rate even more negative. Sooner or later that will support asset prices again: stocks, real estate and probably gold too.

Many of the world's major indices set new records ahead of the recent return-driven consolidation. Nevertheless, market participants are increasingly frustrated, especially because the Dax is still lagging behind the other exchanges. In Shanghai and Hong Kong the leading indices have risen by 13 percent since the beginning of the year, in Tokyo the Nikkei gained 7 percent after adjusting for currency effects. In the Dax, on the other hand, it went up by just under 2 percent.

This may have something to do with the fact that the Dax had risen particularly strongly last year after the bear market. But it is also due to the composition: Too many titles are currently just stuck sideways. Only stocks that are still strong in terms of charts, such as car stocks, Siemens, Infineon or BASF and Covestro, will hardly generate any higher upward momentum.

Upward trend holds

A break in the upward trend at around 13,500 points is not in sight. Nevertheless, interest-rate-sensitive stocks from the telecom industry or the utility sector will continue to have a hard time. Companies that have low debt and generate high cash flows are likely to be better positioned.

The reporting season will continue to be in view in the coming week. On the macro side, the Ifo Business Climate Index and the development of the money supply are on the agenda. The Ifo Business Climate Index is hardly expected to change, somewhere near the January level of 90.1. The dynamics of monetary growth are also likely to remain virtually unchanged at a good 12 percent for the M3 money stock. That would be clearly positive for the markets: Liquidity isn't everything, but without liquidity everything is nothing.

In the USA, US consumer confidence is on the agenda on Tuesday, and according to the forecasts, this should not have changed much either. Incoming orders for durable goods follow on Thursday and the index of purchasing managers in Chicago on Friday. The question here is whether the large slaughterhouses in Chicago and the surrounding area have the high industry-specific pandemic risks under control.

.